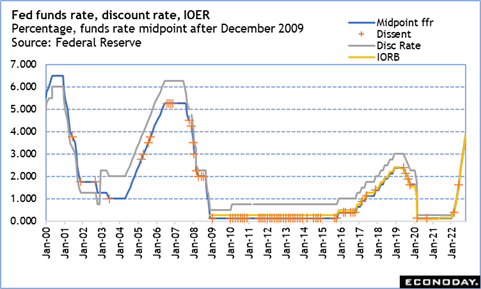

The results of the December 13-14 FOMC meeting are now one week away. The FOMC statement and quarterly update to the Summary of Economic Projections (SEP) are scheduled for 1400 EST on Wednesday, December 14. These will be followed by Chair Jerome Powell’s press briefing at 1430 EST. Expectations are almost universal for a 50-basis-point hike in the fed funds target range from the 3.75-to-4.00 percent range to 4.25-to-4.50 percent with a mid-point of 4.375 percent. Here are a few items to keep in mind for this FOMC meeting:

- A 50-point rate hike means the fed funds target will be the highest since 4.50 percent in October 2007, just before the credit collapse, housing bust, and onset of the Great Recession. It predates the decision to go to a range for the fed funds rate in December 2008.

- The statement will reflect that the fight against inflation is the priority half of the dual mandate as the maximum employment side is holding up well in spite of more restrictive monetary policy. Still, if we include the expected 50-point increase, rates will have gone up a whopping 425 basis points since March. The FOMC is going to be more cautious about lagged effects.

- The SEP is likely to see some revisions to forecasts for real GDP, the unemployment rate, and PCE inflation. The midpoint may not see big revisions, but I anticipate the range of forecasts may widen. There’s likely to be more disagreement about where the fed funds rate should top out and/or how long it should remain there.

- This set of FOMC voters will change over at the January 31-February 1, 2023 meeting.

- This meeting will get November’s senior loan officer survey. The survey isn’t on the publication calendar but will probably be released at 1400 EST on Monday, December 19.

- Recent remarks by New York Fed President John Williams suggest the FOMC may be discussing ways to ensure financial market stability through working with markets to improve resilience rather than through adjustments in monetary policy.

- Powell is likely to get more questions about the reduction in the size of the Fed’s securities holdings, including its impact on the Treasury market and the absence, given the incurring of liabilities on the balance sheet, of remittances to the US Treasury.