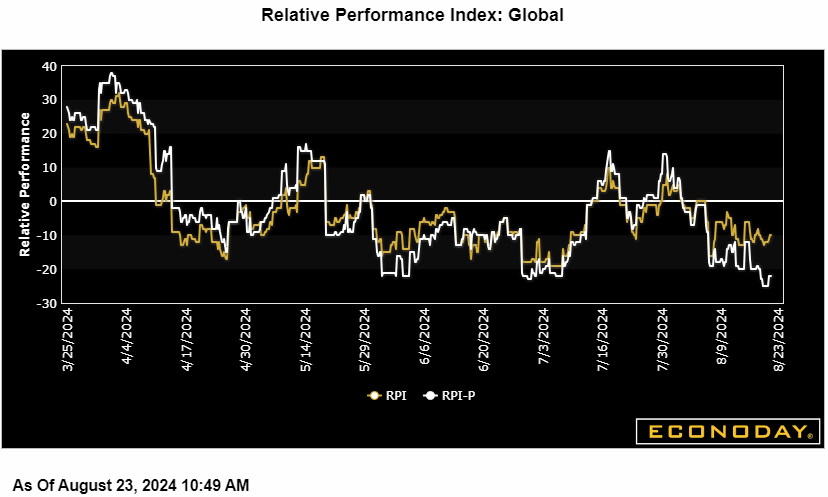

Global data held steady in the underperformance column, ending the week at minus 8 on Econoday’s Relative Performance Index (RPI) and at minus 21 when excluding price data (RPI-P), the latter indicating greater underperformance in real economic activity.

In the Eurozone, economic activity continued to undershoot market forecasts and put the RPI at minus 18 and the RPI-P at minus 32, the latter matching its weakest mark since the start of July. The economy would welcome another ECB ease in September but that would need further proof that inflation is behaving itself.

In the UK, upside and downside surprises effectively cancelled each other out. This left both the RPI and RPI-P at minus 5 and so close enough to zero to indicate overall economic activity performing much as expected. Another cut at the BoE MPC’s September meeting hangs in the balance.

In Japan, the RPI (6) and the RPI-P (4) remained in positive surprise territory, but only just. The BoJ still intends to tighten but the broader economic picture continues to argue against any aggressive moves.

There were no significant data releases in China leaving the RPI at minus 29 and the RPI-P at a lowly minus 60. Such levels were not weak enough to prompt another cut in loan prime rates but must at least keep the door open to further monetary easing down the road.

Lifted at week’s end by new home sales, both the RPI and RPI-P for the US ended at plus 13 to now indicate that recent US data, which had been flat to underperforming, are now coming in just ahead of Econoday’s consensus estimates.

At the top is Canada which is increasingly outperforming, at 37 on the RPI and 42 on the RPI-P in strength that would seem to make a third straight rate cut at the Bank of Canada’s September 4 meeting unnecessary, especially given cooling in consumer prices to 2.5 percent in July.