Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

September US wholesale prices – data collection for which happened before the federal government shutdown – rose as expected fueled by a surge in energy prices (gasoline prices saw an 11.8 percent spike). The costs for wholesale services saw no change, which might provide a modicum of comfort to hawkish Federal Reserve officials.

Overall, this report does not move the needle in either direction in terms of what the FOMC will do in December.

The knock-on effects of tariffs continue to show up in the data. Transportation and warehousing services costs continue to rise at a significant rate on a monthly basis, and jumped 3.4 percent compared to September 2024.

Food prices, at the forefront of current affordability concerns, accelerated both on a monthly and annual basis.

U.S. wholesale price inflation as measured by the Producer Price Index for final demand rose 0.3 percent in September, following an unrevised 0.1 percent dip in August, and matching expectations in the Econoday survey of forecasters. Final demand prices were up 0.8 percent in July and saw a 0.1 percent uptick in June.

Compared to September 2024, final demand PPI rose 2.7 percent, compared to a 2.6 percent increase for the 12 months ended in August. Expectations were for a 2.6 percent rise.

Final demand prices excluding foods, energy, and trade services saw a 0.1 percent rise in September, following a 0.3 percent rise in August, and a 0.7 percent jump in July. For the 12 months ended in September, prices for final demand less foods, energy, and trade services rose 2.9 percent, compared to a 2.8 percent increase on an annual basis in August.

Prices for final demand goods saw a 0.9 percent spike – following August’s 0.2 percent rise. This is the fifth consecutive monthly increase. Goods prices excluding food and energy rose 0.2 percent. Prices for final demand services saw no change in September, after a 0.3 percent decline in August. The services index excluding trade, transportation, and warehousing and for final demand transportation and warehousing services increased 0.1 percent and 0.8 percent, respectively.

September final demand prices excluding food and energy came in up 0.1 percent, following a 0.1 percent decline in August, and are up 2.6 percent from a year ago after a 2.8 percent rise in August.

Food prices jumped 1.1 percent after a 0.1 percent increase in August, and surged 4.0 percent compared to September 2024. Energy prices rose 3.5 percent in September after a 0.4 percent contraction in August, and are 3.8 percent higher when compared to September 2024 (after prices fell 1.9 percent on an annual basis in August).

Demand

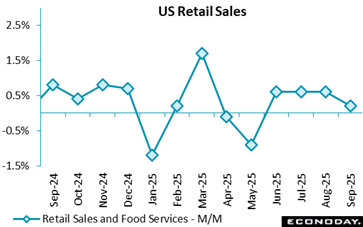

US retail sales slowed down more than expected in September, when they were up 0.2 percent, half the growth pace of the 0.4 percent consensus forecast in an Econoday survey, after rising 0.6 percent in August. On a 12-month basis, retail sales rose 4.3 percent, down from 5.0 percent the previous month.

Other measures of sales also reflected weakening momentum amid ongoing affordability concerns and uncertainty related to tariffs. These data precede the government shutdown, which started in October through November 12.

Sales excluding motor vehicles and parts increased 0.3 percent, as expected, down from 0.6 percent in August. Core retail sales, which also exclude gasoline, edged up 0.1 percent from 0.6 percent, below expectations, for a 12-month gain of 4.2 percent after 5.4 percent in August. Gasoline receipts increased 2.0 percent on the month and 3.1 percent year-over-year.

Auto sales contracted 0.3 percent on the month, bringing down the 12-month growth rate to 5.1 percent from 5.7 percent.

Sales also declined in discretionary items such electronics and appliances (minus 0.5 percent) and sporting goods, hobby, musical instruments (minus 2.5 percent). Clothing and accessories were down 0.7 percent.

By contrast, housing-related and essential goods and services sales increased from August, with gains of 1.1 percent for health and personal care and 0.2 percent for food and beverages. Sales of building material and garden equipment increased 0.2 percent, and furniture and home furnishing was up 0.6 percent.

General department store and food services and drinking places recorded higher sales on the month: 0.1 percent and 0.7 percent, respectively. Miscellaneous sales rose 2.9 percent.

Nonstore retailers receipts were down 0.7 percent.

Production

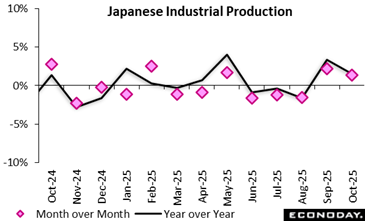

Japan’s industrial production unexpectedly rose a modest 1.4% on the month in October for the second straight gain (consensus -0.8%), driven by a rebound in the auto industry, but the outlook remains, underscoring the drag from stiff Trump tariffs on autos and metals and following a 2.6% rise in September, which was its first gain in three months.

The Ministry of Economy, Trade and Industry projected that output would slip back 2.6% in November before sliding a further 2.0% in December as the impact of trade rows becomes more apparent in the fourth quarter. METI maintained its long-held view that industrial output was "taking one step forward and one step back."

Takeaway: For a clear picture of how global trade and growth are impacting Japan’s economy, policymakers will have to wait for November trade data due on Dec. 17 and industrial output on Dec. 26. Japanese export values posted the second straight rise in October, up 3.6% on year, as the European economy continues picking up and China is slowly crawling out of the doldrums while export volumes were down for third straight month (-1.2% y/y), hit by the protectionist U.S. trade policy.

Looking at the bright side, the government noted in its monthly economic report for November released this week that there are signs of a pickup in goods exports to the United States while export prices of Japanese automobiles for the U.S. market appear to have hit the bottom. Earlier, Japanese carmakers slashed the sales prices for U.S. customers in hopes of protecting their market share.

Details:

Japan Oct industrial output +1.4% m/m (Sept revised up to +2.6% from +2.2%); second straight rise; median forecast -0.8% (range: -1.3% to +0.6%)

Japan Oct industrial output unexpected m/m rise driven by a rebound in passenger cars and engines, as export data show resilience despite US tariffs

Japan Oct industrial output index level at 104.6 is nearly a 2-year high, strongest since 105.0 in Dec 2023

Japan Oct industrial output +1.5% y/y (Sept revised up to +3.8% from +3.4%), second straight rise; median forecast -0.5% (range: -1.2% to +0.7%)

Japan METI keeps view: industrial output taking one step forward and one step back

Japan METI forecast index: Nov industrial output -2.6% m/m (adjusted for upward bias), Dec -2.0%

Japan Oct industrial output: 10 out of 15 industries post gains, 5 are down

Sentiment

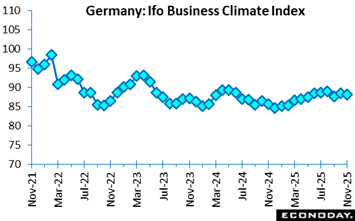

Germany’s economic sentiment weakened further in November as the business climate index slipped to 88.1, 0.2 points below the consensus and reflecting growing pessimism among firms despite a marginal improvement in assessments of current conditions.

The manufacturing sector remained under strain, with shrinking order books and sharp declines in expectations signalling continued uncertainty. Services offered a mixed picture, although current activity improved, caution persisted, particularly in transport and logistics, contrasting with renewed optimism in tourism. Trade faced a difficult month, with retailers reporting disappointment at the onset of the Christmas season as both current assessments and expectations fell. Construction displayed a paradoxical pattern as firms reported better current conditions, yet their future outlooks deteriorated due to persistently weak demand.

Overall, the latest data suggest that German businesses are experiencing an uneven climate, where widespread concerns about recovery overshadow isolated pockets of resilience. The divergence between improved present conditions and declining expectations indicates that firms remain wary of structural headwinds affecting demand, investment, and sectoral stability.

Growing concerns about current economic conditions as well as rising negative sentiment regarding future employment and income prospects continue to weigh on the US consumer, with inflation and concerns about finances top of mind.

The Conference Board’s Consumer Confidence Index declined by more than expected in November to 88.7, down from a revised 95.5 (previously 94.6) in October, and falling significantly short of expectations for 93.3 in the Econoday survey of forecasters.

Consumers’ assessment of current business and labor market conditions turned sour, while their short-term outlook for income, business, and labor market conditions remained pessimistic – and well below the threshold that indicates a recession ahead.

“Consumer confidence tumbled in November to its second lowest level since April after moving sideways for several months,” the report said. “Mid-2026 expectations for labor market conditions remained decidedly negative, and expectations for increased household incomes shrunk dramatically, after six months of strongly positive readings.”

Price inflation, tariffs and trade, and politics, and the federal government shutdown saw the most mentions, while labor market worries “eased somewhat but still stood out among all other frequent themes not already cited.”

Consumers’ views of their current financial situations plunged to the lowest level since August 2024; perceptions of future family financial situations were also “less buoyant”.

Average one-year inflation expectations remained at 5.7 percent in November from October.

The Conference Board also said the share of consumers expecting a recession over the next 12 months declined again in November, but the share of those who believe the economy is already in a recession rose for the fourth straight month.

On a six-month moving average basis, purchasing plans for autos, both new and used, declined – same for household appliances and most electronics. Plans to buy a home shrank in November but remain near two-year highs. Plans to purchase services in the coming months were curbed compared October.

US Review

Fed Beige Book Report on Economic Conditions in Focus Before FOMC Meeting

By Theresa Sheehan, Econoday Economist

US statistical agencies are issuing revised release calendars for the coming weeks as they catch up on delayed reports or skip some missed releases in favor of combining these with the next month’s data. The backlog of reports should be cleared by the end of December.

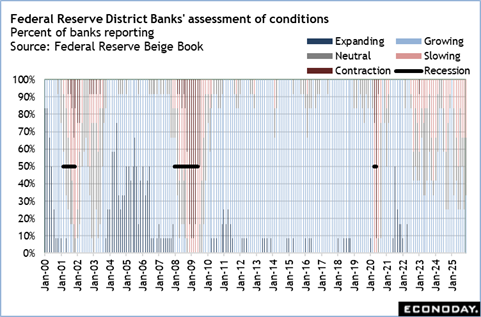

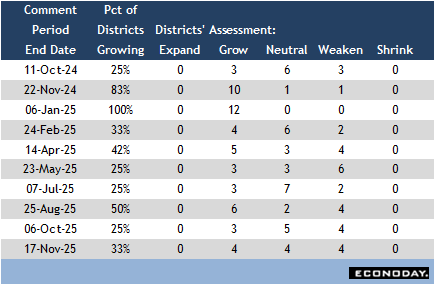

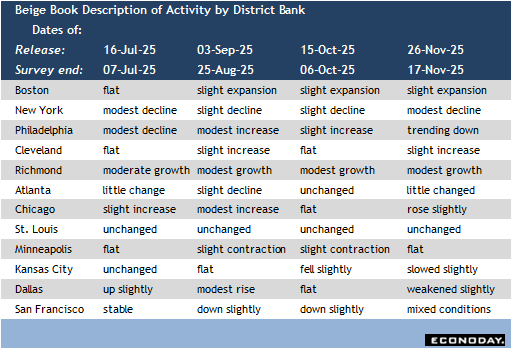

With the FOMC set to meet on December 9-10, the most important information released this week is the Fed’s Beige Book. Fed policymakers always pay attention to its content as important in gauging current conditions in the US economy. However, it has been pivotal during and around the period of the federal government shutdown in providing direction for setting monetary policy in the absence of other data.

While the FOMC will have some key reports for September – payrolls and the unemployment rate, CPI, final-demand PPI, and retail sales – this only takes the hard data through the end of the third quarter. The fourth quarter is now well advanced and the FOMC needs to be thinking about current conditions and the economic outlook. The Beige Book covers most of the intermeeting period from early October through mid-November and coincides with much of the shutdown.

Despite the presence of the shutdown, there was overall little change in conditions across the 12 districts. The Beige Book covers roughly from early October through mid-November. There was some narrow improvement, but activity is mostly reported as flat to modest expansion. Overall economic conditions remained soft in the Beige Book for the period between early October and mid-November, but there was some improvement from the prior report. Four districts reported at least some growth (Boston, Cleveland, Richmond, and Chicago), four said conditions where neither growing nor contracting (Atlanta, St. Louis, Minneapolis, and San Francisco), and four reported weaker conditions (New York, Philadelphia, Kansas City, and Dallas). The risk of recession remains and the outlook is a cautious one.

The FOMC will have to consider the balance of the dual mandate for maximum employment and price stability. The Beige Book shows that if hiring remains slow, so does firing. Conditions in the labor market are little changed in recent months. If payrolls are not growing, the unemployment rate isn’t on the rise in a way that would signal labor market distress. On the other side, tariff-related inflation is pushing up prices and it does not appear that it is done. Those who will have to pay the increased costs is still moving through the supply chain and businesses have not made final decisions about what can be absorbed and what will be passed on.

The Beige Book indicates that a majority of FOMC participants are likely to favor keeping rates on hold at the next meeting.