The Federal Open Market Committee (FOMC) is made up of 19 participants – as referred to in the minutes of the FOMC meetings – of whom 12 are actual voters when the time comes to decide monetary policy. The 19 participants are the 7 members of the Federal Reserve Board of Governors and the 12 presidents of the district banks.

The FOMC meets eight times a year to decide monetary policy. If there is a crisis during the intermeeting period, the FOMC will meet to discuss the situation. If necessary, the committee may adjust monetary policy during that time or take other measures to ensure the stability of the financial system. Although options may diverge as to the best path forward and dissents emerge in the vote, the committee majority determines policy, not any individual.

The FOMC’s main – and definitely preferred – tool to guide monetary policy is the federal funds target rate range. Its other tools include credit policy via reserve holdings and communications.

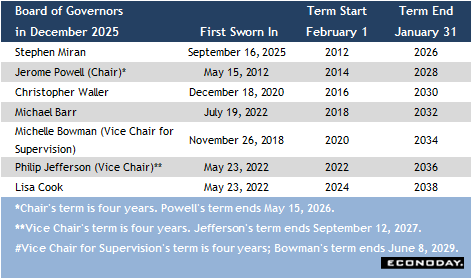

All the governors are FOMC voters

All the governors are FOMC voters. If a governor is not present to vote, recuses themselves from the vote, or if the complement of governors is less than the full seven, there is no alternate to vote for them.

The Chair of the Board of Governors is the Chair of the FOMC. At present, the Chair is Jerome Powell whose four-year term as Chair of the Board of Governors through mid-May 20, 2026. Speculation is high about who might be appointed as the next Chair, but there are certain things that need to happen.

The first is for an opening on the Board. Powell’s term as a governor runs through January 31, 2028. Even if he is not the Chair, he does not have to exit the Board. Note the recent example of Governor Michael Barr who resigned as Vice Chair for Supervision, but who remains on the Board and can until his term ends on January 31, 2032.

The next governor likely to leave the Board is Stephen Miran who was sworn in on September 16, 2025 for a term that ends January 31, 2026. Given that Miran was not nominated to the term beginning February 1, 2026, it seems he will be one of the shortest serving governors at the Fed. Miran does not have to leave office until the White House nominates someone to fill the new term and a new governor is sworn in. It is probable that the new year will see an official nomination for one of the names being floated as the next Chair. Miran can be a voter at the January 27-28, 2026 FOMC meeting, although most governors on the way out recuse themselves.

The remainder of the governors are unlikely to leave in the near future.

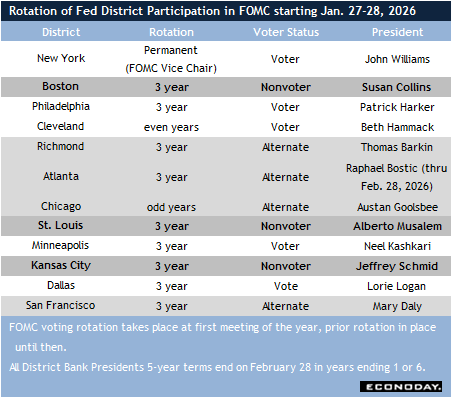

Five of the 12 district bank presidents are voters

All 12 of the district bank presidents are participants in FOMC discussions and contribute to the summary of economic projections (SEP). However, only five vote on monetary policy decisions at the end of the meeting. The roster of presidents is likely to see only one change in the coming year. No president is going to reach mandatory retirement age until 2028, although it is possible someone will decide to move on. However, Atlanta Fed President Raphael Bostic has announced he will retire at the end of his term on February 28, 2026 (Atlanta is not a voter in the FOMC rotation in 2026).

The president of the New York Fed the Vice Chair of the FOMC and has a permanent place as a voter. The remaining 11 vote in a specified rotation. The rotation takes place at the first scheduled meeting in a calendar year.

In 2026, the voters are:

New York – John Williams/Alternate 1st VP Sushmita Shukla

Cleveland – Beth Hammack/Alternate Chicago Austan Goolsbee

Philadelphia – Patrick Harker/Alternate Richmond Thomas Barkin

Dallas – Laurie Logan/Alternate Atlanta Raphael Bostic (through February 28, 2026)*

Minneapolis – Neel Kashkari/Alternate San Francisco Mary Daly

The policy approach from the 2026 voting presidents can be broadly said to be centrist, but that isn’t necessarily a useful categorization at the present juncture.

As Powell said in his December 10 press briefing, at 3.625 percent, the fed funds rate target is getting within reach of the longer-run forecast for a midpoint of 3.0 percent. There is no reason to expect more than another one or two 25-basis point rate cuts as long as the US economy is humming along near or above the longer-run forecast of up 1.8 percent, unemployment is not rising rapidly, and the worst of the upward price pressures from tariffs are passing through the inflation data. Policymakers will be cautious to bring its rate to a point where it is neither easy nor restrictive.