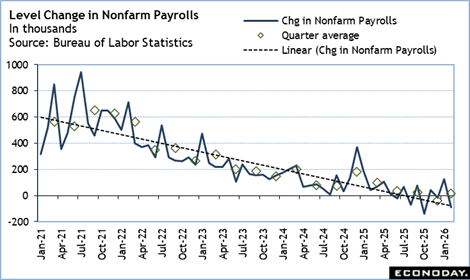

The monthly employment report for February delivered a shock with a steep drop in nonfarm payrolls of 92,000 that was on top of a net downward revision of 69,000 to the prior two months. Although the first quarter to-date is averaging a gain of 17,000 in new jobs, it is more-or-less in line with the meager gains in hiring over the past year. In the first quarter 2025 it was up 99,000, then dropped to up 34,000 in the second quarter, 23,000 in the third quarter, and fell 39,000 in the fourth quarter. The US economy has been subjected to a series of shocks since the spring of 2025, most of these coming from federal government policy decisions. The bitter cold and wide-ranging storm activity in January and early February has not helped the first quarter to recover and the war on Iran will further erode economic confidence as geopolitical uncertainty rises.

Fed policymakers are going to have to parse the data on the labor market carefully. The February decline in payrolls was affected by the nurses’ strike in New York and these jobs will come back in the March report. Nonetheless, there are hints that other businesses are paring payrolls where they can such as the decline of 27,000 in leisure and hospitality which is seeing pullbacks in consumer spending on activities like travel.

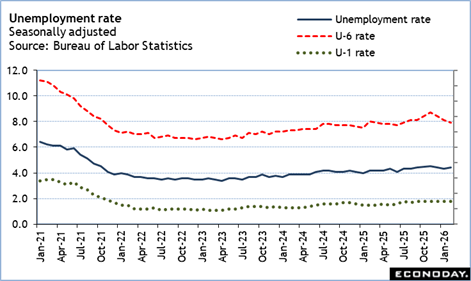

The unemployment rate is essentially unchanged at 4.4 percent in February after 4.3 percent in January. So is the size of the labor force which is up a scant 18,000 to 170.483 million in February as the number of employed fell 185,000 and the number of unemployed is up 203,000. The labor force participation rate is at 62.0 percent in February, the lowest since 62.0 percent in December 2021. There may be some strike impact on these numbers with some strikers reporting as unemployed. However, there are only 9,000 new entrants to the labor force in February which points to a lack of labor supply that will continue to pressure compensation costs, especially for skilled workers.

Fed policymakers will not overreact to one month’s data for the labor market but it is evident that the risks to the maximum employment side of the dual mandate are on the rise. The problem is that the risks to the price stability side of the dual mandate are also increasing. Energy costs can be volatile and swing wildly within short time spans. The war on Iran has steepened oil prices in just days but is unlikely to resolve lower in the near term as the conflict continues and spreads, infrastructure is damaged and/or destroyed, transport of supplies are unreliable, and refineries are forced to adapt to changing supplies of different types of crude. There will be knock-on effects as costs are increased for manufacturing and services. Where commodities inflation had been trending lower and helping bring inflation closer to the Fed’s 2 percent target, that is going to reverse.

The FOMC is once again facing the “tension” in the dual mandate to determine whether inflation or a weakening labor market are the more compelling need to address via monetary policy when it next meets on March 17-18.

On March 4, the White House finally did the official part of nominating Kevin Warsh to be the next Chair of the Federal Reserve. Warsh was nominated to the seat on the Board of Governors for the 14-year term ending January 31, 2024, thus meaning that Stephan Miran will be exiting the Board soon. Warsh was also nominated as the next Chair for a four-year term that will begin upon his confirmation and swearing-in. Given the current political turmoil, the Senate Banking Committee will have to make the nomination hearing a priority if it is to happen soon. Jerome Powell’s term as Chair ends mid-May. If no new Chair is confirmed by then, Vice Chair Philip Jefferson will be acting Chair of the Board of Governors. It is possible that Powell could be voted as Chair Pro Tem for the FOMC if he has decided to remain on the Board as a governor for the time being.