The May reports for the consumer price index (CPI) and final-demand producer price index (PPI) point to significant pass-through of prior price increases related to the spike in energy costs. Yet more pass-through can be expected in the coming months as elevated prices continue to impact producers. There is no indication that the current bout of upward price momentum is over. The longer oil prices remain elevated, the less able producers will be to absorb the shock. Costs will have to be passed on in the form of surcharges and/or higher prices. Where prices cannot currently be raised due to prior price agreements, these will likely go up once the agreements have expired.

Fed policymakers meet next week on June 16-17. The FOMC will have to make a difficult assessment regarding the mandate for price stability and the growing gap between the 2 percent inflation target and actual price movements. While the impacts of the spike in oil prices be less disruptive over for the longer term, the lengthening conflict in the Middle East means that neither is this a short-term problem for the US economy.

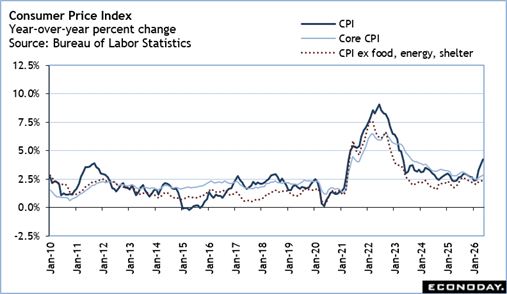

The May inflation numbers are broadly consistent with steep prices across major categories in the past two months.

The year-over-year rise in the consumer price index is 4.2 percent in May, nearly two percentage points higher than in February before the February 28 attack on Iran. Food prices have not escalated the way that energy costs have. The CPI for food and beverages is up 3.0 percent from May 2025, the same pace as before the war began. The CPI for energy is up 23.5 percent year-over-year in May compared to a decrease of 5.6 percent in February. The core CPI points to modest price increases outside food and energy at up 2.9 percent in May from a year earlier compared to up 2.5 percent in February.

However, that does not change that consumers are getting hit hard in these two big areas of nondiscretionary spending. Another is in housing costs. The CPI for shelter is up 3.4 percent in May, reversing a trend of incremental improvements that had levels off at up 3.0 percent in February and March. The CPI excluding shelter is up 4.7 percent in May after up 2.1 percent in February. Together, food, energy, and shelter account for over 40 percent of the CPI basket of goods. Consumer spending will shift away from discretionary goods and services as a result. And if the dollar value of spending is rising, it may be due more to costlier goods and services than actual consumption.

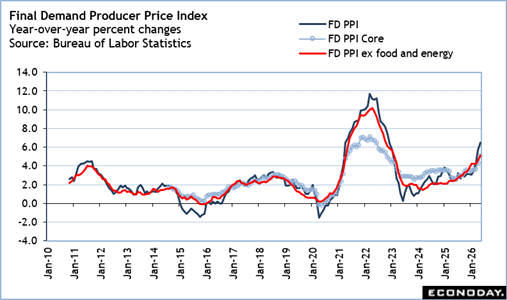

The May PPI does not suggest any moderation in price pressures in the pipeline. The year-over-year increase in final demand PPI is 6.5 percent in May compared to up 3.4 percent in February before the start of the war. The core PPI – excluding food, energy, and trade services – is up 5.1% compared to up 3.5 percent in February. The PPI for food is up 2.6% in May from a year ago compared to up 2.3 percent in February. This is only a modest uptick. However, the PPI for energy jumps to an annual pace of up 36.6 percent in May, still escalating rom up 22.7 percent in April, up 13.3 percent in March, and only up 2.1 percent in February. Costs for trade services – like shipping costs – have moderated a bit but are still elevated. The PPI for trade services is up 4.1 percent compared to May 2025 after rising 6.6 percent in April and 4.9 percent in March, and a dip of 0.3 percent in February.