The Econoday factory sector activity index (EFSAI)* for April is 10.8 after 13.1 in March and 6.7 in February. The reading suggests the factory sector is experiencing softening expansion based on six surveys of manufacturing from Fed district banks. The regional surveys show mildly improved activity in three of six reports and three with slower conditions than in the previous month.

A closer look at the individual surveys suggests that conditions are mixed and a little volatile. Where there is some improvement, it may not be sustained. The rise in the New York, Philadelphia, and Richmond regions may be a weather story as milder conditions follow on a period of severe cold that blanketed large portions of the Atlantic seaboard earlier this year. The mild declines in Dallas and Kansas City may reflect the impact of higher energy prices supporting a segment of local industries and moderating broader weakness. The plunge in the Chicago index is a reset after a large increase in the prior month with its underlying trend consistent with modest growth. Overall, activity in the factory sector seems closer to neutral.

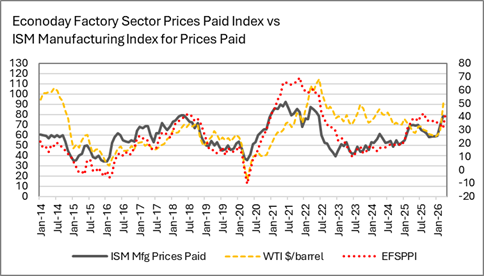

The initial impacts of the ware on Iran begun on February appear to have had a negative impact for the factory sector. In part, this could be attributed to the jump in prices paid and slowdowns in the global supply chain.

The Econoday factory sector prices paid index (EFSPPI) actually dipped to 31.4 in March after 33.6 in February and did not reflect the runup in energy prices in the first weeks of the war. However, the April EFSPPI rises sharply to 43.3 to its highest since mid-2022. Upward pressure will ease as prices move past the first surge, but input costs are not coming down again. Higher costs will pass through to the producer level and eventually reach consumers.

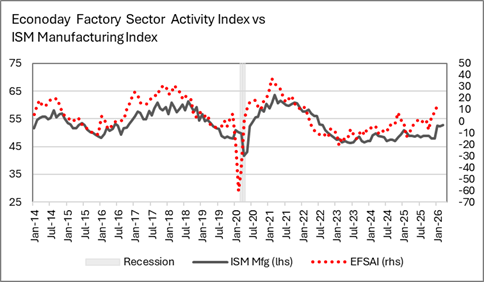

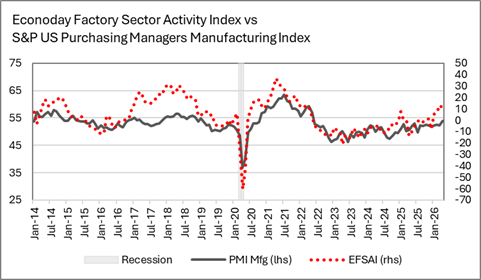

The EFSAI has strong correlations** with the major national indexes for activity in the factory sector. In both cases it points to an increase from the March data.

The S&P manufacturing purchasing managers index had a flash reading of 54.0 for April, up from the final 52.3 in March and 52.6 in February. The April preliminary reading is the highest the first half of 2022.

The ISM manufacturing index was essentially unchanged at 52.7 in March from 52.4 in February when it was the first three-month string above the 50-mark since 2022. Most districts are seeing gains in new orders and rising order backlogs, so the April ISM index could maintain tempered growth.

The S&P final manufacturing index for April is set for release at 9:45 ET on Friday, May 1.

The ISM manufacturing index for April is set for release at 10:00 ET on Friday, May 1. Consensus forecast is 53.0 for April.

*The EFSAI is an average of seasonally adjusted indexes from the Federal Reserve district bank surveys of manufacturing that includes smoothing for month-to-month volatility. The districts correspond with about 48 percent of the US labor force. An index above 0 indicates expanding activity and below 0 indicates contracting activity.

**S&P PMI for manufacturing correlation 0.803, ISM manufacturing 0.886.