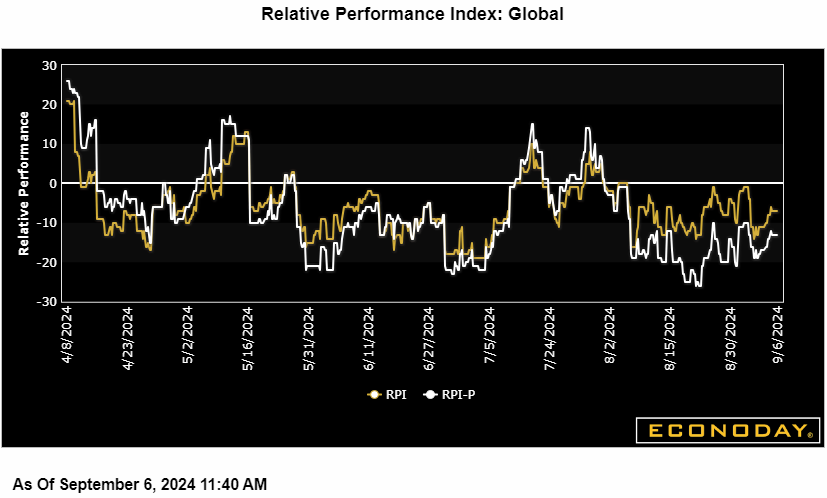

Global economic data have been consistently underperforming economist forecasts since the beginning of August, though only to a limited degree. Econoday’s Relative Performance Index (RPI) held unchanged in the week at minus 10, just within the low end of consensus ranges. When excluding prices (RPI-P) which have been coming in near estimates, the index falls to minus 17 which is likewise little changed to indicate that real economic activity has been, as it has for the last five weeks, generally subpar relative to expectations.

In the Eurozone, the RPI and RPI-P slipped to 8 and 4 respectively as a surprise downward revision to second-quarter growth simply boosted expectations for another ECB interest rate cut on Thursday.

In the UK, fresh signs of surprisingly respectable third-quarter GDP lifted the RPI to minus 4 and the RPI-P to exactly zero. With the economy performing much as expected, speculators remain split over this month’s MPC decision. Tuesday’s labour market update will be a key input.

In Switzerland, the RPI (14) and RPI-P (25) extended their move above zero. Even so, with inflation a little softer than forecast and superficially robust second-quarter growth masking soft domestic demand, financial markets still anticipate another cut by the Swiss National Bank later this month.

In Japan, unexpectedly soft household spending sank the RPI to minus 36 and the RPI-P to a lowly minus 71. Wage pressures may be rising but overall economic activity rates still argue in favour of only cautious monetary tightening.

In China, fresh data questioning the attainability of the government’s 5 percent growth forecast for 2024 saw the RPI and RPI-P close the week at minus 29 and minus 42 respectively. Both measures have been in largely negative surprise territory since May, sustaining pressure on the central bank to expand its monetary policy toolbox.

Both the US and Canada are performing exactly as expected, at scores of zero and plus 1 respectively overall and at zero and minus 1 when excluding inflation. The US scores assure a rate cut at the FOMC’s September 18 announcement though not necessarily justifying an upsized 50-point move; Canada’s scores won’t question the Bank of Canada’s decision in the prior week to cut interest rates with a third straight 25-point move.