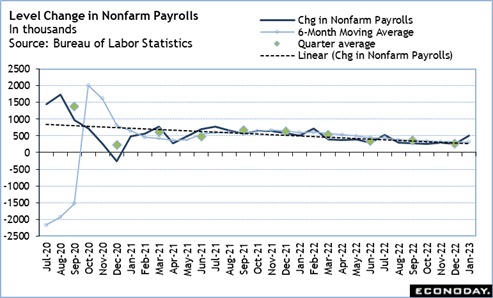

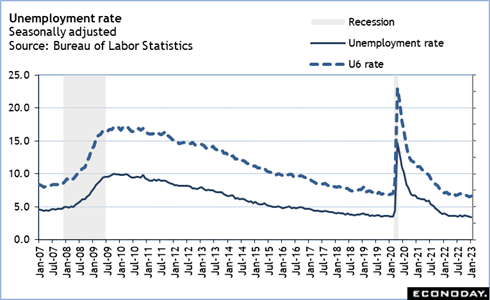

There’s virtually nothing on the economic data calendar that is likely to capture market attention in the February 6 week, especially as it will take a little time to fully digest the implications of January’s employment report. Nonfarm payrolls posted a whopping 517,000 increase in the month, dwarfing market expectations. Even accounting for a few seasonal factors like hiring of teachers and college professors at the start of a new semester or the travel industry desperately hiring to correct for some of the massive failures around the winter holidays, hiring was broad-based. The unemployment rate fell a tenth to 3.4 percent in January and remains consistent with tight labor supply. At least through January, the big sectoral layoffs don’t seem to have changed the wider story that many businesses are hungry for workers and snapping them up where they find them.

With few numbers to focus on, attention will shift to comments from Fed officials. Markets are clearly anticipating a rate cut later this year, while policymakers will be pushing back on that notion. Fed Chair Jerome Powell certainly gave no indication that restrictive monetary policy will be rolled back any time soon at his February 1 press briefing.

There’s always the caveat that the Fed is data-dependent in its decision making. If inflation data are persuasively lower for a sufficient number of months in a row to argue that pressures have been tamed, then a rate cut becomes more possible. But Powell’s remarks suggest that that will be a high and wide bar. It’s been made clear that the Fed does not want to change direction only to have inflation reemerge. Policymakers are more willing to overstay with restrictive rates than risk allowing entrenched inflation or damaging their credibility as inflation fighters. As long as the labor market data is consistent with an imbalance in labor supply and demand, and the economy ekes out growth, the FOMC is going to keep policy restrictive. It may pause on further rate increases, but it is doubtful it will cut.

I’d also note that under the dual mandate, if the economy rebounds and labor markets remain strong, the prescription for monetary policy will be to keep rates higher to prevent overheating. This isn’t the most likely scenario, but given the resilience of the US economy, the narrow path to avoiding a recession should not be discounted.

The January 31-February 1 FOMC meeting was the last before Chair Jerome Powell will deliver the semiannual monetary policy testimony later in February, or in case of scheduling problems, by early March. The dates have not yet been set. Any remarks by Fed officials in the February 6 week should be read in that context. Powell and the others will not want to muddy the message that will be in the semiannual Monetary Policy Report to Congress. Whatever they say is likely to preview what will be in the report and Powell’s prepared testimony when he appears before the Senate Banking Committee and the House Financial Services Committee. Powell’s appearance at the Economic Club of Washington, DC on Tuesday at 12:40 PM will get a lot of attention as he may update his outlook in light of the January employment numbers. There are other appearances by Fed governors later in the week. The only other one likely to highlight monetary policy is Governor Christopher Waller at 13:45 ET on Wednesday.