The January 23 week encompasses the communications blackout period around the January 31-February 1 FOMC meeting. This starts at midnight on Saturday, January 21 and runs through midnight on Thursday, January 26. Fed officials will make no public comment about monetary policy during this time. Note that the Fed has announced that Chair Jerome Powell has tested positive for and is symptomatic for Covid-19. His case is said to be mild. In all likelihood he will be able to attend the FOMC meeting – either remotely or in person.

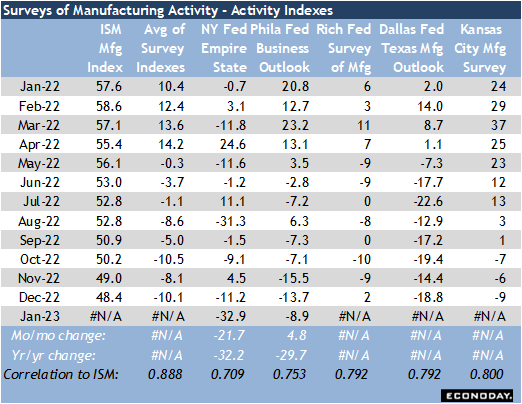

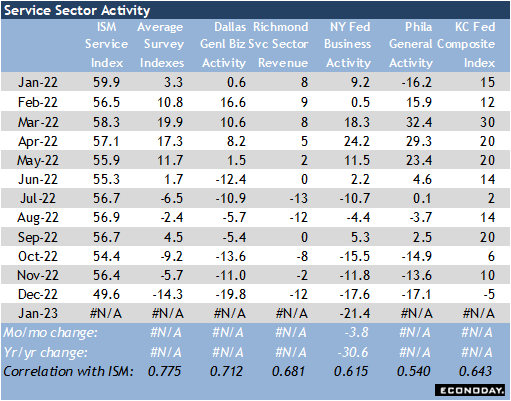

In any case, most of the data that will substantially influence the outcome of the FOMC decision have already been published. The only new reports that might have an impact are the regional Fed surveys of manufacturing and services for January. Already reported was the New York survey for manufacturing (Empire State) which showed an outsized drop while service sector data remain in contraction. Then the Philadelphia Fed survey for manufacturing told a more positive story, although its factory sector is slowing. In the coming week, the Philadelphia Fed will release its survey of the service sector at 8:30 EST on Tuesday. The Richmond Fed’s surveys of manufacturing and services will be reported at 10:00 EST on Tuesday. The Kansas City Fed’s manufacturing survey will be at 11:00 EST on Thursday and service sector survey at 11:00 EST on Friday. If these back up the data that the factory sector is moving into recession and that activity in services is continuing to slow, it might give Fed policymakers another reason to reduce the size of the next rate hike to 25 basis points after the 50 basis points in December. The FOMC will have evidence that inflation is improving – if still too high – and incorporate lagged effects of previous rate hikes into their policy outlook.

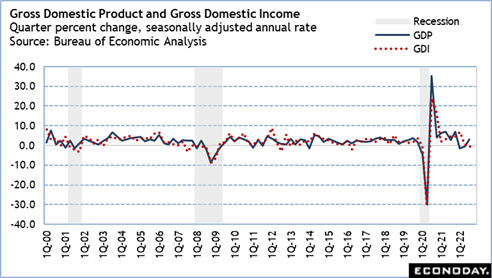

The report that is most anticipated is the advance estimate of fourth quarter GDP at 8:30 EST on Thursday. The Atlanta Fed’s GDPNow looks for an increase of 3.5 percent in the final quarter of 2022, similar to the 3.2 percent rise in the third quarter. While this makes the second half of 2022 one of solid growth, indications are that first-quarter 2023 is going to reflect subpar activity, at best.