In the July 10 week the focus will be on the reports related to inflation – the consumer price index (CPI), final-demand producer price index (PPI), and the import and export price indexes. All three are for June and will be released at 8:30 ET on Wednesday, Thursday, and Friday, respectively.

These are the last major reports on inflation that the FOMC will have in hand when Fed policymakers meet on Tuesday and Wednesday, July 25-26. With data related to the labor market showing still tight conditions despite some reductions in job openings and slowing in hiring, the inflation data will determine if the FOMC decides to hike rates again at this next meeting. While the Fed’s preferred measure of inflation is the PCE deflator, this June report will not be available for the FOMC. It will not be released until 8:30 ET on Friday, July 28.

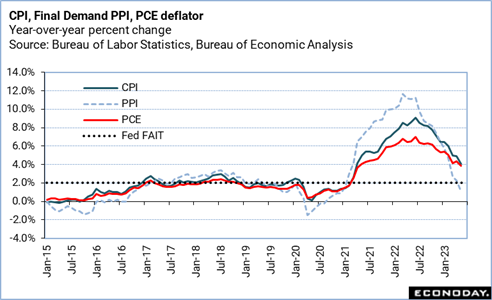

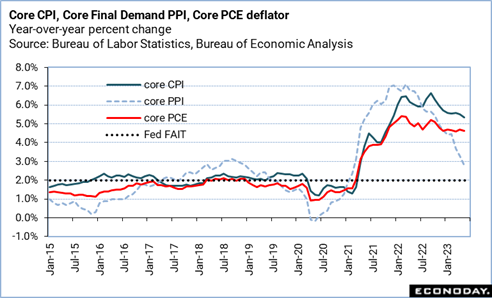

So-called “headline” inflation – for all items in the index basket – has been coming down steadily due to relief in commodities prices where demand has eased and supply chains improved. It is price pressures at the “core” – all items excluding food and energy – where central bankers see inflation as more persistent and therefore more likely to need restrictive monetary policy for some time to come.

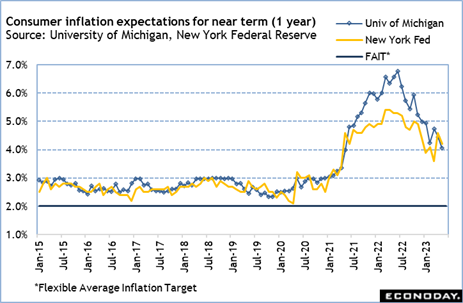

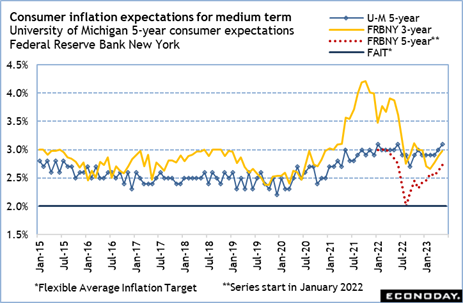

Fed policymakers are also keeping a close eye on inflation expectations. Failure to control inflation could unsettle expectations with the result of inflation becoming entrenched and making it more difficult for policymakers to credibly act to fight inflation. So far, though inflation expectations for the medium term have only risen modestly since the beginning of the current inflation episode, they remain above the Fed’s 2 percent flexible average inflation target. The FOMC wants to ensure that expectations do not lose their anchor.

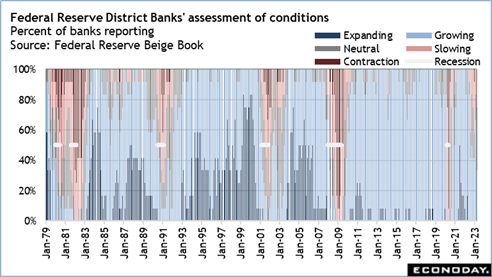

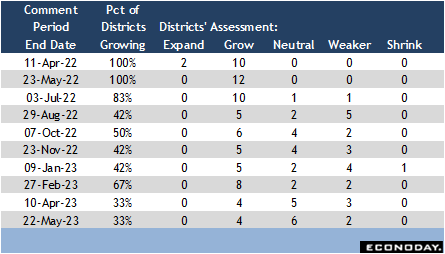

Also important for the upcoming FOMC meeting is the release of the Fed’s Beige Book compilation of anecdotal evidence about conditions across the 12 District Banks. Recent Beige Books have been consistent with the sort of “subpar” or underperformance that Fed officials have talked about in consequence of the aggressive series of rate hikes begun in March 2022 to tame inflation. The next report is set for release at 14:00 ET on Wednesday.

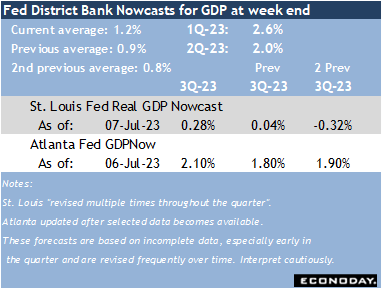

GDP Nowcasts from the St. Louis and Atlanta Feds both anticipate a below-trend increase in third quarter GDP. The St. Louis Fed’s Real GDP Nowcast looks for meager growth of 0.28 percent when the advance estimate is released at 8:30 ET on Thursday, July 27. The Atlanta Fed GDPNow forecasts an increase of 2.1 percent, quite similar to the up 2.0 percent in the second quarter.