There is little doubt that the coming will be tightly focused on the FOMC meeting on Tuesday and Wednesday. The release of the meeting statement at 14:00 ET on Wednesday will settle speculation about whether Fed voters will pause interest rate hikes or take rates higher for the eighth meeting in a row. If the Committee raises rates, by how much? Will it be a 25 or 50 basis points?

At issue is how much emphasis will the FOMC put on the state of the banking sector which is currently seeing a number of problems that regulators have to deal with. The Fed likes to ensure that markets remain calm as the best way to ensure the transmission of monetary policy. Would a rate hike unsettle things further or convey confidence that the problems are not systemic and within the capacity of the Fed and other regulators to fix without undue disruptions?

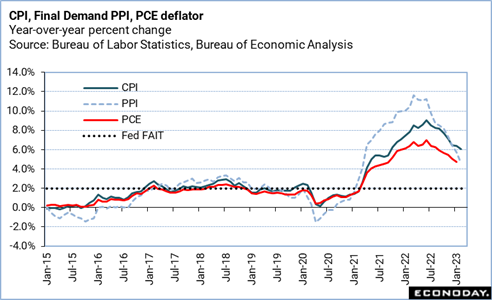

Then there’s the matter of fulfilling the dual mandate. Can the FOMC afford to let up in the price stability fight after the annual revisions for 2017-2022 showed inflation higher than previously thought? Was the easing up on price pressures in February after an unexpectedly high reading in January enough to keep the rate hike at 25 basis points? Or is one month’s data not enough to offset inflation expectations for the medium term which were a bit higher for some measures in February and early March? At least the FOMC need not feel immediately troubled by labor market conditions. The evidence suggests that if job openings are decreasing and hiring starting to slow, significant widespread layoff activity has yet to emerge except in a few narrow sectors – notably technology. An unemployment of 3.6 percent has a way to go before it could be considered anything except low in the historical context.

In the end, FOMC voters could opt for a slightly more cautious 25 basis points; if problems in the banking sector had not manifested, a 50 basis points would have been a stronger possibility.

Perhaps more interesting than the March 22 FOMC statement will be the Summary of Economic Projections (SEP). Markets will be watching for any significant – and maybe insignificant – shifts in the collective forecast. There will be a close eye on how much more rates are forecast to rise in 2023 and when the FOMC consensus is for the first possible rate cut.

Powell’s press briefing at 14:30 ET on Wednesday will be the first opportunity for the press to query the Fed Chair about recent turmoil in the banking sector. Much of the news became public just as Fed officials entered the communications blackout period around the meeting (midnight, Saturday March 12 through midnight, Thursday, March 23). Unless there was an urgent need to alter the signals previously given about the direction of monetary policy, it is not a topic that Powell would speak about publicly until after the meeting. Powell is likely to get as many questions about the state of the banking industry in the US as he will about the FOMC decision and forecast.

It is a relatively light week for economic data. The two reports most likely to capture market attention are the NAR data on sales of existing homes in February at 10:00 ET on Tuesday, and the government report on sales of single-family homes in February at 10:00 ET on Thursday. The dip in mortgage interest rates in December and January could give a little boost to home sales in February.