September 5 week was a full market close in observance of Labor Day making a sparse week for the economic calendar even sparser. This will allow plenty of time to mull over the August employment numbers from the prior week and speculate about the direction of Fed monetary policy. With one exception, the reports on this week’s release schedule don’t have much potential to move the needle on expectations for another big rate move at the September 20-21 FOMC meeting.

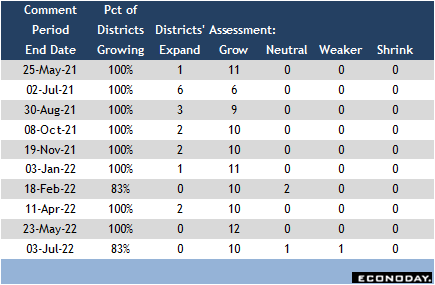

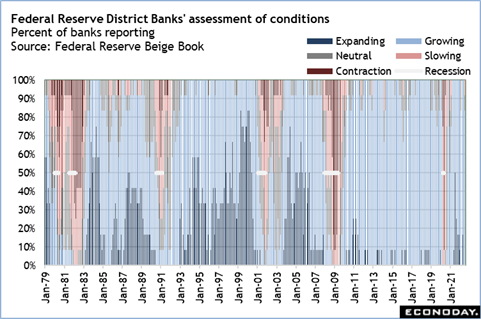

The exception is the Fed’s Beige Book at 14:00 ET on Wednesday. The Beige Book – called by no one by its proper name, the Summary of Commentary on Current Economic Conditions by Federal Reserve District – is a compilation of anecdotal evidence about economic activity in the 12 Fed district banks and is released two weeks ahead of the FOMC. While it is not hard data, it is a useful gauge of the strength or weakness of the US economy and is good at signaling turns in the economy. All Fed policymakers pay attention to its contents.

The Beige Book doesn’t provide an estimate of the size of economic growth, but it does point clearly and in close proximity to when a downturn is on the way, or an upturn is in the works. As of the July Beige Book, the economy looked softer but not in immediate danger of a recession. Ten of 12 districts continued to report expansion, although the language suggested a downgrade in activity. It is when only 6 or 7 districts are reporting expansion after a period of growth that a recession starts to look likely. Wednesday’s Beige Book – which will cover early July through late August – should see growth stable for the moment.

With the labor market indicators solid – and with a desirable rebalancing of supply and demand – Fed policymakers are weighing the strength of the US economy after significant rate increases earlier this year. Just how much more rates can be raised from the current more-or-less neutral fed funds rate of 2.25-2.50 percent without choking off growth while stifling demand-side inflation pressures is the question facing the FOMC. The outlook is for a slightly restrictive stance after the next FOMC meeting. Whether that will mean a 50 or 75 basis point increase depends on some of the other data reports before those deliberations. These include the August CPI report at 8:30 ET on Tuesday, September 13, and the August retail sales numbers at 8:30 ET on Thursday, September 15.