Last Week: Bank of Canada Cuts Rate, Bank of Japan Holds Steady, as Expected

Edited by Simisola Fagbola, Econoday Economist

The Economy

Canadian Monetary Policy

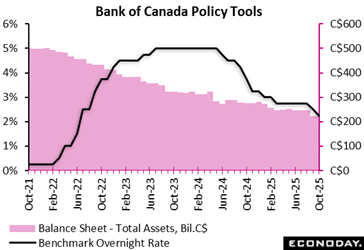

As was widely expected, the Bank of Canada reduced its key policy rate by 25 basis points to 2.25 percent, citing “a difficult transition” for the Canadian economy.

Going forward, the policy statement raised the bar for further rate cuts. “If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment,” it said. The central bank also stressed that the structural nature of the “damage” caused by the trade conflicts limits the role monetary policy can play to support growth while maintaining low inflation.

Should the outlook change, however, the BoC is prepared to respond. It projects GDP to grow 1.2 percent this year, with a “weak” second half as “U.S. trade actions and related uncertainty are having severe effects on targeted sectors including autos, steel, aluminum, and lumber”.

GDP is projected to slow down even further to 1.1 percent in 2026, before picking up to 1.6 percent in 2027. While it pointed out the “sticky” September inflation numbers with its own core measures around 3 percent, it estimates underlying inflation to be around 2.5 percent when considering a broader range of indicators. It expects inflationary pressures to ease, with inflation close to 2 percent over the projecting horizon.

Japan’s Monetary Policy

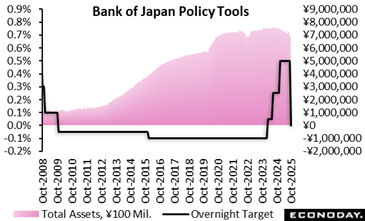

The Bank of Japan’s nine-member board voted 7-2 to maintain the target for overnight interest rate at 0.5 percent, in line with the consensus forecast and extending the policy stability seen since early in the year. Board members Naoki Tamura and Hajime Takata proposed an increase in the rate to 0.75 percent, as they did previously.

Officials also published updated economic forecasts. Core inflation forecasts are unchanged at 2.7 percent in this fiscal year, and then 1.8 percent and 2.0 percent in the following two fiscal years. Real GDP forecasts for fiscal years 2026 and 2027 were also unchanged at 0.7 percent and 1.0 percent respectively, with the forecast for the current fiscal year revised slightly higher from 0.6 percent to 0.7 percent.

Although their forecasts were little changed, officials noted risks to the outlook, with ongoing global trade tensions suggesting to them that growth may be weaker than they currently expect. Risks to the inflation outlook, however, were considered to be evenly balanced. Although they concluded no change in policy settings was warranted today, officials stressed that policy will continue to be set in upcoming meetings "without any preconceptions".

Eurozone Inflation

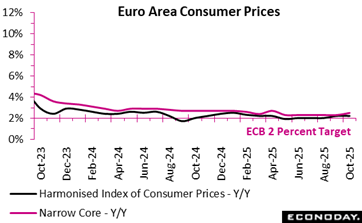

Euro area inflation eased slightly to an estimated 2.1 percent in October 2025, indicating continued progress toward price stability despite persistent pressures in some sectors. Services remained the strongest contributor, rising to 3.4 percent, which reflects ongoing wage adjustments and elevated demand for labour-intensive activities. Food, alcohol, and tobacco slowed to 2.5 percent, suggesting that supply chain pressures are gradually normalising. Non-energy industrial goods grew modestly at 0.6 percent, pointing to improved manufacturing conditions and reduced input costs.

Energy prices fell further to minus 1.0 percent, largely driven by lower wholesale gas and oil costs and improved storage capacity across Europe. This decline helped to offset more stubborn price increases in services, acting as a balancing force on household budgets. The overall picture suggests a disinflationary trend, although the divergence between service and goods categories highlights underlying structural cost dynamics.

Regionally, headline inflation fell in Germany (2.3 percent after 2.4 percent), France (0.9 percent after 1.1 percent), and Italy (1.3 percent after 1.8 percent), but rose in Spain (3.2 percent after 3.0 percent).

If services inflation remains elevated, the European Central Bank may face challenges in anchoring inflation firmly at its 2 percent target. However, the continued easing across most components indicates growing resilience in the euro area economy.

Eurozone GDP

The euro area economy showed a modest improvement in the third quarter of 2025, with seasonally adjusted GDP rising 0.2 percent compared with the previous quarter. This marks a slight acceleration from the 0.1 percent expansion recorded in the second quarter, suggesting that growth momentum is slowly building despite persistent economic headwinds.

On an annual basis, GDP increased by 1.3 percent, a small easing from the 1.5 percent recorded previously. This indicates that while year-over-year growth remains positive, the pace of expansion is gradually cooling. The figures point to an economy navigating a challenging environment of weak external demand and cautious consumer spending, yet still avoiding stagnation. Among the top four nations within the region, Germany (0.0 percent after minus 0.2 percent) and Italy (0.0 percent after minus 0.1 percent) showed no growth in the third quarter, while France (0.5 percent after 0.3 percent) grew.

However, the rate of increase in Spain (0.6 percent after 0.8 percent) decelerated. In essence, the data highlight resilience, but the slight slowdown in annual growth reinforces the need for policy stability and supportive investment conditions across the euro area.

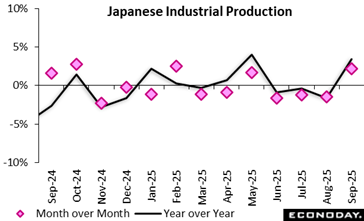

Japanese Industrial Production

Japan’s industrial output topped expectations with a 3.4 percent increase on year in September as activity bounced back from a revised 1.6 percent drop in August (previously reported at minus 1.3 percent) The median forecast looked for a 2.4 percent rise for September in a range of plus 0.8 percent to plus 3.8 percent. This was the first increase in three months.

JAPAN SEPT INDUSTRIAL OUTPUT +2.2% M/M (AUG REVISED DOWN TO -1.5% FROM -1.2%); 1ST RISE IN 3 MONTHS; MEDIAN FORECAST +1.4% (RANGE: +1.0% TO +2.4%)

JAPAN METI KEEPS VIEW: INDUSTRIAL OUTPUT TAKING ONE STEP FORWARD AND ONE STEP BACK

JAPAN METI FORECAST INDEX: OCT INDUSTRIAL OUTPUT -0.5% M/M (ADJUSTED FOR UPWARD BIAS), NOV -0.9%

JAPAN JULY-SEPT INDUSTRIAL OUTPUT -0.1% Q/Q VS. +0.4% IN APR-JUNE, -0.3% IN JAN-MAR, +0.4% IN OCT-DEC

JAPAN METI: SEPT INDUSTRIAL OUTPUT M/M RISE LED BY MANUFACTURING MACHINERY, CHEMICALS, METALS

JAPAN’S INDUSTRIAL PRODUCTION AND OTHER DATA SUGGEST JAPAN Q3 GDP TO POST 1ST CONTRACTION IN 6 QUARTERS AMID US TARIFF IMPACT AFTER Q2 SHOWED RESILIENT ECONOMIC GROWTH

US Consumer Confidence

Concerns about prices as well as future employment prospects continue to dampen U.S. consumer sentiment, with inflation in particular expected to be a drag on holiday spending compared to last year.

The Conference Board’s Consumer Confidence Index declined less than expected in October to 94.6, down from a revised 95.6 (previously 94.2) in September, and above expectations of 93.4 in the Econoday survey of forecasters.

Consumers’ assessment of current business and labor market conditions improved, while their short-term outlook for income, business, and labor market conditions remained pessimistic – remaining well below the threshold that indicates a recession ahead.

“Consumers’ view of current business conditions inched upward, while their appraisal of current job availability improved for the first time since December 2024,” the report said. “Consumers were a bit more pessimistic about future job availability and future business conditions while optimism about future income retreated slightly.”

Higher prices remain top of mind, clouding views of the economy, while there were less mentions of tariffs, but remain at an elevated level. “Mentions of jobs and employment eased somewhat after picking up in September… . References to US politics were up notably, with the ongoing government shutdown mentioned multiple times as a key concern,” the Conference board said.

Average one-year inflation expectations rose to 5.9 percent in October from 5.8 percent in September.

The Conference Board also said the share of consumers expecting a recession over the next 12 months declined in October, but the share of those who believe the economy is already in a recession rose for the third straight month.

On a six-month moving average basis, purchasing plans for autos – both new and used – increased. Plans to buy a home shrank in October, but the six-month average is trending upwards. Plans to buy big-ticket items were mixed but changed little overall. Intentions to purchase services in the coming months improved compared to September.

Finally, preliminary data suggest that consumers’ holiday spending will be down this season compared to last year, the report said. “Most purchases are expected to take place between October and the end of the year, with November seeing the largest share of planned spending.”

US Review

FOMC Faces Tricky Balancing Act, Diverging Views

By Theresa Sheehan, Econoday Economist

The US federal government shutdown drags on, leaving the data release calendar largely empty.

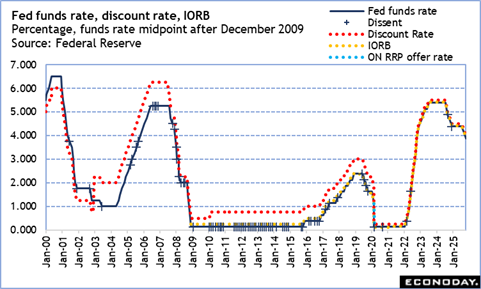

The absence of official government data reports was a particular concern this week as Fed policymakers met on October 28-29. The FOMC statement said the decision to cut the fed funds target rate range by 25 basis points to 3.75 to 4.00 percent was made with the “available” data. So far policymakers have been able to scrap together enough reliable data and good anecdotal evidence that the decision could be made with reasonable confidence.

However, Chair Jerome Powell was more emphatic than usual in saying that monetary policy is not on a predetermined path and that present conditions make that particularly true. Not only will the FOMC have a dearth of hard data to deal with but it also must assess the effects of the shutdown on the US economy. Powell mentioned the Fed’s Beige Book more than once as a source of information about the state of the economy between meetings. He expressed confidence that the FOMC would have enough data from private and public sources to set policy in December. But he also gave a warning that divergent “strong” opinions about the next steps in monetary policy should not be given too much weight until the FOMC next sits around the table to deliberate.

There were dissents in the FOMC vote in two different directions. Governor Miran wanted a 50 basis point cut while Cleveland Fed President Jeffrey Schmid wanted no change in rates. This is unusual and has not happened since the September 18, 2019 meeting when Kansas City Fed President Esther George and Boston Fed President Eric Rosengren wanted no cut in rates and St. Louis Fed President James Bullard wanted a 50 basis point cut.

The bifurcated dissent in the vote of the October meeting point to the challenges in taking a balanced approach to setting monetary policy. Some FOMC participants are leaning towards being more hawkish on inflation and keeping rates steady until it is clear that current upward price pressures are not getting entrenched. There are clearly a majority of centrists who favor the base case that once the effects of tariffs are priced in that disinflation will resume for goods. Some are more concerned about the overall weakening of the labor market where shrinking labor supply has resulted in less hiring while layoff activity has picked up slightly. As Powell has said several times, there is no risk-free path through the conflicting demands on the dual mandate.