Last Week: Eurozone Inflation Tops ECB Target: Japan’s Retail Sales Fall Short

Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

Euro area inflation edged higher in September 2025 at 2.2 percent, up from 2.0 percent in August. The rise keeps inflation above the European Central Bank’s 2 percent target, reflecting persistent price pressures in key sectors despite easing energy costs.

Services remained the main driver, accelerating slightly to 3.2 percent, underscoring ongoing wage pressures and robust demand in areas like travel and hospitality. Food, alcohol, and tobacco inflation softened to 3.0 percent but continues to weigh heavily on households, particularly lower-income groups. Non-energy industrial goods held steady at 0.8 percent, signalling subdued pricing power in consumer goods. Meanwhile, energy prices contracted by just 0.4 percent, a sharp moderation from August’s 2.0 percent decline, suggesting that the recent relief from falling energy costs may be fading.

Regionally, headline inflation rose in Germany (2.4 percent after 2.1 percent), France (1.1 percent after 0.8 percent), Spain (3.0 percent after 2.7 percent) and Italy (1.8 percent after 1.6 percent).

In essence, while headline inflation remains relatively contained, underlying components reveal persistent stickiness, particularly in services. The September uptick reinforces expectations that the ECB will remain guarded on rate cuts, prioritising inflation stability over growth concerns in the near term.

Demand

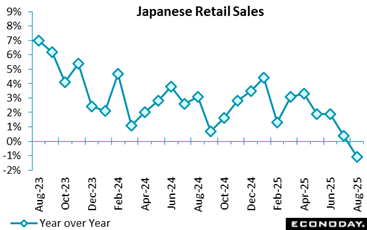

Japan’s retail sales dropped shockingly by 1.1 percent on year in August, the first decline in 41 months, and much worse than the 0.8 percent increase anticipated in the Econoday consensus. July was revised to show a 0.4 percent rise compared with the 0.3 percent previously reported.

JAPAN AUG RETAIL SALES RARE Y/Y DROP SHOWS IT WAS NOT SAFE TO GO SHOPPING DURING PEAK OF SEVERE, FATAL HEAT WAVE

JAPAN AUG RETAIL SALES -1.1% M/M (JULY -1.6%); MEDIAN FORECAST +1.2% (RANGE: +0.7% TO +1.4%)

JAPAN AUG RETAIL SALES Y/Y FALL LED BY AUTOS AFTER RECOVERY FROM 2024 SLUMP CAUSED BY TOYOTA SAFETY SCANDAL; DEPARTMENT STORES, FOOD/BEVERAGES AS PEOPLE STAYED HOME AMID EXTREME HEAT WAVE

JAPAN AUG RETAIL SALES: ELECTRONIC APPLIANCES (AIR CONDITIONERS, FANS), DRUGS, COSMETICS REMAIN STRONG.

Germany’s retail sector showed that turnover slipped 0.2 percent in real terms compared with July. This follows a revised 0.5 percent decline in July, pointing to two consecutive months of contraction. Yet, year-over-year data offers a more positive view as sales were 1.8 percent higher in real terms than in August 2024, signalling that consumer demand remains sturdier than the monthly dip suggests.

Food retail provided a modest boost, rising 0.6 percent month-over-month, though sales were still 0.6 percent lower than last year in real terms, evidence of inflation’s squeeze on purchasing power. Non-food retail painted the reverse picture, down 1.0 percent from July but up 3.2 percent compared with August 2024, hinting at resilience in discretionary spending.

The sharpest monthly fall came from internet and mail-order trade, down 2.0 percent, yet this channel still recorded an impressive 7.4 percent annual increase, confirming its role as a long-term growth driver.

In essence, August reflects a cautious retail landscape as households are spending, but inflationary pressures and shifting consumption habits continue to shape outcomes. With online trade thriving and non-food sales showing resilience, the sector remains adaptive even in the face of short-term weakness.

Production

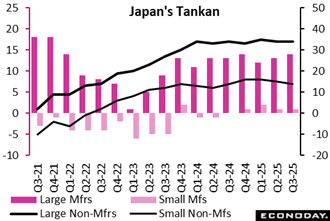

The Bank of Japan’s Tankan large manufacturer sentiment index improved to 14 in the September quarter from 13 in the June quarter but missed the median forecast of 15.

BOJ SEPT TANKAN SHOWS LARGE MFG SENTIMENT EDGES UP IN LIGHT OF US TRADE DEALS WITH JAPAN BUT MANY FIRMS CAUTIOUS FOR DEC AS TARIFF IMPACT TO EMERGE

BOJ SEPT TANKAN BIG FIRMS: AUTO INDUSTRY ONLY SLIGHTLY BEARISH ABOUT DEC SENTIMENT, STEEL MILLS SEE STABLE BUSINESS AFTER SLUMP

BOJ SEPT TANKAN LARGE NON-MANUFACTURER SENTIMENT INDEX AT 34 (JUNE 34); MEDIAN FORECAST 33

BOJ SEPT TANKAN LARGE NON-MFG SENTIMENT FLAT AS SENTIMENT AMONG HOTELS, RESTAURANTS PLUNGES AMID RISING COSTS, SLOWER INBOUND SPENDING

BOJ SEPT TANKAN: LABOR SHORTAGES DEEPEN ACROSS SECTORS, SEEN GETTING WORSE IN DEC, PARTICULARLY AMONG SMALLER FIRMS

BOJ SEPT TANKAN: MANY FIRMS SEE CONTINUED DROPS IN SALES PRICES, COST AFTER REPORTING FASTER FALL IN JUNE; MIXED OVER DEC FORECAST

BOJ SEPT TANKAN SMALLER MANUFACTURER SENTIMENT INDEX AT 1 (JUNE 1); MEDIAN FORECAST 2

BOJ SEPT TANKAN SMALLER NON-MANUFACTURER SENTIMENT INDEX 14 (JUNE 15); MEDIAN FORECAST 14

CAPEX

BOJ SEPT TANKAN: LARGE FIRM FISCAL 2025 COMBINED CAPEX PLANS +12.5% Y/Y (JUNE +11.5, MAR +3.1%); MEDIAN FORECAST +11.3%

BOJ SEPT TANKAN: SMALLER FIRM FISCAL 2025 COMBINED CAPEX PLANS -2.3% Y/Y (JUNE -5.6%, MAR -10.0%); MEDIAN FORECAST -1.5%

PRICES

BOJ SEPT TANKAN: MAJOR MANUFACTURERS SEE INFLATION AT 2.0% A YEAR FROM NOW VS. 2.1% FORECAST IN JUNE SURVEY

BOJ SEPT TANKAN: MAJOR MANUFACTURERS SEE INFLATION AT 2.0% IN 3 YEARS FROM NOW VS. 2.0% FORECAST IN JUNE SURVEY

BOJ SEPT TANKAN: MAJOR MANUFACTURERS SEE INFLATION AT 1.9% IN 5 YEARS FROM NOW VS. 1.9% FORECAST IN JUNE SURVEY

Business Surveys

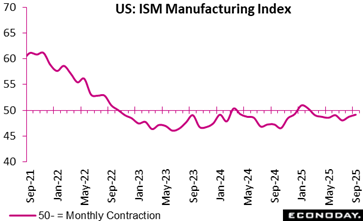

The ISM manufacturing index is very close to expectations at 49.1 in September versus the 49.0 consensus, and up marginally from 48.7 in August, all pointing to continued slow contraction in business activity. An improvement in production accounts for most of the rise but production growth looks to be fleeting.

New orders ticks down to 48.9 from 51.4, which bodes poorly for sustaining the uptick in production to 51.0 in September from 47.8 in August. Employment continues to contract at 45.3 versus 43.8. Prices paid remain highly pressured at 61.9 versus 637 in August.

On the trade front, tariffs continue to bite with new export orders in the tank at 43.0 versus 47.6 and imports at 44.7 versus 46.0.

US Review

US Jobs Report Painfully Absent with Government Shutdown

By Theresa Sheehan, Econoday Economist

That partial shutdown of the US federal government that began on October 1 interrupts the release of the data reports. While disruptions are generally minor in the first few days of the loss of the data releases, the lack of the monthly employment report for September does leave a big hole.

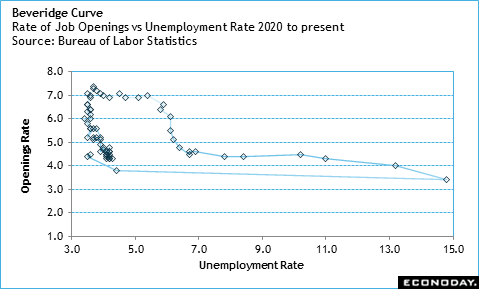

There is no report more important for assessing the health of the US economy and its direction. The lack of it comes at a time when the condition of the labor market reflects slow hiring and fewer job openings, although layoff activity remains relatively low through August as seen in the report on job openings and labor turnover (JOLTS) release on September 30. The Beveridge Curve – the rate of job openings versus the national unemployment rate – points to conditions somewhat weaker than just before the pandemic, but which are not much changed in recent months.

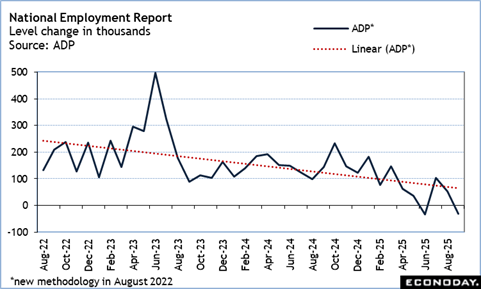

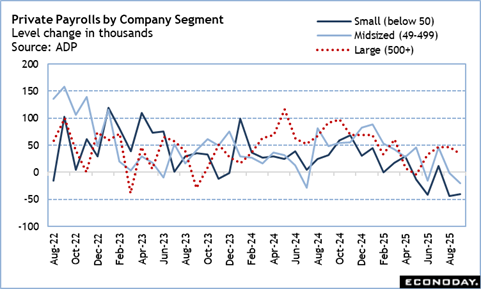

The best data currently available for payrolls is the ADP national employment report for September which was released October 1. The report included annual revisions which have put private payroll growth lower than previously reported with the inclusion of revised data from the BLS. Private payrolls are now down for a second month in a row. The pace appears to be accelerating. Cuts in payrolls are broad-based – although not universal. Interestingly, payrolls are down for small- to medium-sized firms where large companies (500+ employees) have added workers. It appears that the crackdown in immigration may mean many companies that rely on immigrant labor have lost needed workers, not cut jobs because of economic conditions. Larger companies may be moving to take advantage of increased labor supply among workers with the right skills and/or experience.