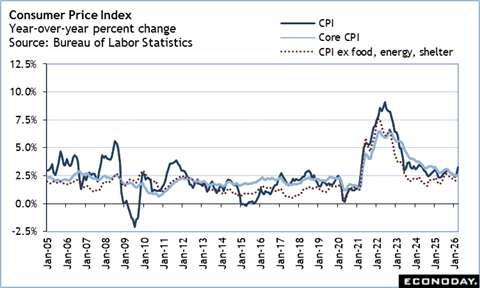

The March CPI report came in about as expected with a surge in energy prices driving the year-over-year increase to 3.3 percent, the highest since up 3.3 percent in May 2024. On the other hand, the core CPI annual increase was 2.6 percent, on trend with the data since November 2024. The CPI less energy only is up 0.2 percent in March from February and up 2.6 percent compared to March 2024.

The 10.9 percent hike in energy prices in March from February is a shock created by the war on Iran started on February 28. The increase is likely a one-off unless the conflict escalates. Although Fed policymakers will “look through” a temporary upward spike in price pressures, they will also have to consider that prices may not come down immediately and higher costs will ripple through the economy, especially for the transportation sector. Higher energy prices will also have a chilling effect on household discretionary spending that could impede economic growth.

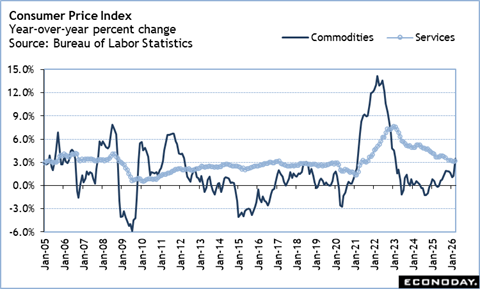

In meantime, the FOMC will have to consider what the fundamentals are in the economy as related to the mandate for price stability and the 2 percent inflation objective. Commodities prices had been the mainstay of disinflation but started rising again early in 2025. The March price shock does not change that these are rising modestly. Service prices had been inching lower since the peak in early 2023 but returning to a sustainable pace consistent with price stability has yet to be achieved.

The March CPI report is a setback for disinflation even if it is short-lived.