The February 13 week includes two reports delayed by the brief government shutdown of February 2-3 and which are critical to the outlook for Federal Reserve monetary policy. Too much emphasis should not be placed on these reports as policymakers will get the February employment report on March 6 at 8:30 ET and consumer price indexes for February at 8:30 ET on Wednesday, March 11 at 8:30 ET. The next FOMC is Tuesday and Wednesday, March 17-18. Both reports included annual revisions back five years.

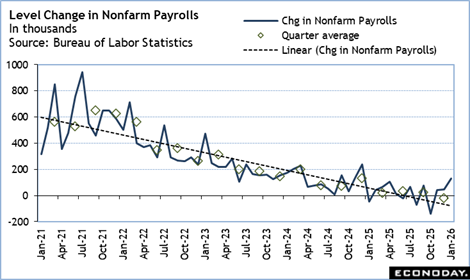

The monthly employment report included annual revisions back five years and the expected large downward revisions for 2025 which totaled 898,000 fewer payroll gains than previously reported (original estimate was down 911,000).

Nonfarm payrolls registered a solid 130,000 increase in January with private payrolls up 172,000 and government jobs down 42,000. However, job gains were mostly in a few narrow sectors as they have been in recent months. These occurred in healthcare and social assistance (123,500), professional and business services (up 34,000), and construction (up 33,000). Payroll employment changed little in 2025 (+15,000 per month on average). The unemployment rate ticked down a tenth to 4.3 percent in January. The January data extends the story of soft hiring with a few exceptions while job losses are relatively few and mainly from industries eliminating less profitable locations and services and/or adopting AI tools.

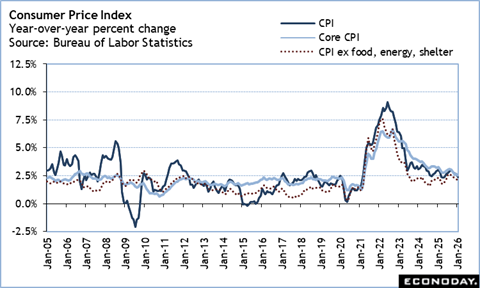

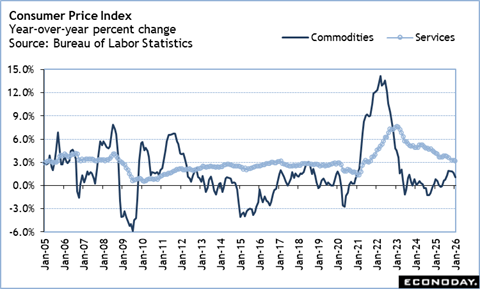

Although the PCE deflator is the Fed’s preferred measure of inflation, the CPI is also important to setting monetary policy. The CPI is up 2.4 percent in January from a year ago, moderating from the annual change of up 2.7 percent in December. The core CPI is up 2.5 percent year-over-year in January, down a tenth from up 2.6 in December. Price pressures in 2025 were mainly from the introduction of higher tariffs that were passed through the supply chain. The January data suggests that most of the higher costs for imported goods have reached consumers or soon will. The main impact was seen in increased costs for commodities while services prices were less affected. Price pressures are moderating for commodities fairly quickly while services are taking a slower path. The CPI for commodities is up 1.0 percent in January from a year ago compared to up 1.7 percent in December. The CPI for services is up 3.2 percent from January 2025 while the December year-over-year increase is 3.3 percent.