Kevin Warsh was sworn in on May 22 as a governor and 17th chair of the Federal Reserve with less than a month before his first FOMC meeting as chair on June 16-17.

At his Senate Banking Committee nomination hearing, Warsh fiercely insisted he would maintain an independent central bank in response to harsh questions from committee members. Failures in competence and probity of a numerous Trump past appointees means that any nomination was going to get extra scrutiny. The Fed chair’s leadership and integrity are critical to ensuring that the financial system remains healthy and resilient, and that the dual mandate of maximum employment and price stability are achieved with appropriate monetary policy decisions. There is no reason to doubt Warsh’s assertions. What remains to be seen is how he approaches keeping the Fed independent from political interference.

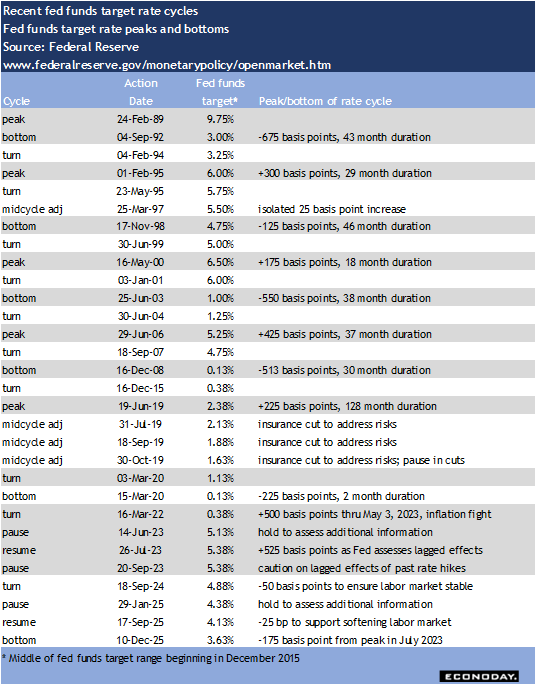

Warsh returns to the Fed at a time when the next steps in monetary policy are not necessarily clear. FOMC participants are unusually divided in their opinions, although it is more a matter of degree of concern about the risks that differing on the nature of the risks. Warsh will have an opportunity to outline his take on the economy and monetary policy when he delivers his first semiannual monetary policy in June or July. It is likely that it will be scheduled sooner rather than later. The Senate Banking Committee and House Financial Services Committee both faithed to schedule the normal testimony for February and no biannual monetary policy report to Congress was issued.

Warsh takes over as Fed Chair at a time when FOMC participants’ sentiment is turning more hawkish on inflation. Inflation reports for April confirm that consumer prices are on the rise as impacts from higher energy costs pass through from the producer level and that producers have yet to see any relief from upward pressure. Measures of inflation expectations for the near term are substantially elevated and those for the medium- and long-term are inching up. As long as the dashboard of employment data remains consistent with a labor market where supply and demand are roughly in balance, the outlook for monetary policy is for no easing in rates and slightly toward a mid-term adjustment higher to ensure that inflation does not become entrenched.