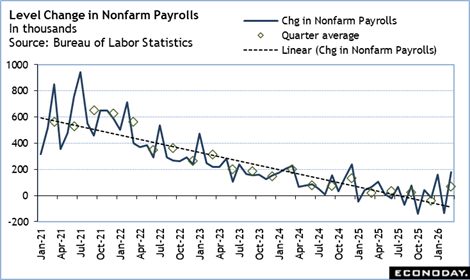

On the surface, the 178,000 increase in March nonfarm payrolls looks like a strong comeback from the 133,000 decline in February. However, the details of the report suggest that job growth remains confined to a few industries in the private sector. Moreover, the March payroll gains are driven by special factors that provide only a one-month boost. March got a push higher from the resolution of the nurses’ strike in New York added back in a substantial number of workers in health care, a rebound from the winter weather conditions that predominated in late January and early February, and hiring in sectors associated with travel during the spring break holidays.

Payrolls in health care and social assistance are up 89,900 in March after declining 27,800 in February. There were 31,000 union nurses on a strike that was resolved in February and brought these workers back on payroll. Cold weather kept outdoor construction activity in check, but warmer temperatures meant builders are adding workers. Construction rose 26,000 in March. Many school districts scheduled spring break at the end of March with Passover beginning on April 1 and Easter on April 5. Leisure and hospitality jobs are up 44,000 in March.

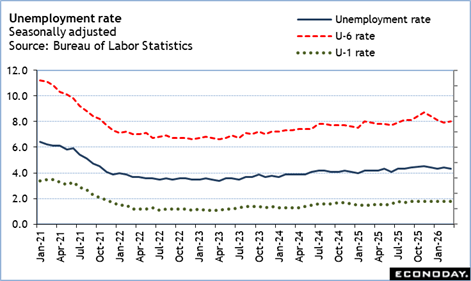

Payroll gains average 68,000 in the first quarter 2026 compared to a decrease of 39,000 in the fourth quarter 2025. While this starts the year off on a positive note, it is too early to say that the “low hire, no fire” conditions in the labor market are changing. A dip in the unemployment rate to 4.3 percent in March from 4.4 percent is from a decrease in the size of the labor force, not expansive hiring. The participation rate of 61.9 percent points to a lack of new entrants in the labor market and a withdrawal of others. Some workers may be retiring, some may be finding less economic incentive to work, however a lack of immigrant labor is also a factor.

When the FOMC next meets on April 28-29, it will probably find that underlying conditions and risks are little changed over the intermeeting period for the maximum employment side of the Fed’s dual mandate. The balance between labor supply and demand remains roughly equal and not in immediate danger of shifting to the downside. Nonetheless, the war on Iran is lengthening without a clear end in sight. Fed policymakers are going to tread carefully while uncertainty is heightened.