Last week’s news was dominated by the prospect that President Trump would order an invasion of Greenland and raise punitive tariffs on European allies if they opposed its annexation by the US. In the end, Trump backed down from the most aggressive of his threats, but the situation remains unclear.

Most of the data in the week only brings it up through the end of 2025. Catchup continues after the government shutdown of October 1-November 12, although the gaps are fewer, especially for the labor market and major inflation indicators. This is particularly welcome with the January 27-28 FOMC meeting on the near horizon. One of the biggest challenges in setting monetary policy during the shutdown and the months afterward was a lack of current data.

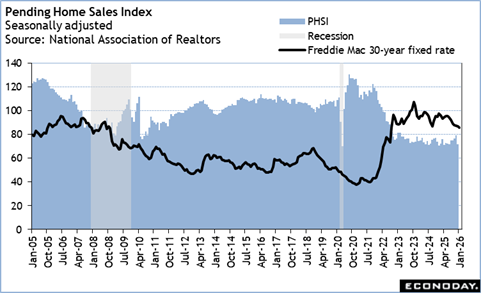

The one report that held some surprise in the week was the NAR’s pending home sales index for December. The Econoday survey of forecasters anticipated an index of 79.2 which would have been the same as the November reading. Instead, the index dropped 9.3 percent to 71.8 in December and was down 3.0 percent from a year earlier. Some of this may have been due to difficulty in seasonally adjusting the index for December. December can feel the impact of holidays, vacations, and/or weather. The decline was even more of a surprise given the downturn in mortgage interest rates. The monthly average for a Freddie Mac 30-year fixed rate mortgage was down to 6.19 percent in December, a low not seen in over three years.

However, the decision to buy a home isn’t just the mortgage rate. Price and available inventory figure in as well. And then there’s weak consumer confidence that has gotten further jolts in January from geopolitical events. Potential homebuyers will want a less uncertain future before committing to a purchase. Memories of the housing market crash in 2007 may be nearly 20 years old, but the echoes are still there.