The big data for the week comes with the numbers on personal income and spending, and the PCE deflator – currently the Fed’s preferred measure of inflation.

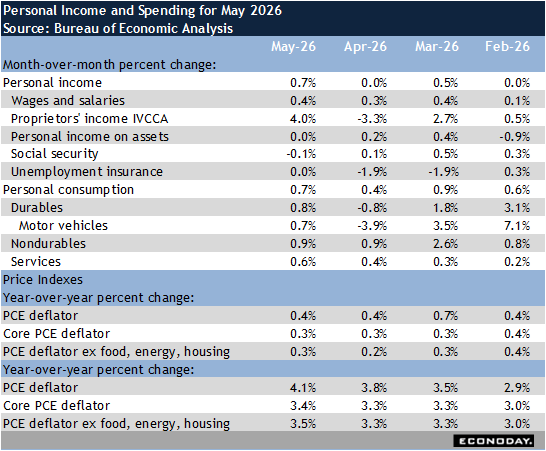

In May, personal income rose 0.7 percent after a flat reading in April. However, the increase in wages and salaries was a trend-like 0.4 percent for May. The big gain in income was from a 4.0 percent rise in proprietors’ income, rebounding from a decline of 3.3 percent in the prior month. Personal income on assets was unchanged in May from April after a small 0.2 percent increase in April from March.

Personal consumption in May was also up 0.7 percent after rising 0.4 percent in April and 0.9 percent in March. March had widespread spending increases related to higher oil prices after the onset of the war on Iran on February 28. The upward momentum eased off in April but May’s numbers point to pass through of higher costs as energy prices remain elevated. Spending on durables was up 0.8% in May, with nondurables up 9.0 percent and services up 0.6 percent.

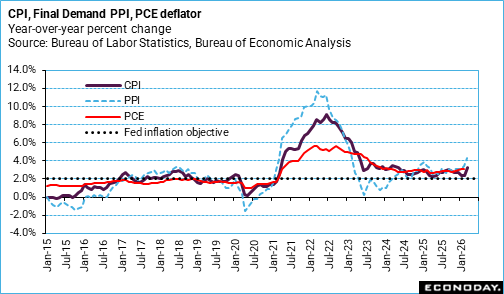

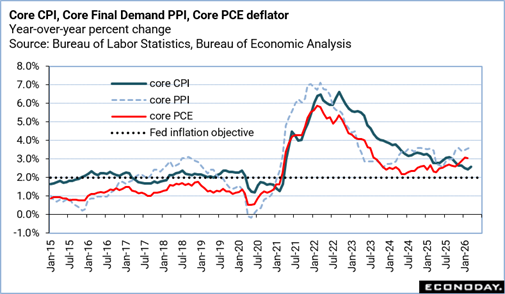

While month-over-month increases in the PCE deflator are show little change, the year-over-year increase is inching higher. The PCE deflator is up 4.1 percent in May from a year ago and the highest since up 4.5 percent in April 2023. The core PCE deflator is up 3.4 percent in May, its highest since up 3.5 percent in October 2023. Inflation is moving in the wrong direction. Whether it will start to come down again depends in large part on getting a lasting cease-fire in the Middle East and normalizing oil supplies. In the meantime, Fed policymakers will have to guard against inflation becoming entrenched. It likely rules out a rate cut any time soon, but whether a majority of FOMC voters will want a rate hike remains to be seen.

Fedwatchers will be waiting for the dates Chair Kevin Warsh’s first semiannual monetary policy testimony which will be sometime after the July 4 congressional recess.