While survey data should be viewed with caution as at times reflecting opinion more than reality, the April numbers in the University of Michigan’s survey of consumers are flashing some warning lights about the US economy.

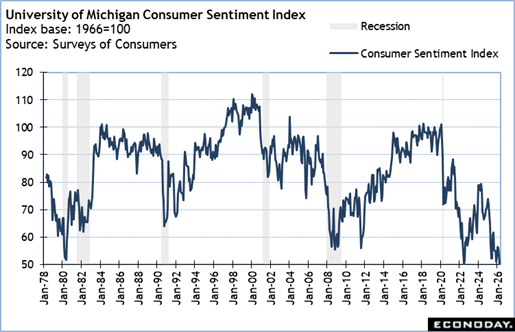

The consumer sentiment index reached a series low of 49.8 in April, although it was revised up from the preliminary 47.6. This reflects the worst sentiment among consumers since the series began in 1978 and during any period of recession including the Great Recession (December 2007-June 2009). Readings of consumer confidence in the normal low-to-high range do not necessarily means a change in consumer behavior. But at the extremes – particularly at the low end – consumers do modify their spending plans.

The index for current conditions is down to 52.5 in April from 55.8 in March but has been lower in recent months at 51.1 and 50.4 in November and December 2025. However, confidence in current conditions has been much weaker overall since late 2025.

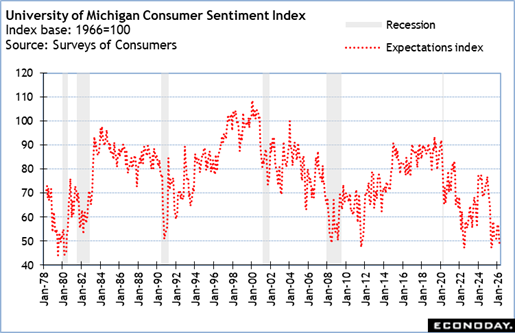

The expectations index – roughly for conditions six months from now – is down to 48.1 in April from 51.7 March. This is the lowest reading since 47.9 in June 2025. The future hasn’t looked bright since early 2025 but there’s a growing recession concern among consumers.

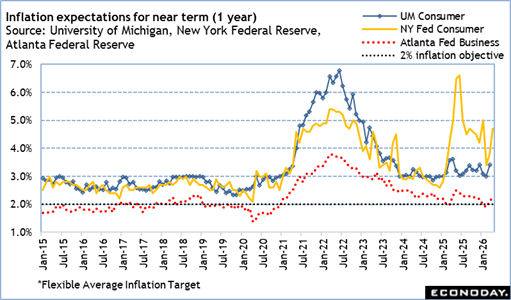

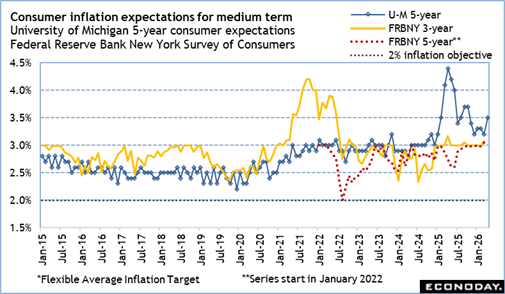

Some of the fall in consumer sentiment can be laid at the door of inflation expectations. The measure for 1-year inflation expectations jumps to 4.7 percent in April from 3.8 percent in March, reversing the downward trend of the prior two months. Higher gasoline prices often spark short-term inflation expectations. However, the 5-year inflation expectations measure is up to 3.5 percent in April, wiping out the downward trajectory from 3.7 percent in October 2025.

Fed policymakers will not overreact to the swing higher in inflation expectations in a single month but they will also not ignore the potential for expectations to come unanchored if its credibility as an inflation fighter is called into question. These sorts of numbers are likely to encourage the FOMC to stay on hold regarding the fed funds target rate and maybe even increase the potential for a rate hike rather than a rate cut.