By Theresa Sheehan, Econoday Economist

The release of the November CPI report on Thursday without the data for October made it virtually impossible to form any useful picture of the state of inflation and the inflation outlook. There were no month-over-month percent changes for November or October except for prices for gasoline.

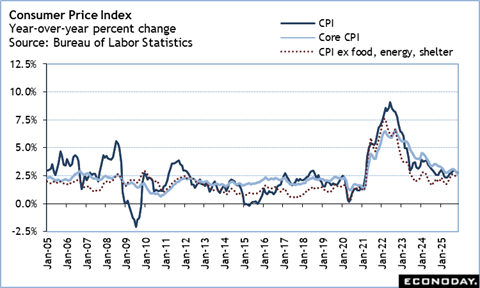

The year-over-year rise in the CPI in November is 2.7 percent, a decline when compared up 3.0 percent in September. The core CPI is up 2.6 percent in November compared to up 3.0 percent in September.

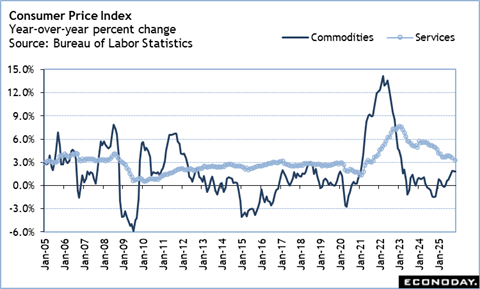

The year-over-year increase in the CPI for commodities remains more elevated at up 1.8 percent in November compared to 1.9 percent in September. Commodities prices have been the main source of price inflation in recent months. The CPI for services continues to reflect deflation, although the 3.2 percent annual increase in November remains what the FOMC would term as elevated. The services CPI for September is up 3.6 percent. Notably, the CPI for shelter costs – which accounts for about 1/3 of the CPI basket – continues to trend lower. The annual increase for the CPI for shelter is 3.0 percent in November compared to 3.6 percent in September.

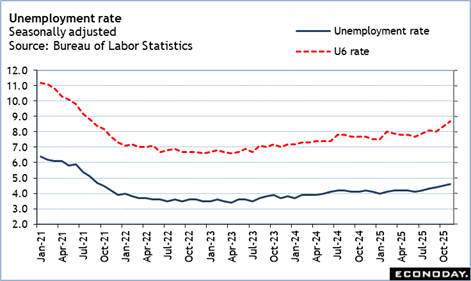

Missing data in October had an impact on the monthly employment report for November. The household survey did not take place for October due to the government shutdown and the BLS did not attempt to collect the data. The national unemployment rate rose to 4.6 percent in November compared to 4.4 percent in September. Making an educated guess, the unemployment rate has been rising about one-tenth a month since 4.1 percent in June. The November rate is the highest since 4.7 percent in September 2021.

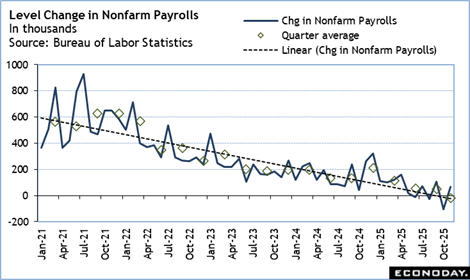

The increase of 64,000 in nonfarm payrolls in November comes after a decline of 105,000 in October – mainly from idled workers during the federal government shutdown – and an increase of 108,000 in September. Looking past the month-to-month variation, hiring is trending lower steadily. Moreover, it is largely confined to a few narrow sectors like construction and healthcare where skilled workers remain in high demand.

The underlying story appears to be that there is less hiring and more job cutting, although outright job losses remain relatively low. The labor market is continuing to rebalance after the massive layoffs in federal employees earlier this year, the rapid adoption of AI technology, consolidation in the retail sector, businesses figuring out how to operate efficiently in the new tariff environment, and the impact of heightened uncertainty on consumers and businesses.