This week saw the release of the December CPI report, and the November numbers for final-demand PPI and the import and export price indexes. The gap in data collection for October still presents problems in assessing the state of current inflation. However, the year-over-year picture is more complete.

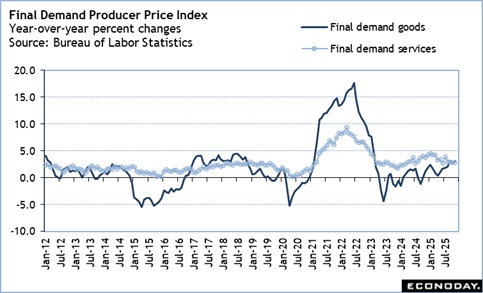

Upward price pressures for consumers have plateaued but remain elevated. Producers face a mixed picture on price pressures with the overall underlying trend still one that points to more pass-through of costs to consumers in the near future. Prices for imports are complicated with oil prices – which are in US dollars – bringing the costs of total imports lower while a weaker dollar is making nonfuel imports more expensive.

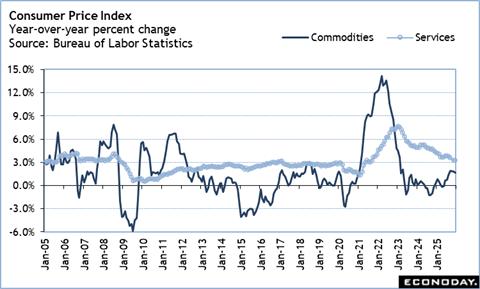

Behind the movements are a change in momentum for services and commodities. Declining commodities costs had powered earlier disinflation until the imposition of high tariffs on imports drove these up again. At the same time, the slow improvement in services prices had finally begun steady, meaningful deceleration until the tariffs hit. Taken together – disinflation is on hold until the tariff-related higher costs move fully through the economy. This may be nearly done or it may take some months. In addressing the price stability side of the Fed’s dual mandate, policymakers will have a tough call in assessing just how close inflation is to the 2 percent objective and just how long it might take to get there.

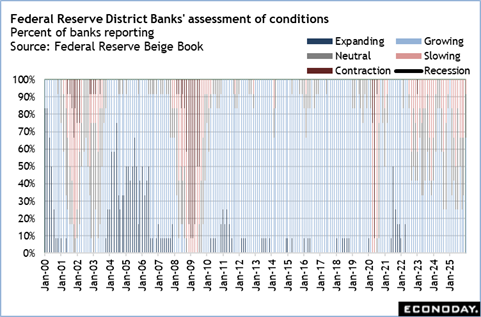

Between the recent reports about the labor market and the contents of the latest Beige Book, the FOMC will have less reason for concern about deterioration in the labor market. The labor market isn’t thriving in the traditional sense, but unemployment remains low even as robust hiring is limited to a few narrow sectors. The US economy continues to expand at a modest pace, although growth is not uniform and the outlook is uncertain.