Edited by Simisola Fagbola, Econoday Economist

Here are the key economic indicators and events in the week past.

The Economy

Inflation

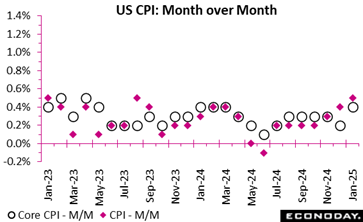

The Consumer Price Index in January jumped 0.5 percent, following a 0.4 percent increase in December, and a 0.3 percent rise in November. This compares to expectations for a 0.3 percent rise in the Econoday survey of forecasters. The overall monthly rise in consumer prices is the largest spike since August 2023.

The Consumer Price Index in January jumped 0.5 percent, following a 0.4 percent increase in December, and a 0.3 percent rise in November. This compares to expectations for a 0.3 percent rise in the Econoday survey of forecasters. The overall monthly rise in consumer prices is the largest spike since August 2023.

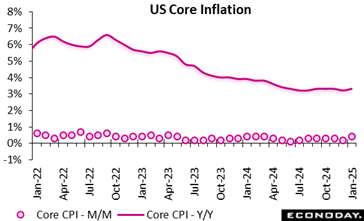

Over the last 12 months, consumer prices are up 3 percent, compared to a 2.9 percent year-over-year rise in December. Expectations were for a 2.9 percent increase.

Over the last 12 months, consumer prices are up 3 percent, compared to a 2.9 percent year-over-year rise in December. Expectations were for a 2.9 percent increase.

Core CPI, excluding food and energy prices, rose 0.4 percent, picking up the pace after rising by 0.2 percent in December, and +0.3 percent in November. Consumer prices less food and energy rose 3.3 percent from the January 2024, after rising by 3.2 percent on an annual basis in December.

The data resurrects concerns that inflation is flaring up again, even before the effects of recently announced higher tariffs feed through to consumer prices. This underpins the Federal Reserve’s decision to hit pause on rate cuts for the foreseeable future.

After rising by 0.3 percent in December, shelter costs rose by 0.4 percent in January (and are up 4.4 percent year-over-year). Food prices increased by 0.4 percent, building on a 0.3 percent rise in December, as grocery prices saw a 0.5 percent spike, and restaurant prices rose by 0.2 percent. Energy costs jumped 1.1 percent over the month, after surging 2.4 percent in December.

Energy prices are up 1 percent year-over-year, following a 0.5 percent decline for the 12 months ending December. Food prices increased 2.5 percent compared to January 2024, the same rate as in December.

GDP

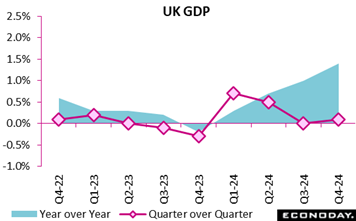

The UK economy grew slightly by 0.1 percent in the final quarter of 2024, precisely a percentage point above consensus forecasts for the quarter and marking a return to growth after a stagnant third quarter. While modest, this performance contributed to an annual GDP expansion of 1.4 per cent in the fourth quarter compared to the 2023 fourth quarter, indicating a slow but sustained recovery and 0.3 percentage points above the estimated forecast for the quarter.

The UK economy grew slightly by 0.1 percent in the final quarter of 2024, precisely a percentage point above consensus forecasts for the quarter and marking a return to growth after a stagnant third quarter. While modest, this performance contributed to an annual GDP expansion of 1.4 per cent in the fourth quarter compared to the 2023 fourth quarter, indicating a slow but sustained recovery and 0.3 percentage points above the estimated forecast for the quarter.

The services sector remained the backbone of the economy, expanding by 0.2 percent, while construction saw a solid 0.5 percent increase. In contrast, production output fell by 0.8 percent, reinforcing manufacturing’s ongoing struggles. On the expenditure side, net trade and capital investment declines were offset by a notable increase in inventories, suggesting businesses stockpiled goods, possibly in anticipation of future demand shifts.

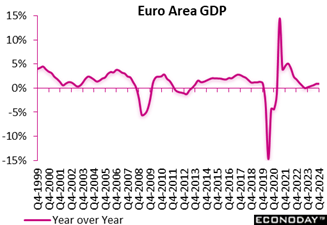

The euro area’s GDP growth in the fourth quarter of 2024 grew slightly by 0.1 percent, down from 0.4 percent growth in the third quarter of 2024. This signaled a deceleration, likely driven by weakened consumer demand and external uncertainties. However, year-over-year growth remained stable at 0.9 percent, in line with the third quarter of 2024, suggesting a degree of resilience despite prevailing economic challenges. The stagnation in quarterly expansion raises concerns about whether the euro area can sustain growth amid geopolitical risks and inflationary pressures.

The euro area’s GDP growth in the fourth quarter of 2024 grew slightly by 0.1 percent, down from 0.4 percent growth in the third quarter of 2024. This signaled a deceleration, likely driven by weakened consumer demand and external uncertainties. However, year-over-year growth remained stable at 0.9 percent, in line with the third quarter of 2024, suggesting a degree of resilience despite prevailing economic challenges. The stagnation in quarterly expansion raises concerns about whether the euro area can sustain growth amid geopolitical risks and inflationary pressures.

While the economy avoids contraction, this sluggish pace leaves little room for policy complacency. The ECB may face renewed pressure to balance monetary policy adjustments with economic stability. Looking ahead, fiscal stimulus or targeted interventions may be necessary to inject dynamism into the region’s growth trajectory.

Demand

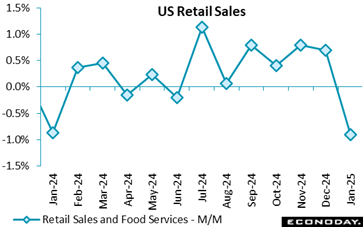

U.S. January retail sales fell by 0.9 percent to start the year, a step backwards after the revised 0.7 percent monthly increase (previously +0.4 percent) reported for December, and a much larger decline than the 0.1 percent drop expected in the Econoday survey of forecasters.

U.S. January retail sales fell by 0.9 percent to start the year, a step backwards after the revised 0.7 percent monthly increase (previously +0.4 percent) reported for December, and a much larger decline than the 0.1 percent drop expected in the Econoday survey of forecasters.

There were broad-based declines, with online sales down almost 2 percent, auto sales falling by 3 percent, furniture stores -1.7 percent, building material as well as supplies stores -1.3 percent, and sporting goods -4.6 percent.

Severe winter storms were likely a factor in the drop in retail sales activity, although this data still underlines the “balance of risks” to the economy that Fed officials continue to emphasize.

Compared to a year ago, retail sales are up 4.2 percent, compared to December’s revised 4.4 percent jump (previously +3.9 percent).

Excluding gasoline, retail sales contracted by 1 percent, negating December’s 0.6 percent rise, and are up 4.4 percent from January 2024 vs. +4.8 percent on an annual basis in December.

Stripping out purchases of motor vehicles and parts, sales dipped by 0.4 percent compared to a revised 0.7 percent increase (from +0.4 percent) in December. On an annual basis, retail sales ex-autos are up by 3.7 percent, an improvement on December’s 3.4 percent rise.

Core retail sales, removing autos and gasoline sales, fell 0.5 percent last month after rising by that same rate in December (revised up from +0.4 percent), and are up 3.9 percent y/y – the same annual rate as in December.

Production

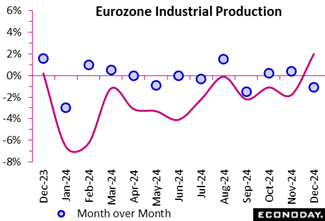

Industrial production in the euro area took a downturn in December 2024, contracting by 1.1 percent month-over-month, reversing November’s 0.4 percent growth. This decline signals renewed fragility in the industrial sector, dragging annual production down by 2.0 percent compared to December 2023. A closer look at the monthly breakdown reveals a steep drop in capital goods output (minus 2.6 percent), indicating reduced investment in machinery and equipment, a potential red flag for future productivity. Intermediate goods production also shrank (minus 1.9 percent), suggesting weaker demand in supply chains. On the upside, non-durable consumer goods surged by 5.1 percent, pointing to resilient household spending on essentials, while energy output edged up by 0.5 percent, possibly due to seasonal demand.

Industrial production in the euro area took a downturn in December 2024, contracting by 1.1 percent month-over-month, reversing November’s 0.4 percent growth. This decline signals renewed fragility in the industrial sector, dragging annual production down by 2.0 percent compared to December 2023. A closer look at the monthly breakdown reveals a steep drop in capital goods output (minus 2.6 percent), indicating reduced investment in machinery and equipment, a potential red flag for future productivity. Intermediate goods production also shrank (minus 1.9 percent), suggesting weaker demand in supply chains. On the upside, non-durable consumer goods surged by 5.1 percent, pointing to resilient household spending on essentials, while energy output edged up by 0.5 percent, possibly due to seasonal demand.

Over the year, average industrial output fell by 2.0 percent in the euro area, reflecting persistent structural challenges. The annual picture remains bleak, with capital goods plunging 8.1 percent-a worrying sign of declining business investment confidence. However, non-durable consumer goods jumped 8.3 percent, hinting at some resilience in daily consumption.

Regionally, among the top 4 economies, industrial production rose in Spain (2.6 percent after minus 0.8 percent), but fell on an annual basis in France (minus 1.3 percent after minus 1.1 percent), Italy (minus 7.1 percent after minus 1.5 percent), and Germany (minus 4.0 percent after minus 3.3 percent). With persistent contractions in core industrial sectors, the euro area faces ongoing production headwinds, requiring stronger policy support and investment incentives to stimulate recovery.

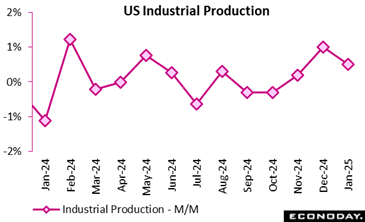

Industrial production came in stronger than expected with output up 0.5 percent on the month in January after a revised 1.0 percent rise in December (versus an increase of 0.9 percent previously reported for December). The consensus looked for a more modest 0.3 percent increase for January.

Industrial production came in stronger than expected with output up 0.5 percent on the month in January after a revised 1.0 percent rise in December (versus an increase of 0.9 percent previously reported for December). The consensus looked for a more modest 0.3 percent increase for January.

Output of aircraft and parts after the end of a strike added 0.2 percentage points to the increase in January. Even so, manufacturing was down 0.1 percent on the month, depressed by a 5.2 percent decrease in motor vehicles and parts.

On the plus side, utilities jumped by 7.2 percent on the month amid strong heating demand due to very cold weather. Mining was down 1.2 percent.

Capacity utilization rose to 77.8 percent from a revised 77.5 percent in December (previously 77.6 percent). Even with the rise, capacity remains 1.8 percentage points below its long-term average.