Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

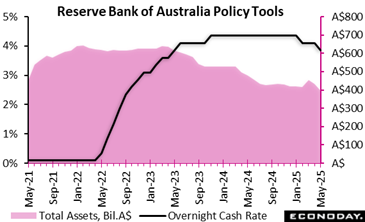

The Reserve Bank of Australia lowered its main policy rate, the cash rate, by 25 basis points from 4.10 percent to 3.85 percent at its meeting today, in line with the consensus forecast. This rate was left on hold at the RBA’s previous meeting in April after it was cut for the first time since 2020 in February. The rate decision coincided with the publication of updated economic forecasts in the quarterly Statement on Monetary Policy.

In the statement accompanying today’s decision, official noted recent declines in inflation and expressed optimism that risks to the inflation outlook had become more balanced after they were more concerned previously about upside risks. This, they judge, provides more confidence that inflation will be around the midpoint of their target range of 2 percent to 3 percent throughout much of the forecast period. However, despite ongoing tightness in the labour market, officials remain uncertain about growth prospects, reflecting both external risks and the outlook for domestic household consumption.

Reflecting these considerations, officials concluded that a rate cut was warranted today but they also stressed that the remain cautious about the outlook. They noted that monetary policy is well placed for them to “respond decisively” if external factors weigh on domestic economic conditions.

Today’s decision that a rate cut is warranted reflects the fact that officials have revised their near-term inflation forecasts lower. Headline inflation is now forecast to be 3.0 percent at end-2025, down from the previous forecast of 3.7 percent made in February, and then remain steady at 3.1 percent at mid-2026 and 2.8 percent at end-2026, little changed from the previous forecasts of 3.2 percent and 2.8 percent respectively. The forecast for the trimmed mean measure of inflation at end-2026 has also been revised slightly lower from 2.7 percent to 2.6 percent. Both measures of inflation are forecast to be at 2.6 percent mid-2027, down from 2.7 percent previously.

Officials have also revised down their growth forecasts. Australia’s economy is now forecast to expand by 2.1 percent on the year in the three months to December 2025, down from 2.4 percent previously, and by 2.2 percent in the three months to March 2026, down from 2.3 percent previously.

In the post-meeting press conference, Governor Michele Bullock confirmed that officials had briefly considered keeping rates on hold again at this meeting but had then debated between cutting policy rates by 25 or 50 basis points. Although she was non-committal about the potential for a series of rate cuts in upcoming meetings, she stressed that officials now have more scope to respond to incoming data, suggesting officials are now more open to cutting rates further if conditions allow.

Inflation

In April 2025, UK inflation accelerated more sharply than expected, with the consumer prices index (CPI) rising by 3.5 percent year-over-year from 2.6 percent in March. Month-over-month, inflation jumped 1.2 percent, compared to 0.3 percent in the previous month and 0.2 percent above the consensus forecast.

Core inflation, which strips out volatile items such as food and energy, also edged higher to 3.8 percent, indicating underlying price pressures remain persistent. Notably, prices for goods rose from 0.6 percent to 1.7 percent, while services inflation surged from 4.7 percent to 5.4 percent, driven by rising costs in housing, transport, and recreational sectors.

The broader CPIH measure, which includes owner occupiers’ housing costs, climbed to 4.1 percent from 3.4 percent annually, highlighting the role of housing in fuelling inflationary pressure. Although clothing and footwear provided some downward drag, it was insufficient to counterbalance the broad-based increases elsewhere.

These figures suggest that inflation is not only resurfacing but becoming increasingly embedded in services, which may pose challenges for monetary policy, especially if wage growth follows suit. The data may also signal potential delays in anticipated interest rate cuts, as the Bank of England weighs the risk of premature easing amid stubbornly high core and services inflation.

GDP

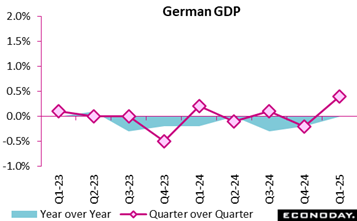

Germany’s economy expanded by 0.4 percent in the first quarter of 2025, 0.2 percent above earlier estimates. This marks the most substantial quarterly growth since the third quarter of 2022 and offers a modest sign of recovery. Manufacturing and exports led the rebound, bolstered by strong demand for pharmaceuticals and vehicles, possibly driven by pre-emptive buying amid US trade tensions. Household consumption also improved (0.5 percent), supported by warmer sentiment and rising wages, while public spending faltered due to temporary budget constraints.

Fixed investment grew by 0.9 percent, driven by gains in both machinery and construction, although year-over-year figures still reveal lingering weakness. Gross value added rose overall, with notable strength in ICT and hospitality, though finance and public services dragged down service sector growth. Employment slightly declined year-over-year, yet average working hours rose, keeping labour volume stable.

While exports surged quarter-over-quarter, annual comparisons showed a dip, revealing the fragility of Germany’s external demand. Real income gains were partly offset by rising social contributions, nudging down household savings to 13 percent. Compared to peers, Germany outpaced the EU average but lagged in year-over-year terms.

Overall, the first quarter rebound is promising, but fragile, anchored more in short-term dynamics than structural revival.

Demand

Retail sales in the UK bounced back strongly in April 2025, with volumes rising by 1.2 percent, 0.9 percent above the consensus forecast and the sharpest monthly increase since mid-2021. This momentum caps four consecutive months of growth, marking a 5.0 percent increase year-over-year, some 1.5 percentage points above the consensus forecast. Food retailers were the winners, with a 3.9 percent surge attributed to favourable weather boosting supermarket and specialty store activity. However, non-food stores saw a modest dip of 0.7 percent, reflecting a cool-off after a robust performance in March, especially in clothing and leisure categories.

Despite the digital shift in recent years, online spending slipped slightly by 0.3 percent month-over-month, nudging online sales’ share down to 26.8 percent. Still, annual growth in online value sales remained healthy at 6.1 percent, signalling sustained consumer appetite for digital channels. Notably, sales volumes have now exceeded pre-pandemic levels, suggesting renewed consumer confidence.

The retail sector’s resilience, particularly amid inflationary pressures, hints at a cautious but strengthening recovery, rooted in weather-driven footfall, seasonal demand, and tentative shifts in consumer sentiment.

International trade

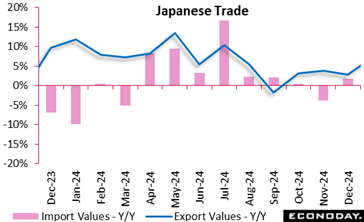

Japanese export values posted a seventh straight year-on-year rise in April but the global trade war launched by the United States led the pace of increase to decelerate further to 2.2% (vs. consensus +3.1%) from a revised 4.0% in March, 11.4% in February and 7.3% in January. Higher shipments of computer chips, food and drugs were partly offset by declines in automobiles as well as iron and steel, hit by Trump tariffs on imports. Exports of ships also dropped.

Import values slipped back 2.2% (vs. consensus -3.9%) after rebounding a revised 1.8% in March on a 0.7% dip the previous month. The decrease was led by lower purchases of coal, crude oil and aircraft as seen the previous month. The prices for crude oil and other materials have eased on dimmer global growth prospects while a firmer yen on waning U.S. currency safe-haven status has lowered import costs.

The trade balance marked a deficit of ¥115.85 billion (vs. consensus ¥191.30 billion in surplus) for the first shortfall in three months (the eighth in 12 months) following a revised ¥559.43 billion surplus in March and narrowing from a ¥504.69 billion deficit seen in April 2024. The deficit was not entirely unexpected. NLI Institute Chief Economist Taro Saito, who often accurately predicts trade figures, had called for a deficit of ¥140.50 billion, which was at the bottom of the economist forecast range, with the highest being a surplus of ¥343.80 billion.

Exports to the United States, which is the largest market for Japanese exports, dipped 1.8% on year after +3.1% in March, marking their first drop in four months (down for a fifth straight month through December 2024).

Those to the European Union slipped 5.2% (vs. -1.1% the previous month) for the fourth drop in a row while shipments to China fell 0.6% after falling 4.8% in March and marking the first gain in three months in February (vs. +14.1%).

Housing

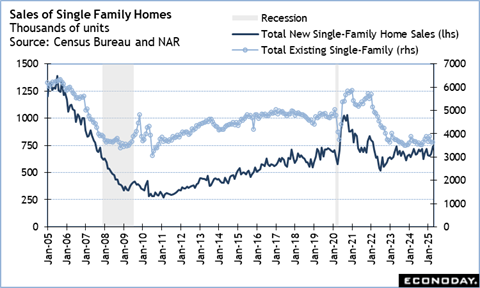

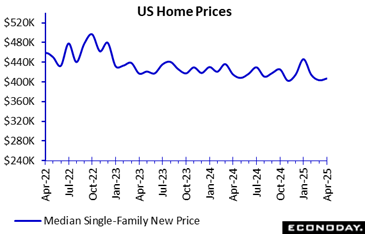

US sales of new single-family homes in April are up 10.9 percent to a 743,000 seasonally adjusted annual rate. The level is above the consensus of 700,000 in the Econoday survey of forecasters. The report includes annual revisions. Sales in March are revised substantially lower to 670,000. April sales are up 3.3 percent compared to a year ago.

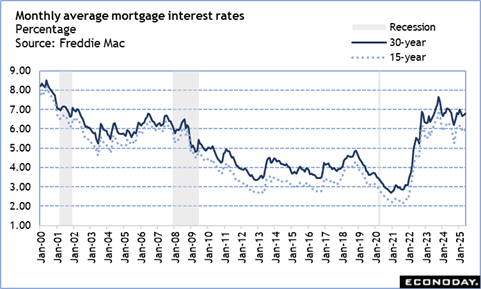

Buyers of new single-family homes likely acted to take advantage of a dip in mortgage rates. Sales in April reflect contracts signed that probably used mortgage rates locked in in March and early April. The Freddie Mac rate for a 30-year fixed rate mortgage rate was at 6.63 percent in the March 6 week but rose incrementally for a few weeks after and then declined to 6.62 percent in the April 10 week. Rates took a jump of 21 basis points to 6.83 in the April 17 week and have remained elevated since then. It remains to be seen if the current higher mortgage rates will choke off new home sales in May at the start of what is usually the busiest home sales period of the year.

Sales are up in three of four regions and show an uneven performance for the new single-family home market in April. The Northeast has declined of 14.8 percent. Sales climb 35.5 percent in the Midwest where homes are typically more affordable. Sales are up 11.7 percent in the South and 3.3 percent in the West.

The supply of new single-family homes on the market is down to 8.1 month’s worth after 9.1 months in March and 7.7 months in April 2024. Homebuilders have been cutting back on new construction. With prices and availability of construction materials uncertain, and labor costly, builders are cautious about starting new projects. New projects are tilting to smaller homes to reach the entry level market. The price of a new single-family home is up 0.9 percent in April to $407,200 from March but down 2.0 percent from $415,300 a year ago.

The dip in mortgage rates in March and into early April encouraged homebuyers to commit to buying before the unit was done. In April, 11 percent of new single-family homes sold are units not yet started and 36 percent are units under construction. Completed single-family homes account for 53 percent of the total.

Sentiment

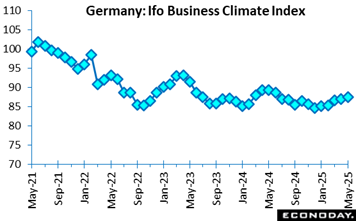

Business sentiment in Germany showed a welcome improvement in May 2025, with the business climate index rising to 87.5, up from 86.9 in April and in line with the consensus forecast. The increase reflects growing optimism about the future, even as firms remain slightly cautious about their current business conditions. The easing of uncertainty suggests that the German economy is beginning to regain momentum after months of subdued performance.

Manufacturing led the sentiment rebound, driven by stabilising orders and more upbeat expectations, especially in the food industry. However, the chemical sector remained under pressure. The services sector also recorded a rise in confidence, with logistics firms bouncing back after earlier disruption from customs-related tensions. Nonetheless, some hesitation remained in assessing present business conditions.

Trade saw a marked lift in optimism across wholesale and retail, with traders reporting improved overall satisfaction. Meanwhile, construction sentiment continued its steady climb, buoyed by a more favourable assessment of current projects and a gradual fading of pessimism about the future.

The latest report points to cautious optimism across Germany’s economic landscape. While current conditions remain uneven, the more positive forward-looking outlook across key sectors signals early signs of recovery and rebuilding business confidence.

Business Surveys

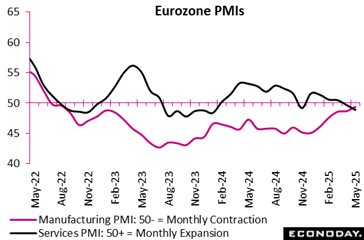

Eurozone business activity faltered in May 2025, marking the first contraction in five months as the composite PMI dropped to 49.5 from 50.4, a six-month low. The services sector led the downturn, where output declined at the fastest pace since January 2023 (48.9 from 50.1), amid sustained weakness in new business and growing uncertainty. Meanwhile, manufacturing showed faint signs of stabilisation, with production rising for a third consecutive month and new orders ending a three-year decline—underscoring a tentative shift toward recovery (49.4 from 49.0).

Despite this, the overall demand environment remains fragile, with new orders across sectors falling for the twelfth month and export demand weakening. Employment plateaued, as job losses in manufacturing offset modest gains in services, particularly in Germany and France, which slipped into contraction territory. Inflationary pressures eased, though unevenly. Manufacturing faced falling input and output prices, while service providers struggled with elevated cost pressures.

Business confidence dipped further, hitting a 19-month low, driven by pessimism in the service sector, where sentiment plunged to levels not seen since 2012 outside the pandemic. In contrast, manufacturers grew more optimistic, buoyed by improving order books and supply conditions, pointing to a potential rebalancing of the recovery narrative.

US Review

Housing Market Looking Shaky

By Theresa Sheehan, Econoday Economist

The data in the May 23 week reveals a housing market that remains interest rate sensitive and nervous about the near future. Consumers are worried about job security and household incomes. In turn, high prices and mortgage rates near the 7-percent mark are exercising a chilling effect on home sales.

The Freddie Mac weekly average rate for a 30-year fixed rate mortgage was as high as 7.04 percent in the January 16 week, then moderated to as low as 6.63 percent in the March 6 week. Rates varied little for the next five weeks, ending at 6.62 percent in the April 10 week. The rate abruptly swung 21 basis points higher to 6.83 percent in the April 17 week, dipped a bit, then started to climb again to 6.86 percent in the May 22 week.

Existing home sales in April – closed in April with contracts signed a month or two earlier – dipped 0.5 percent month-over-month to 4.00 million units at a seasonally adjusted annual rate and were down 2.0 percent from a year ago. Sales of existing single-family homes were down 0.3 percent to 3.63 million units in April from March and were down 1.4 percent from April 2024. The median price of an existing single-family home was up 2.6 percent in April to $418,000 from the prior month and up 1.7 percent from a year ago. In spite of more supply on the market, competition remains fierce for the most sought after units. Buyers have more power to negotiate terms but prices are not falling.

New single-family home sales – for contracts signed but not necessarily closed – increased 10.9 percent to 743,000 in April from 670,000 in March and were up 3.3 percent from a year ago. The size of the month-over-month gain is substantial but probably a one-off as buyers moved to take advantage of lower mortgage rates. The median price of a new single-family home is up 0.9 percent to $407,200 in April from March but down 2.0 percent year-over-year. This is likely due to builders offering smaller units to appeal to first-time buyers.