Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

Germany’s inflation rate in May 2025 shows signs of moderation, with the consumer price index rising by 2.1 percent year-over-year, in line with the consensus, which suggests relative price stability compared to the heightened inflation seen in previous years. On a month-over-month basis, prices increased only 0.1 percent, 0.1 percent below the consensus forecasts. The harmonised index, used for European comparisons, mirrored this trend with a 0.2 per cent monthly increase and the same annual rise of 2.1 percent.

However, the underlying picture reveals more persistent pressures. Core inflation, which excludes volatile food and energy prices, stands at 2.8 percent. This suggests that while headline inflation is cooling, structural price increases remain embedded in the economy, likely driven by services and rent. This mix of low headline and higher core inflation presents a balancing act for policymakers and consumers alike.

GDP

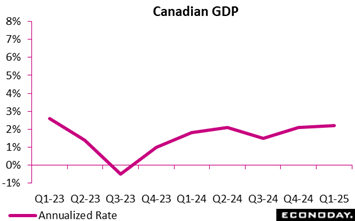

A surge in exports ahead of the imposition of punitive tariffs on Canadian goods by the United States fueled Canada’s first quarter economic activity, but a slowdown in household spending to 0.3 percent (from +1.2 percent in Q4 2024) is in line with the Bank of Canada’s expectation for weaker consumption.

The significant downside risk from tariffs – and the accompanying blow to business and consumer confidence – means the central bank might be forced to take more aggressive actions in the near term to prop up the economy.

GDP increased 0.5 percent in the first quarter of 2025 after also rising by 0.5 percent in Q4 2024 and +0.6 percent in Q3. Economic activity expanded by 2.3 percent compared to the first quarter of 2024.

Total exports rose 1.6 percent in the first quarter of 2025 after increasing 1.7 percent Q4 2024. “In the context of looming tariffs from the United States, exports of passenger vehicles (+16.7 percent) and industrial machinery, equipment and parts (+12 percent) drove the overall increase in exports in the first quarter of 2025,” StatsCan said.

Imports increased 1.1% in Q1, following a 0.6 percent rise in the previous quarter. Higher imports of industrial machinery equipment and parts (+7.4 percent) and passenger vehicles (+8.3 percent) led the overall increase. “The threat of tariffs can be expected to influence trading patterns and incite importers to increase shipments prior to these tariffs being implemented to avoid additional costs,” the report said.

In the United States, the second estimate of first quarter GDP is a negligible upward revision to down 0.2 percent. This is a near match to the consensus of down 0.3 percent in the Econoday survey of forecasters. While growth in personal consumption expenditures is revised lower, government consumption expenditures and gross investment are revised up. Net exports are revised slightly lower and the change in private inventories is revised higher.

The dip in growth in the first quarter 2025 remains a story of a swift and deep widening in the trade deficit that has an outsized effect. However, it is now also a story of moderating consumer spending after households stocked up on goods and locked in prices for services in the fourth quarter 2024 resulting in falling demand in the first quarter.

Personal consumption expenditures rose 1.2 percent in the first quarter. Spending on durables is down 3.8 percent, nondurables spending is up 2.2 percent and services up 1.7 percent. The revision for personal consumption expenditures reflects weaker spending in nondurables and services than first estimated, and even less spending on durables.

Government consumption is revised higher to down 0.7 percent in the first quarter, cutting the advance estimate by nearly half.

Gross investment rise 24.4 percent in the first quarter. The upward revision is in nonresidential investment which is revised to up 10.3 percent, although residential investment reverses from a gain in the advance report to down 0.6 percent in the second estimate.

Net exports are a bit wider in the second estimate for the first quarter at a deficit of $1.268 billion. The change in private inventories is higher in the second estimate at $210.3 billion.

Demand

Germany’s retail sector experienced a mild slowdown in April 2025, with real sales declining by 1.1 percent compared to March. This retreat follows a revised growth of 0.9 percent in March, correcting earlier estimates that had suggested a contraction. Despite April’s dip, year-over-year performance remained positive, with real sales up 2.3 percent compared to April 2024, reflecting underlying resilience in consumer activity.

Sectoral trends reveal a mixed picture. Food retail showed relative stability, dipping just 0.1 percent in real terms from March but rising 2.3 percent over the year, buoyed by strong nominal growth of 4.9 percent, hinting at price pressures. Non-food retail saw a sharper monthly contraction of 1.3 percent in real terms, yet still posted a 2.6 percent year-over-year gain, suggesting consumers remain engaged despite short-term fluctuations. The standout story remains the online and mail order segment, which rose a remarkable 14.1 percent year-over-year in real terms, underlining the persistent digital transformation in shopping habits.

Overall, while April brought a modest pause in momentum, annual growth across all major segments signals cautious consumer confidence and an evolving shift toward digital retail channels.

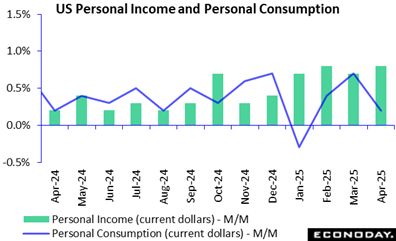

The slowdown in the pace of annual PCE price inflation is encouraging; however, the data does not indicate further progress towards the Federal Reserve’s 2 percent inflation objective. It also fails to capture the delayed impact of the tariffs imposed by the Trump administration in early April. Expect the Federal Reserve to remain on hold as it continues to assess the balance of risks to the economy.

U.S. personal income surged 0.8 percent in April, building on a 0.7 percent increase in March (revised from +0.5 percent) and far above expectations for a 0.3 percent rise in the Econoday survey of forecasters.

Consumer spending, however, as measured by the Personal Consumption Expenditures (PCE) index, slowed down to 0.2 percent last month following a 0.7 percent spike in March as consumers stockpiled ahead of the anticipated imposition of punitive tariffs.

As for the Federal Reserve’s preferred inflation gauge, the PCE price index was up by just 0.1 percent on a monthly basis in April, after no change in March and a 0.4 percent rise in February. Prices for goods saw a 0.1 percent uptick and prices for services increased at the same rate. Food prices fell 0.3 percent and energy prices increased 0.5 percent. Excluding food and energy, the PCE price index was up 0.1 percent, the same rate as in March.

Compared to a year ago, the April PCE price index rose 2.1 percent after a 2.3 percent increase in March. Prices for goods contracted by 0.4 percent and the cost of services jumped 3.3 percent. The core PCE price index is up 2.5 percent from April 2024, compared to March’s 2.7 percent year-over-year increase.

Production

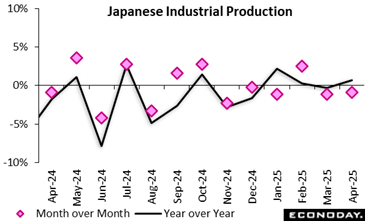

Japan’s industrial production posted its first drop in three months in April, down 0.9% (consensus -1.5%) after a slight 0.2% gain (revised up sharply from -1.1%) in Mach as some effects of the global trade war initiated by President Trump are showing in sluggish export data. The decrease was led by lower output of production machinery (equipment for making flat screen panels, textile and microchips), aircraft parts and metals (bridges, aluminum cans for beverages, etc.)

The Ministry of Economy, Trade and Industry said six out of the 15 industries recorded declines while eight showed gains and one was unchanged. METI’s survey of producers indicated that output would rebound 5.2% in May, led by production machinery, electric/telecom equipment and vehicles. before slipping back 3.4% in June due to expected pullbacks in vehicles and production machinery.

From a year earlier, factory output marked its fourth straight gain, up 0.7%, after rising 1.0% (revised up from -0.3%) in March.

The ministry maintained its assessment, saying industrial output is "taking one step forward and one step back." It said it will keep a close watch on how global economic growth evolves. In its monthly report for May, Japan’s government continued to put on a brave face on the global trade war and politically explosive food price inflation, maintaining its cautiously optimistic domestic economic outlook for the ninth straight month, saying the economy is expected stay on a “modest recovery” track.

US Review

Tariffs Trump Economic Data Again

By Theresa Sheehan, Econoday Economist

The economic data in the May 26 week mostly just confirmed what is already known. The driver for the week was the unknown, specifically another round of whiplash regarding tariff and trade policy. The confusing messaging on tariffs by President Trump extended the unsettled future that has weighed on the economic outlook. It was only briefly alleviated by the ruling from the Court of International Trade that would have nullified many of the tariffs announced by the White House. A subsequent stay from another court plunged the situation back into uncertainty.

The week’s data confirmed that the housing market is facing challenges from elevated mortgage rates and consumer pessimism about the economy and job security. Consumer confidence remains low.

If the Conference Board’s consumer confidence index managed an increase to 98.0 in May from 85.7, consumers remain troubled about both current conditions and the six-month outlook. The University of Michigan’s final consumer sentiment index for May is 52.2, the same as in April. In any case, both indexes are at levels similar to episodes of recession.

The second estimate of first quarter GDP was little revised at down 0.2 percent growth after the down 0.3 percent in the advance estimate. However, the details indicated that consumer spending has lost momentum in the first quarter, falling to up 1.2 percent from 4.0 percent in the fourth quarter. While spending was front-loaded in the fourth quarter, it is not clear if it will rebound in the second quarter.

The FOMC minutes of the May 6-7 meeting offered a picture of conditions three weeks ago but could not incorporate fast-moving developments from recent weeks. The next FOMC meeting on June 17-18 is likely to maintain the wait-and-see approach that has characterized this period of evolving conditions.

Fed Chair Powell was invited to a meeting with President Trump on Thursday. Afterward, the Fed issued a terse statement that nonetheless made the point that an independent central bank will set policy according to the dual mandate given by Congress. The statement said, “Chair Powell did not discuss his expectations for monetary policy, except to stress that the path of policy will depend entirely on incoming economic information and what that means for the outlook. Finally, Chair Powell said that he and his colleagues on the FOMC will set monetary policy, as required by law, to support maximum employment and stable prices and will make those decisions based solely on careful, objective, and non-political analysis.”