Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

As expected, the European Central Bank cut its main policy rates by 25 basis points, indicating that it’s satisfied with the current level of inflation which is around the ECB’s 2.0 percent intermediate term target.

It lowered its forecasts for inflation forecasts by 0.3 percentage points for this year and next to 2.0 and 1.6 percent, respectively. With current heightened uncertainty, the ECB will continue to be data-dependent in its assessments and review its policy stance on a meeting-by-meeting basis.

The ECB touched on current trade tensions, saying that should they continue in the coming months growth and inflation would be below baseline expectations. Given the current posture of the US administration, it’s unlikely those will abate in the near term. Germany’s new Chancellor Friedrich Merz is headed to the US for talks with Donald Trump which may give some insight into how tariff policy might proceed.

Should there be a "benign" resolution, the ECB stated expects growth and inflation will be higher than the baseline.

ECB President Christine Lagarde told reporters after the announcement that the rate decision was nearly unanimous with only one dissenting vote.

Inflation

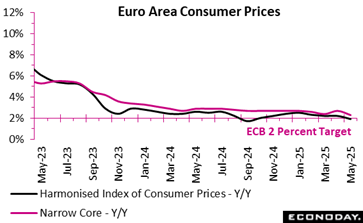

Euro area inflation eased to 1.9 percent in May 2025, falling below the European Central Bank’s 2 percent target for the first time in several months. This deceleration from April’s 2.2 percent suggests growing price stability across key sectors. However, the underlying story reveals nuanced dynamics. While food, alcohol, and tobacco inflation increased slightly to 3.3 percent, likely reflecting ongoing supply-side pressures, the more significant decline was in services inflation, which fell sharply to 3.2 percent from 4.0 percent in April.

Non-energy industrial goods inflation remained subdued at 0.6 percent, pointing to stable manufacturing input costs, while energy prices continued their deflationary trend at minus 3.6 percent, unchanged from April. Persistently negative energy inflation is a crucial drag on overall inflation, offering consumers some relief but also reflecting ongoing volatility in global energy markets.

Among the biggest economies in the area, annual inflation fell in Germany (2.1 percent after 2.2 percent), Spain (1.9 percent after 2.2 percent), Italy (1.9 percent after 2.0 percent) and France (0.6 percent after 0.9 percent).

The latest inflation updates suggest a more balanced price environment in the euro area. If this trend persists, it could strengthen the case for a shift in monetary policy stance, especially as the ECB weighs rate adjustments in the context of moderating inflationary pressure.

Employment

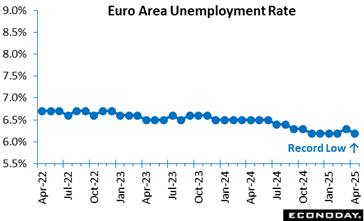

Unemployment in the euro area continued its downward trend in April 2025, with the overall rate falling to 6.2 percent, the lowest over a year. Eurostat’s data reveals a reduction of 207,000 unemployed individuals since March and 343,000 compared to April 2024, suggesting a steadily improving labour market. This progress reflects gradual economic resilience, possibly supported by stabilising inflation and sectoral recovery.

Youth unemployment, often a structural concern, also showed encouraging signs. The rate dropped to 14.4 percent, down from 14.8 percent in March, with 74,000 fewer young people unemployed. Although still high, this marginal improvement hints at a modest recovery in youth labour absorption, possibly linked to seasonal hiring and emerging digital sector opportunities.

Gender-based unemployment gaps also narrowed slightly. Women’s unemployment declined to 6.5 percent, and men’s to 6.0 percent, signalling a more balanced labour recovery. However, the gender gap persists, implying continued barriers to equal labour force participation.

Among the biggest economies in the area, the national unemployment rate did not change between March and April in Spain (10.9 percent after 10.9 percent) and Germany (3.6 percent after 3.6 percent). However, it fell in Italy (5.9 percent after 6.1 percent) and France (7.1 percent after 7.4 percent).

The euro area’s labour market appears firmer, with gains across age and gender groups. These improvements could bolster consumer confidence and strengthen the region’s post-inflation recovery momentum if sustained.

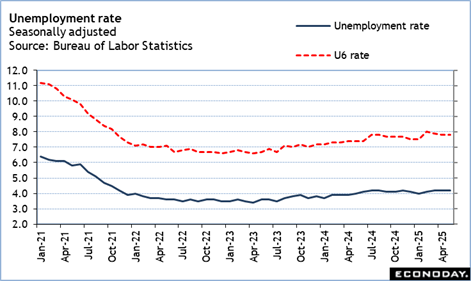

The FOMC will find signs of further cooling in the labor market in the May employment report. The unemployment rate remains steady at a level historically consistent with a healthy labor market able to absorb new entrants and those separated from their jobs. However, the general downward direction of new hiring suggests that businesses are only hiring where necessary and with a wary outlook for economic conditions. The FOMC may deem the labor market remains solid but with a gloomier forecast for the future.

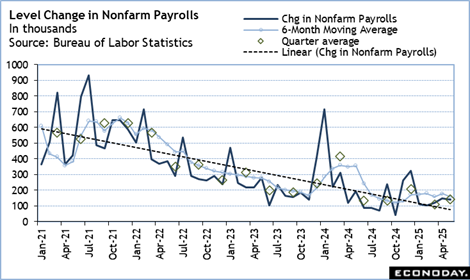

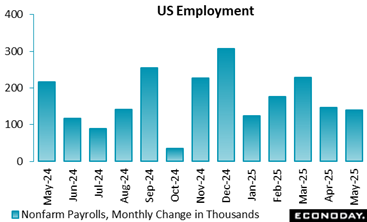

Nonfarm payrolls are up 139,000 in May, a bit above the consensus of up 129,000 in the Econoday survey of forecasters. However, there is a net downward revision to the prior two months of 95,000. The first two months of the second quarter 2025 shows a monthly average increase in payrolls of 143,000, while payroll growth in the first quarter is less than previously thought with a monthly average of up 111,000. Both are below the monthly average of up 209,000 in the fourth quarter 2024. Hiring is ongoing in the present economy, but the underlying trend is slower. Hiring is more diffuse and subject to uneven demand in the major sectors.

Hiring among goods-producers is down 5,000 in May. Construction has been a strong performer since the pandemic sparked a hot housing market but appears to be losing momentum with an increase of 4,000 in May. Manufacturing payrolls are down 8,000 in May and mining and logging are down 1,000. Payrolls at private service-providers are up 145,000 in May. Over half of that is accounted for with an increase of 78,300 in health care and social assistance. One-third of the sectoral increase is from 48,000 new hires in leisure and hospitality at the start of the summer vacation season. Government hiring is down 1,000 in May with federal jobs down 22,000, state government jobs flat, and local government up 21,000.

Average hourly earnings are up 0.4 percent in May from April and up 3.9 percent compared to a year ago. The annual increase has been steady for the last five months, suggesting a plateau in wage gains. The average workweek is unchanged at 34.3 in May from April.

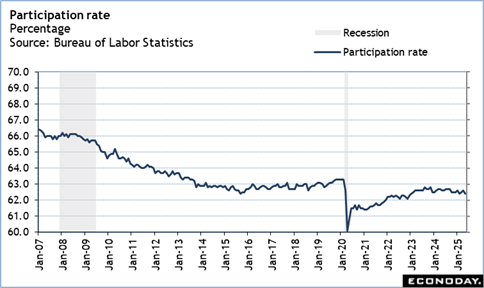

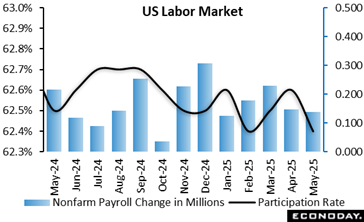

The unemployment rate is 4.2 percent in May, the same as in the prior two months. The U-6 rate – the broadest measure of unemployment – is unchanged at 7.8 percent in May from April. The participation rate is down two-tenths to 62.4 percent in May, erasing the rise in the prior two months. The civilian labor force shrinks 625,000 to 179.510 million in May with the number of people employed down 696,000 to 163.273 million and the number of unemployed up 71,000 to 7.237 million.

Although the pool of workers is smaller, so are the number of jobs open. A less competitive job market means less churn. The number of people leaving one job for another is down for a second month in a row and falls 151,000 to 704,000 in May. May is typically a month in which college graduates enter the workforce. New entrants are 24,000 higher in May to 725,000.

Demand

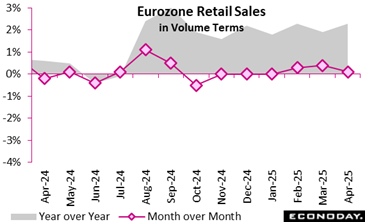

On a monthly basis, Eurozone retail trade volume went up slightly by 0.1 percent, following a modest revised gain of 0.4 percent in March, indicating a slower pace in consumer momentum. Sector-wise, food, drinks, and tobacco sales went up by 0.5 percent, while non-food products also went up by 0.3 percent. Automotive fuel sales offered a modest lift, rising by 1.3 percent, possibly driven by increased mobility or seasonal factors.

On an annual basis, the picture was even more encouraging. Retail trade rose by 2.3 percent compared to April 2025, buoyed by a 2.3 percent rise in non-food product sales and a 2.2 percent increase in food and drink purchases. Automotive fuel sales also rose by 2.9 percent, suggesting overall consumer demand remains robust.

The revised March data showed a better performance with the broader trend hinting at improved consumer confidence. April’s modest monthly increase may be an effect of the ongoing economic uncertainty, however the annual growth points to underlying resilience in euro area consumption.

Business Surveys

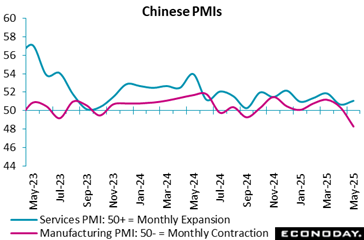

The S&P Global China manufacturing PMI showed a sharp deterioration in conditions in the sector in May, with the headline index falling to 48.3 from 50.4 in April. This is the first time this survey has shown contraction in the sector since September 2024 and the index is now at its lowest level since September 2022. Official PMI survey published on the weekend also showed contraction in the sector in May.

Respondents to the S&P PMI survey reported output, new orders, and new export orders all fell in May and all fell at the sharpest pace in well over a year. Respondents cited the impact of the increase in global trade tensions as a significant factor weighing on external demand. Payrolls were also reported to have been cut in May but the survey’s measure of business confidence shows that respondents expect output to rise from current levels over the next twelve months. The survey also shows input costs fell for the third month in a row and at a sharper pace and that firms cut selling prices for the sixth consecutive month.

The S&P Global PMI composite index for China fell to 49.6 in May from 51.1 in April, indicating contraction in the aggregate Chinese economy for the first time since December 2022. The business activity index for China’s services sector, also published today, rose to 51.1 from 50.7 in April, but the headline index for the manufacturing PMI survey, published earlier in the week, showed renewed contraction in the sector. Official PMI survey data also showed weak conditions in both the manufacturing and the non-manufacturing sector in May.

Respondents to the service sector survey reported improved growth in output and new orders in May, though new export orders were reported to have fallen for the first time this year. The survey showed a small increase in payrolls after two consecutive reductions and its measure of confidence also rebounded from a sharp drop in April, perhaps indicating optimism that global trade tensions will ease. Respondents also reported a stronger increase in input costs but a fourth consecutive reduction in selling prices.

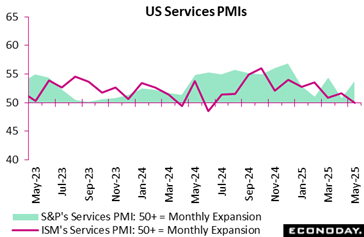

U.S. services sector activity contracted in May, a reflection of the heightened uncertainty following the Trump administration’s escalation of the trade war in April.

The ISM Services PMI fell to 49.9 in May, compared to the 51.6 recorded in April, and lower than the 52.0 expected in the Econoday survey of forecasters.

“Respondents continued to report difficulty in forecasting and planning due to longer-term tariff uncertainty and frequently cited efforts to delay or minimize ordering until impacts become clearer,” the report said.

The New Orders Index contracted for the first time in nearly a year, while higher tariffs drove prices paid by services sector companies to their highest level since November 2022.

Employment expanded after two months in contraction territory, recording the second straight month-over-month gain.

The S&P Global US Composite Purchasing Managers’ Index came in at 53.0 in May, up from 50.6 in April – signaling an uptick in services sector activity while manufacturing output dipped – and above the 52.1 consensus in the Econoday survey of forecasters.

Confidence in the outlook was the highest since January, while tariffs fueled “noticeable accelerations” in both input price and output charge inflation.

The US Services PMI Business Activity Index recorded 53.7 in May, speeding up from 50.8 in April, and beating expectations of 52.3 in the Econoday survey of forecasters.

“There were reports from survey panelists of a more stable business environment compared to April, which helped to drive a rise in client spending,” the report said. “This was however broadly limited to domestic-based customers as foreign sales declined overall for a second successive month.”

“Rising backlogs in part reflected delays in the delivery of ordered equipment due to tariffs, which also drove up cost inflation to its highest in nearly two years,” the report added. “Increased costs were passed on to clients via the steepest increase in output charges since August 2022.”

On the jobs front, the report said a more positive sentiment, plus a rise in current workloads, helped to support increased employment during May – the third in as many months – although it was a modest rise given the non-replacement of job-leavers.

“Moreover, the rise in staffing levels was insufficient to prevent the steepest increase in work outstanding since last November,” the report said.

“Overall, sentiment was at its highest for four months (though remained well below the survey average). Panelists are also planning to raise their marketing and expand their business facilities over the coming year,” the report added.

US Review

Employment Situation: Not So Good

By Theresa Sheehan, Econoday Economist

Despite an unemployment rate that is stable at 4.2 percent in May, there are signs of further weakening in the US job market. The May increase of 139,000 in nonfarm payrolls is substantially lessened by the net downward revision of 95,000 to the prior two months. The economy continues to add jobs at pace that is consistent with an ability to absorb new entrants and find jobs for those who are separated from their previous employment. However, the bulk of the new jobs are in two service sector categories – health care and social assistance, and leisure and hospitality. Outside of those two, job gains are anemic where these are happening.

If unemployment is not rising, it is because the labor force is falling. The size of the labor force is down 625,000 to 170.510 million in May with the number of employment down 696,000 to 163.273 million and the number of unemployed up 71,000 to 7.237 million. The labor force participation rate is down two-tenths to 62.4 percent in May, retracing the improvement from the prior two months. The labor force participation never fully recovered from the effects of the pandemic. Now another wave of exits from the labor force is developing. Some will be from voluntary retirements related to government and private sector retrenchments. Some will be from a net loss in immigration.

It is also worth noting that the Fed’s Beige Book released on June 4 painted a picture of an economy heading into a recession. It is not yet clear whether the economic shock of the arrival of the Trump administration and the imposition of its agenda will end up having a short-term effect similar to a natural disaster or if growth will be affected in the near term.