Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

China’s headline producer price index fell 3.3 percent on the year in May, weakening further from the 2.7 percent decline recorded in April. Headline PPI inflation has been in negative territory since late 2022 and this is the biggest year-over-year decline since July 2023. The index fell 0.4 percent on the month, as it did previously. Consumer price data also published today showed headline inflation remained in negative territory in May.

The data showed a bigger fall than the consensus forecast for a year-over-year decline of 3.0 percent.

The cooler-than-expected US inflation data reflects momentary calm before price increases due to tariffs from mid-2025 onwards. The Federal Reserve will be encouraged by this data, but it is unlikely to shift the central bank out of its wait-and-see mode until it has greater certainty that the tariffs will not have a broad and sustained inflationary impact.

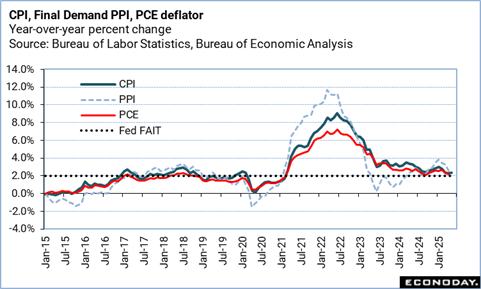

US Consumer Price Index in May slowed to +0.1 percent, following a 0.2 percent rise in April, and a 0.1 percent decline in March. This compares to expectations for a 0.2 percent rise in the Econoday survey of forecasters. The slowdown in the pace of consumer price continues after a steep rise in the CPI between November 2024 and January 2025.

Over the last 12 months, consumer prices are up 2.4 percent, compared to a 2.3 percent year-over-year rise in April. Expectations in the Econoday survey were for a 2.5 percent increase.

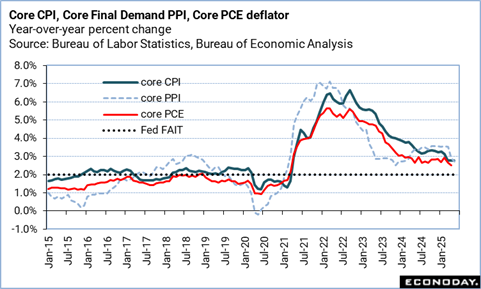

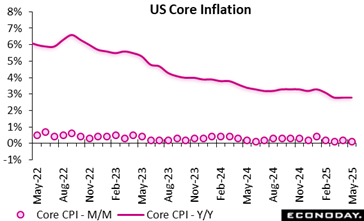

Core CPI, excluding food and energy prices, are up by 0.1 percent, after rising by 0.2 percent in April, and +0.1 percent in March. Consumer prices less food and energy rose 2.8 percent from May 2024, matching the rate of increase on an annual basis in April, and just under the 2.9 percent consensus in the Econoday survey.

After rising by 0.3 percent in April, shelter costs rose by the same rate again in May (and are up 3.9 percent year-over-year). Food prices rebounded by 0.3 percent, erasing a 0.1 percent dip in April, as grocery prices rose 0.3 percent last month, and restaurant prices also rose by 0.3 percent.

Energy costs fell 1 percent over the month, dragged down by a 2.6 percent drop in gasoline prices.

Energy prices are down 3.5 percent year-over-year, following a 3.7 percent slide for the 12 months ending April. Food prices increased 2.9 percent compared to May 2024, following a 2.8 percent rise in April.

Employment

Despite a rise in the UK employment rate (75.1 percent) and an increase in total workforce jobs to 37.1 million, the number of payroll employees declined consistently, from a modest 55,000 drop in April to a sharper 109,000 monthly fall in the early May estimate. Over the year, the number shrank by 274,000, reflecting cooling demand in the job market. Meanwhile, unemployment rose to 4.6 percent, and economic inactivity increased to 21.3 percent, suggesting some return to the labour force but not enough to offset job losses.

Vacancies also fell for the 35th consecutive quarter, pointing to firms’ hesitancy to hire or replace staff. Yet wage growth remained robust. Annual regular earnings rose by 5.3 percent, with real-term growth at 1.4 percent (CPIH-adjusted) and 2.1 percent (CPI-adjusted). Also, the claimant counts for May 2025 increased on the month and the year, to 1.735 million.

The public sector saw slightly stronger pay growth than the private sector. While earnings are improving and job numbers are expanding overall, persistent declines in payroll and vacancies signal a labour market under pressure.

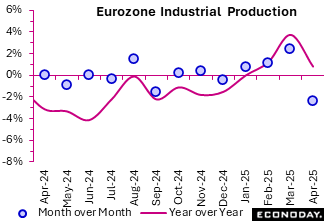

Production

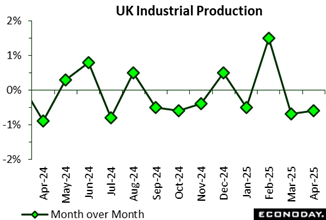

The UK’s production sector stumbled in April 2025, with monthly output down by 0.6 percent, marking a second consecutive decline after March’s 0.7 percent drop. This reversal was largely driven by a sharp 0.9 percent fall in manufacturing and a significant 4.3 percent drop in electricity and gas output, reflecting possible seasonal or supply-related disruptions. Notably, the transport equipment subsector, a key driver in March, plummeted by 5.2 percent, undoing its previous month’s gains and signalling volatility in industrial demand.

Over the year, industrial production fell by 0.3 percent, while manufacturing output rose by 0.4 percent. Over the three months to April 2025, production output grew by 1.1 percent, sustained primarily by manufacturing’s 1.2 percent increase. This expansion in manufacturing output was bolstered by gains in 11 of 13 manufacturing subsectors, with notable strength in textiles, machinery, and transport equipment. Positive contributions also came from water supply (up 3.7 percent) and electricity and gas (up 1.0 percent), partially cushioning the sector from the drag caused by mining and quarrying (down 1.3 percent).

Indeed, April’s figures reveal short-term turbulence, particularly in energy and transport manufacturing, while the underlying trend over the quarter reflects cautious optimism, driven by diversified gains across multiple industrial subsectors.

Industrial production declined by 2.4 percent in April compared to March 2025. All major product categories saw monthly declines, with non-durable consumer goods falling the most at minus 3.0 percent, hinting at cooling consumer demand. Intermediate goods, capital goods, and energy also recorded contractions, signalling widespread output weakness across supply chains and manufacturing.

Despite the monthly downturn, year-over-year figures offered modest reassurance. Euro area industrial production was 0.8 percent higher than in April 2024, underpinned by a strong 6.1 percent surge in non-durable consumer goods, likely reflecting resilient consumer spending on essentials. However, persistent annual declines in intermediate goods (minus 1.0 percent), capital goods (minus 0.6 percent), and energy (minus 0.1 percent) suggest subdued investment activity and ongoing challenges in energy-intensive industries.

Regionally, industrial production fell in Germany (minus 2.4 percent after minus 0.1 percent) and France (minus 2.1 percent after 0.1 percent), while it rose in Spain (0.5 percent after 1.2 percent) and Italy (0.3 percent after minus 1.8 percent) on an annual basis.

The latest updates suggest that policymakers and investors may need to monitor closely for signs of sustained slowdown, especially as consumer momentum alone may not be enough to stabilise industrial output in the longer term.

US Review

CPI Was Good but Not Good Enough

By Theresa Sheehan, Econoday Economist

Although the PCE deflator is the Fed’s preferred measure of inflation, the May CPI report is what the FOMC will have in hand when it meets on June 17-18. In assessing the risks to the price stability side of the dual mandate, the May numbers point to what Chair Jerome Powell has termed as “sideways” move for progress in disinflation.

The month-over-month increase in the all-items and core CPI was a quite mild 0.1 percent. However, it is the year-over-year increase that will be on the mind of Fed policymakers. The all-items CPI has stalled in the past three months at up 2.4 percent in May, up 2.3 percent in April, and up 2.4 percent in March. The CPI excluding food and energy is up 2.8 percent in May, April, and March. It is this measure of inflation that looks past the two most volatile components of the CPI and which the FOMC will use to evaluate current inflation. It is also this sort of reading that has led the FOMC to call inflation “somewhat elevated” in its meeting statements.

The CPI will not counsel the FOMC to reduce the fed funds target rate range from the present 4.25-4.50 percent.

On the maximum employment side of the dual mandate, the data for initial jobless claims in the June 7 week hints that layoff activity is rising, albeit slowly and not yet to alarming levels. Initial jobless claims remained at 248,000 in the June 7 week after a minor downward revision to 248,000 in the prior week (previously 249,000). This is the highest since 250,000 in the week of October 5, 2024. The four-week moving average rose 5,000 to 240,250 in the June 7 week, the highest since 245,000 in the August 26, 2023 week. This strongly suggests that the week-to-week variations that have kept the level from rising steadily are ending and that risks to the labor market have increased.