Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

All of the key decisions and assessments by the Bank of Japan board were widely expected:

–The BOJ nine-member board voted unanimously to maintain the target for the overnight interest rate at 0.5% for the third straight meeting after hiking it by 25 basis points (0.25 percentage point) in January amid uncertainty over the trade war and heightened geopolitical risk.

–The bank didn’t say it will continue raising rates if growth and inflation evolve in line with its medium-term outlook but it is still in the process of normalizing its monetary policy stance from years of keeping short-term rates near zero percent. It repeated its latest outlook that underlying CPI inflation (still around 1.5%) is likely to settle around the bank’s 2% target in the second half of the projection period (fiscal 2025 through fiscal 2027).

–The board decided in an 8 to 1 vote to moderate the JGB purchase reduction pace to by about ¥200 billion a quarter in fiscal 2026 starting in April from by about ¥400 billion now, which will reduce the pace of its JGB buying to around ¥2.1 trillion in January-March 2027 from about ¥4.1 trillion in January-March 2027.

–Board member Naoki Tamura, a former SMBC banking group executive, called for the same tapering pace of ¥400 billion every quarter into the next fiscal year, arguing that the bank should let markets forces set long-term rates.

–The decision is aimed at striking a fine balance between the need to shrink its balance sheet and the need to prevent the lower debt holdings by the central bank from jacking up long-term market interest rates.

–The board maintained the slowing pace of Japanese government bond purchases by about ¥400 billion a quarter for the current fiscal year ending in March 2026 in line with its July 2024 decision to taper JGB buying to around ¥3 trillion in the January-March quarter of 2026 from about ¥6 trillion then (to ¥2.9 trillion from ¥5.7 trillion, to be more precise).

–The BOJ repeated its mantra: Long-term interest rates should be formed in financial markets in principle; it is “appropriate” to trim its JGB purchases ‘in a predictable manner while allowing enough flexibility to support stability in the JGB markets.”

The FOMC maintains the fed funds target rate range at 4.25 to 4.50 percent as expected after the June 17-18 meeting. The post-meeting statement was largely the same as the prior one. The current statement noted that the unemployment rate “remains low” and inflation is still “somewhat elevated”. The main difference in the two statements is that the language regarding the risks to the economy have been downgraded, although not gone.

The latest statement said, “Uncertainty about the economic outlook has diminished but remains elevated” compared to risks being on the rise prior to the last meeting in May. The statement said, “The Committee is attentive to the risks to both sides of its dual mandate,” excising the language about higher risks to unemployment and inflation.

The quarterly update to the summary of economic projections (SEP) that accompanies the statement forecasts slower growth and slightly higher unemployment than in the prior report. Forecasts for the PCE deflator point to noticeably higher inflation in the near term and carrying into 2026. However, the projected appropriate policy path is unrevised for 2025, suggesting two rate cuts of 25 basis points each by the end of this year with a midpoint of 3.9 percent. The path for 2026 and 2027 was for only modest reductions in the fed funds rate. The midpoint for 2026 is revised up to 3.6 percent (previously 3.4 percent) and for 2027 at 3.4 percent (previously 3.1 percent).

This reflects a downward revision for 2025 GDP growth to 1.4 percent (previously 1.7 percent) and for 2026 GDP at 1.6 percent (previously 1.8 percent), while 2027 is unrevised at growth of 1.8 percent. These are mostly below the longer run forecast of up 1.8 percent.

The unemployment rate for 2025 is forecast at 4.5 percent (previously 4.4 percent), 2026 at 4.5 percent (previously 4.3 percent), and 2027 at 4.4 percent (previously 4.3 percent). These are above the longer run forecast of 4.2 percent.

Inflation is expected to decline more slowly in 2025 and into 2026 and 2027. The PCE deflator rise is revised up to 3.0 percent (previously 2.7 percent), 2026 is now up 2.4 percent (previously up 2.2 percent), and 2027 at up 2.1 percent (previously). The core PCE deflator increase is now up 3.1 percent (previously 2.8 percent) for 2025, 2.4 percent (previously 2.2 percent) for 2026, and 2.1 percent (previously 2.0 percent) for 2027. The longer-run expectation for the PCE deflator and core PCE deflator remains at 2.0 percent.

The Swiss National Bank lowered its policy rate by 25 basis points to zero, as anticipated by economists. A minority expected a larger cut which would have kicked off another era of negative rates, a regime the SNB exited in September 2022 after seven years.

In its assessment following the decision, the SNB specifically mentioned trade, noting increased trade tensions are dampening the global economic outlook. It was also concerned additional barriers could be implemented, accelerating the global economic slowdown. The Swiss economic outlook is presently uncertain, with the main risks coming from abroad.

Earlier today, Switzerland reported that its trade surplus nearly halved in May to 3.381 billion Swiss francs from 6.325 billion the previous month, with exports to the US dropping by over 40 percent for two consecutive months. The strong Swiss franc can also have a dampening effect on exports, and the SNB repeated its willingness to be active in foreign exchange markets if necessary.

The central bank sees no inflation threats in the near term. It lowered its 2025 inflation forecast to 0.2 percent from 0.4 percent and that for 2026 from 0.8 percent

to 0.5 percent from its March forecast. Those results were based on the assumption the policy rate remains at zero for the forecast horizon, and that without today’s rate cut, the forecast would have been lower.

While it expects moderating inflation in Switzerland and Europe, it sees prices rising in the US. Left unsaid was that tariffs act as an inflationary trigger on the country imposing them.

With no threat of inflation and a slowing global economy, the stage is set for the SNB to again enter a negative era of interest rates. This is likely to become reality when the policy makers meet again in September.

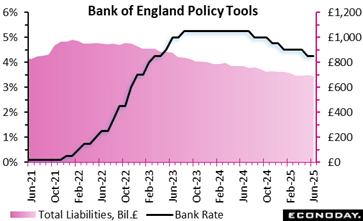

The Bank of England’s June 2025 Monetary Policy Summary signals cautious optimism as inflationary pressures ease. The Monetary Policy Committee (MPC) voted 6 (unchanged) – 3 (rate cut) to keep the Bank Rate at 4.25 percent, reflecting a delicate balance between supporting disinflation and guarding against premature loosening. Although three members favoured a cut, the majority opted to maintain restraint amid lingering global risks and geopolitical tensions, particularly rising energy prices due to Middle East conflict.

The UK economy shows signs of fragility. GDP growth remains weak, the labour market is softening, and pay growth is slowing, suggesting a growing slack in the economy. Yet, inflation rose to 3.4 percent in May, driven by regulated and energy prices, although this was in line with expectations. The MPC expects inflation to stabilise at current levels before easing towards the 2 percent target in 2026.

Indeed, the outcome of the monetary policy meeting is one of cautious patience. Monetary policy will remain restrictive, with the MPC signalling flexibility depending on evolving data. Their approach remains pragmatic, responsive to shifting global dynamics and domestic slack, ensuring inflation expectations stay anchored without choking off economic recovery.

Inflation

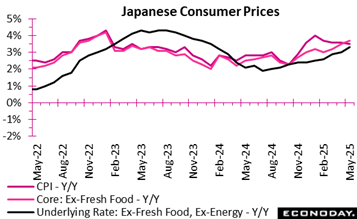

Key points: Consumer inflation in Japan accelerated further in two of the three key readings in May, as largely expected, in the aftermath of rice supply shortages (regular rice prices double the year-earlier levels), partly offset by easing gasoline and utility costs as well as the year-long price-cutting effect of free high school education that began at a national level on April 1

–Core CPI (excluding fresh food) +3.7% y/y, the highest since +4.2% in January 2023 vs. +3.5% in April

–Total CPI +3.5% y/y vs. +3.6% in the previous two months, +4.0% in January; fresh food prices dipped (-0.1%) y/y after the recent spike caused by poor harvest, high import costs.

–Core-core CPI (ex-fresh food, energy) +3.3% y/y vs. +3.0%, the highest since +3.5% in January 2024

Takeaway: The current high inflation rate, neck and neck with Britain on top of the G7 list, is not backed by domestic demand (wage-heavy services price hikes lag behind goods price gains) but largely pushed up by higher import costs. This means that inflation in Japan is not accompanied by sustained and substantial wage growth and that underlying inflation, estimated by the Bank of Japan to be around 1.5%, just below the bank’s 2% price stability target. The bank is in the process of normalizing its policy stance after a decade-long large-scale easing period through 2022 and is set to continue gradually raising the overnight interest rate from the current level of 0.5%. Officials argue that real borrowing costs remain "significantly negative" because the BOJ has been cautious about raising rates even when inflation expectations are rising moderately.

The inflation picture in the UK for May 2025 signals cautious progress. Headline CPI eased slightly to 3.4 percent (from 3.5 percent in April), reflecting modest disinflationary pressure. Monthly CPI rose by just 0.2 percent, slower than the 0.3 percent pace a year earlier and the consensus forecast. Transport costs drove the most significant downward pull on the inflation rate, while rising food prices and household goods softened this effect. Core CPI, which excludes volatile items, also slowed to 3.5 percent from 3.8 percent, indicating easing underlying inflation. However, goods inflation increased to 2.0 percent, suggesting persistent supply-side pressures.

The broader CPIH, which includes housing costs, also dipped to 4.0 percent (from 4.1 percent), with monthly growth halving year-over-year (0.2 percent vs. 0.4 percent). Core CPIH decelerated to 4.2 percent, down from 4.5 percent, though services inflation remains relatively elevated at 5.3 percent. Notably, a previous overstatement caused by a vehicle excise duty error in April has been corrected in the May data.

The data reflects a slow but steady easing in inflationary pressure, with services still sticky. The Bank of England may view this as incremental progress but will likely remain cautious about cutting rates too soon given persistent core and housing-related inflation.

Demand

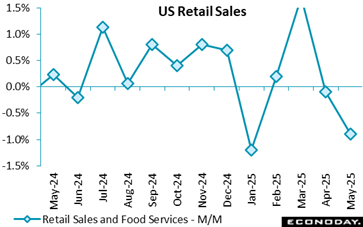

Evidence of the trade war’s impact in May’s US retail sales data, with consumer spending continuing to tail off following the March’s surge to get ahead of the punitive tariffs imposed in April.

The underlying data, however, shows enough resilience for Federal Reserve officials to not be overly concerned when they meet this week for the June gathering of the Federal Open Market Committee.

U.S. May retail sales declined by 0.9 percent, slowing down further from the revised 0.1 percent monthly drop reported for April (previously +0.1 percent), and greater than the -0.6 percent consensus in the Econoday survey of forecasters.

Core retail sales, removing autos and gasoline sales, dipped 0.1 percent last month following a revised flat reading in April (previously reported as +0.1 percent). Core retail sales are up 4.6 percent on an annual basis in May compared to a 5.3 percent y/y jump in April.

Auto sales fell 3.5 percent (still +2.5 percent vs. last year), as activity continues to fall off following the spike in March.

The post-Winter/Spring spending binge is also winding down, with building materials, garden equipment and suppliers’ sales down 2.7 percent in May, while restaurants and bars’ sales fell 0.9 percent (but +5.3 percent from May 2024).

There was a 0.9 percent uptick in online sales, and they are 5.3 percent higher than a year ago.

Compared to a year ago, May retail sales are up 3.3 percent, compared to April’s 5 percent jump.

Excluding gasoline, retail sales decreased 0.8 percent, falling after April’s flat reading, and jumped 4.1 percent from May 2024 vs. +6 percent on an annual basis in April.

Stripping out purchases of motor vehicles and parts, sales fell 0.3 percent compared to no change (previously +0.1 percent) in April. On an annual basis, retail sales ex-autos are up by 3.5 percent, a slowdown from April’s 4.1 percent pace.

US Review

Tariff Uncertainty Keeps Fed on Hold

By Theresa Sheehan, Econoday Economist

Fed Chair Jerome Powell answered questions at Wednesday’s press briefing about why the FOMC is not lowering the fed funds target rate range from the current 4.25 to 4.50 percent that has been in place since the December 2024 meeting. Economic growth is moderating, labor markets are a tad weaker, and inflation is near the 2 percent objective – although somewhat closer or further away depending on which measure is preferred.

The crux seems to be anticipation of and uncertainty around the impact of higher tariffs. The size and timing of tariffs and which countries will bear the brunt of higher import taxes is unsettled as yet. Powell pointed out that whatever the final form of tariffs, these will have to be paid by someone along the supply chain. In question is whether that will be manufacturers, shippers, wholesalers, or the consumer, or some combination of these.

The current fed funds rate remains some distance from 3.0 percent in the FOMC longer-run forecast and isn’t expected to be significantly lower in the remainder of 2025 and through 2027. The FOMC forecast implies about two rate cuts of 25 basis points before the end of this year. But that remains dependent on the economic data and how the tension in the dual mandate plays out between maximum employment and price stability.

The FOMC also cannot do much to anticipate the impact of geopolitical events which are a big wild card. The escalating conflict in the Middle East could have implications beyond disruption of oil supplies and spillover effects into global economies.

In the meantime, the FOMC will be carefully parsing the available economic data and watching financial markets for instability.