Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

Canada’s Consumer Price Index was up 0.6 percent in May from April, coming in at the high end of expectations in an Econoday survey of forecasters that had centered on a 0.5 percent increase. The 12-month inflation rate remained stable at 1.7 percent, as expected.

Excluding energy, year-over-year inflation slowed to 2.7 percent from 2.9 percent, with energy prices dropping 11.0 percent from a year earlier despite a 0.9 percent monthly gain.

Excluding food and energy, core inflation was up 0.6 percent on the month and 2.6 percent year-over-year, above the 2 percent Bank of Canada’s target. Food prices were up 0.5 percent on the month and 3.4 percent year-over-year.

Two of the Bank of Canada’s own measures of core inflation showed some easing pressure as they came down to 3.0 percent from 3.1 percent, although this is still the top end of the central bank’s 1-to-3 percent operating range. The average remained steady at 2.9 percent.

Core inflation, while stable, still remains quite a bit higher than the central bank’s target for comfort and likely in the “firmness” zone.

Goods prices were up 0.5 percent on the month while edging down 0.1 percent on the year. Services rose 0.7 percent and 3.2 percent, respectively.

In its minutes of the June 4 meeting, the Bank of Canada pointed out the “considerable” amount of time spent on discussing inflation in light of opposing pressures from weaker demand and higher tariff-related costs. Governing Council members assessed that the direct impact from retaliatory tariffs on goods prices “was not yet evident”. But Governor Tiff Macklem said in a June 18 speech that overall “we may be seeing some indirect effects related to trade disruption”. On the downside, the elimination of the consumer carbon tax will also continue to have a downward effect on year-over-year comparisons for months to come.

In May, the eight main categories saw higher monthly prices, except shelter, which was flat, for a 12-month increase of 3.0 percent. Given the concern of some of the central bank members over the breath of CPI categories with price increases above 3.0 percent, the slowdown in shelter from 3.4 percent the previous month will come as a relief. The weight of shelter in the basket inched up to 29.41 percent from 29.15 percent in the 2023 basket. Still, mortgage interest cost and rent remained the top two contributors to the 12-month CPI increase. That being said, both saw a slowdown in May, to 4.5 percent from 5.2 percent for rents and to 6.2 percent from 6.8 percent for mortgage interest cost, which decelerated for the 21st consecutive month. Gasoline prices, down 15.5 percent, were the main downward contributor to the 12-month CPI, followed by air transportation.

On a 12-month basis, transportation was the only one of the eight main categories to record lower prices, with a 1.3 percent decline. The highest increase was food (3.4 percent).

On a monthly basis, traveller accommodation was main upward contributor (21.6 percent), followed by telephone services and gasoline prices, which increased 1.9 percent, driving up transportation.

The seasonally adjusted CPI rebounded 0.2 percent on the month after declining 0.2 percent in April. The core index, however, rose at a steady pace of 0.3 percent.

Overall, the report provided some relief, with core prices stabilizating, but likely not enough reassurance to move ahead with a 25-basis point rate cut that had been discussed at the June 4 BoC meeting. The latter will also depend on the extent to which activity weakens in the second quarter.

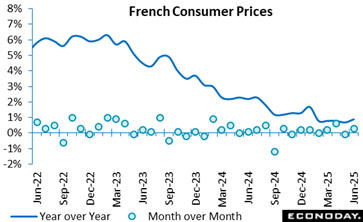

After declining in May by 0.1, French consumer prices are seen rising 0.3 percent in June, driven higher by increased prices for services and higher petroleum product prices, likely from the events in the middle east.

Year-on-year, prices are predicted to rise 0.9 percent from June of last year, compared with a 0.7 percent gain in May, according to preliminary estimates. Services were the main driver, rising 2.4 percent in June from a year ago after a 2.1 percent annual gain in May. A 6.9 percent drop in energy prices helped mitigate the overall increase. Food prices gained 1.4 percent in June from a year ago, up from 1.3 percent in May.

The harmonized CPI used to compare inflation among EU countries rose 0.8 percent in June from a year ago, accelerating from 0.6 percent in May. On a monthly basis, inflation is seen up 0.4 percent in June after falling 0.2 percent in May.

Energy prices have been keeping overall prices gains in check, but with volatility in the middle east, that could change rapidly.

More details will be available with the release of final figures July 11.

Demand

The slowdown in the pace of US annual PCE price inflation is encouraging; however, the rise in the core measure does not indicate further progress towards the Federal Reserve’s 2 percent inflation objective. The Federal Reserve will remain on hold as it continues to assess the balance of risks to the economy, and if the impact of tariffs on prices will be short-lived or more persistent.

U.S. personal income fell 0.4 percent in May, partially erasing a 0.7 percent increase in April (revised from +0.8 percent) and far below expectations for a 0.3 percent rise in the Econoday survey of forecasters.

Consumer spending, as measured by the Personal Consumption Expenditures (PCE) index, contracted by 0.1 percent last month, following a 0.2 percent increase in April. The bulk of demand was pulled forward, especially for goods, as consumers raced to beat the imposition of the Trump administration’s punitive tariffs.

As for the Federal Reserve’s preferred inflation gauge, the PCE price index was up by just 0.1 percent on a monthly basis in May, the same rate as in April and following no change in March.

Prices for goods saw a 0.1 percent uptick and prices for services increased at a 0.2 percent rate. Food prices rose 0.2 percent and energy prices declined 0.1 percent. Excluding food and energy, the PCE price index was up 0.2 percent, following a 0.1 percent rise in April.

Compared to a year ago, the May PCE price index rose 2.3 percent after a 2.2 percent increase in April. Prices for goods are up by just 0.1 percent and the cost of services jumped 3.4 percent. The core PCE price index is up 2.7 percent from May 2024, compared to April’s 2.6 percent year-over-year increase.

Expectations in the Econoday survey were for a 0.1 percent monthly increase and a 2.3 percent rise on an annual basis.

Sentiment

The bump in US consumer confidence from the May 12 trade war truce between China and the United States was short-lived.

The Conference Board’s Consumer Confidence Index took a step back in June to 93.0, down from a revised 98.4 (previously 98.0) in May, and below expectations of 99.0 in the Econoday survey of forecasters.

Consumers’ assessment of current business and labor market conditions soured, while their short-term outlook for income, business, and labor market conditions remained pessimistic – and well below the threshold that indicates a recession ahead.

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices. Inflation and high prices were another important concern cited by consumers in June,” the report said. “References to geopolitics and social unrest increased slightly from previous months but remained much lower on the list of topics affecting consumers’ views.”

U.S. consumers had a less optimistic assessment of current business conditions, while their views on job availability weakened for the sixth straight month. “Consumers were more pessimistic about business conditions and job availability over the next six months, and optimism about future income prospects eroded slightly,” the Conference board said.

The Conference Board said the share of consumers expecting a recession over the next 12 months “rose slightly” in June and remains above 2024’s levels.

Average one-year inflation expectations fell to 6 percent in June from 6.4 percent in May.

On a six-month moving average basis, purchasing plans for autos jumped to the highest level since December 2024, while plans to buy a home declined. Likewise, plans to buy big-ticket items were mixed, while intentions to purchase services in the coming months weakened compared to May, with almost all services categories declining.

Business Surveys

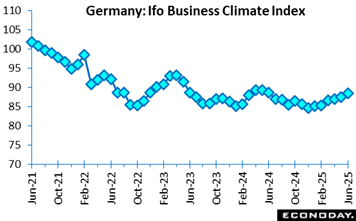

Germany’s business sentiment gained traction in June 2025, with the business climate index climbing to 88.4 from 87.5 in May, its highest level this year. The uplift was driven primarily by improved expectations across sectors, signalling a cautious return of confidence in Europe’s largest economy. Although current conditions improved only slightly, the overall mood reflects growing optimism.

In manufacturing, sentiment edged up, but firms continued to express frustration with weak order books, suggesting demand-side challenges remain. In contrast, the service sector saw a notable boost, especially among business service providers who reported better outlooks and stronger current conditions, an encouraging sign for domestic economic activity.

The trade sector also saw improvement, thanks to wholesaling. However, retail trade lagged slightly, hinting at uneven consumer demand. Meanwhile, the construction sector sustained its gradual rebound, with future expectations reaching a post-pandemic high, though firms remain wary about persistent risks.

Indeed, the latest update paints a stabilising picture of the German economy, with optimism returning in most sectors despite lingering structural challenges. The divergence between expectations and current conditions suggests that while confidence is rebuilding, tangible recovery may still take time.

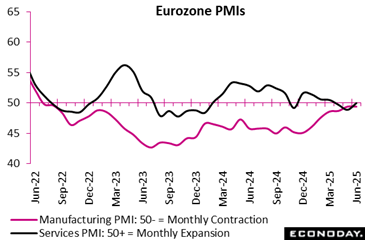

The Eurozone economy showed that the composite PMI remained steady at 50.2, marking a sixth straight month of marginal growth. While the headline figure suggests stability, the underlying picture reveals an economy cautiously shifting gears. Manufacturing maintained a slow but steady expansion in output (49.4), now four months running, even as services activity stabilised (50.0) after dipping in May. Encouragingly, new orders nearly flatlined, marking the mildest decline in over a year, while export orders fell only slightly, hinting at improving demand conditions.

Employment edged up again, fuelled by modest gains in services, though manufacturing job losses intensified. Notably, Germany rebounded in new foreign business for the first time in nearly 3.5 years, underscoring emerging green shoots in Europe’s industrial powerhouse.

Price trends diverged. Input inflation continued to cool, especially in manufacturing, yet selling prices rose faster than in May, led by strong price hikes in services. Manufacturers cut output prices, responding to weak cost pressures and tepid demand.

Optimism improved across the bloc, particularly in services, lifting sentiment to its highest since January. Despite regional contrasts, the Eurozone seems poised for a cautious but broadening recovery into the second half of 2025.

US Review

Fed’s Powell Repeats Policy on Hold; Second Quarter Looking Softer

By Theresa Sheehan, Econoday Economist

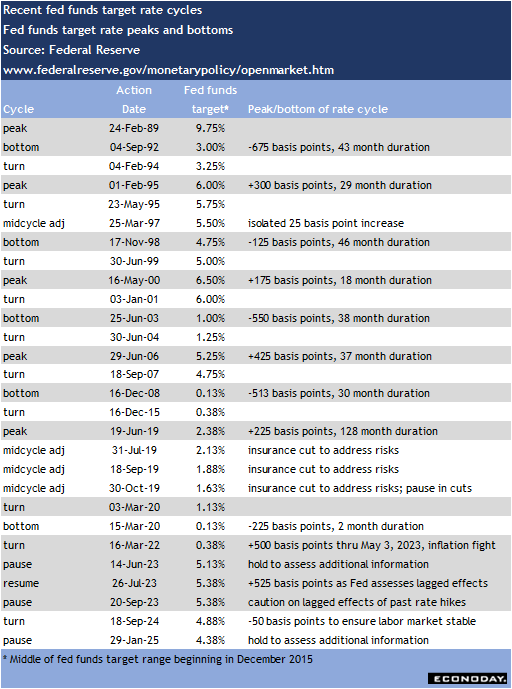

Fed Chair Jerome Powell’s semi-annual monetary policy testimony was delivered against a backdrop of political partisanship and geopolitical uncertainty. Powell gave essentially the same message on Tuesday and Wednesday that he did at his June 18 press conference. To wit, that the US economy continues to grow modestly, that the labor market is “solid”, and that underlying inflation remains “somewhat elevated”. He reiterated that the FOMC is both data-dependent and forward-looking. The present economic data is not a cause for alarm about the health of the economy, while unsettled trade and tariff policy leaves a lot of unknows on the near horizon.

The patience on the part of the FOMC before lowering rates may in part be a desire to avoid one of those mid-cycle adjustments that have been so poorly received in the past when signals from the data suggest the FOMC has raised or cut rates too soon.

Prior to the release of the third estimate of first quarter GDP, Powell noted the “unusual swing” in the net exports component of GDP that has “complicated” measuring growth. That complication was on display when the BEA released the report on Thursday which was a downward revision to negative 0.5 percent growth. Powell highlighted PDFP – private domestic final purchases – which was up 2.5 percent in the first quarter.

If underlying growth remained “solid” in the first quarter as Powell said, there are signs of weakening in the second quarter. Downward revisions to personal consumption expenditures to up 0.5 percent in the first quarter 2025 after 4.0 percent in the fourth quarter 2025 speak to softening consumer demand. The front-loading of buying hard goods – often big-ticket items like motor vehicles and appliances – as exhausted demand and low confidence is unlikely to refresh it. The rush for businesses to buy equipment and lock in contract pricing in the first quarter will remove those investments in the second quarter.

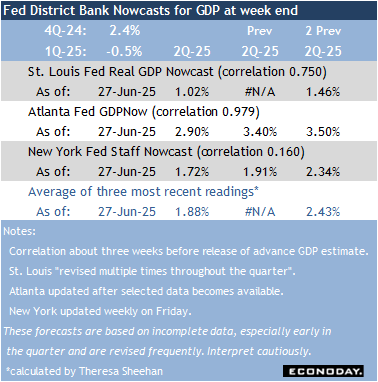

Early forecasts for growth in the second quarter took a hit with the Friday release of the data on personal income and spending in May. The Atlanta Fed’s GDPNow measure was revised lower to up 2.9 percent in the second quarter from 3.4 percent in the prior forecast. If the most reliable of the three Fed district bank estimates of GDP is signaling a loss of momentum in the data at the mid-point of the second quarter, then more soft numbers for June could erode it further. Trade flows may be more normal in the second quarter, but this won’t disguise weaker consumer spending and business investment.