Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

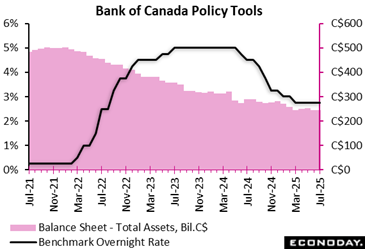

The Bank of Canada left its target interest rate unchanged at 2.75 percent for the third consecutive meeting, as expected by forecasters in an Econoday survey. The central bank cited the resilience of the Canadian economy and ongoing pressures on core inflation, adding it continues to proceed “carefully.”

In his opening statement of a press conference following the policy announcement, Governor Tiff Macklem said, “At this rate decision, there was clear consensus to hold our policy rate unchanged.” The minutes of the June meeting had pointed out “some diversity of views on the most likely path ahead”.

The impact of trade policy and related uncertainty on Canada’s economic activity and inflation remains the key determinant for the interest rate path forward. “If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate,” the BoC said.

It continues to monitor the impact of U.S. tariffs on Canadian exports, how this in turns spills over to business investment, employment and consumer spending. As it mentioned in its June statement, the Bank also continues to assess the extent and speed at which businesses pass on cost increases to consumers while monitoring inflation expectations.

Overall, in the face of the ongoing unpredictability of U.S. trade actions despite some “more concrete” elements in recent weeks, the central bank continues to avoid providing its conventional base case scenario, offering three possible paths instead: the current scenario, an escalation scenario, and a de-escalation scenario.

Under the current scenario based on tariffs already in place, Canada’s GDP growth contracts in the second quarter of 2025. It recovers to about 1 percent in the second half of this year as exports stabilize and household spending increases gradually. Weakness continues next year before growth picks up to close to 2 percent in 2027. Inflation, currently at 1.9 percent, remains close to 2 percent throughout the horizon as upward and downward pressures offset each other.

Under the de-escalation scenario, GDP growth rebounds faster and inflation is expected to remain below the 2% target until late 2026. Inflation would average around 2 percent in 2027.

Under the escalation scenario, growth contracts through the end of 2025. CPI inflation is projected to peak at just above 2.5% in the third quarter of 2026, before receding to around 2 percent in 2027.

In all three scenarios, the neutral nominal rate is assumed to be between 2.25 percent and 3.25 percent. At 2.75 percent, the current policy rate sits at the middle of the neutral range.

Overall, the central bank left the door open to further rate cuts to support growth as long as inflation can remain under control.

The BoC made its announcement as uncertainty remains around the outcome of the most recent round of trade negotiations. U.S. President Donald Trump set an Aug. 1 deadline for reaching a deal, without which he said it will impose 35 percent tariffs on Canadian goods. Prime Minister Mark Carney has recently shifted his messaging to signal that some level of tariffs will remain.

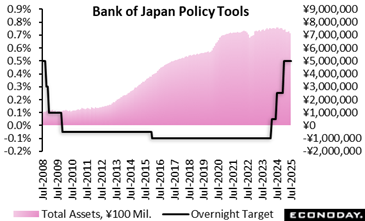

–The Bank of Japan’s nine-member board voted unanimously to maintain the target for the overnight interest rate at 0.5% for the fourth straight meeting after hiking it by 25 basis points (0.25 percentage point) in January amid uncertainty over trade rows.

–The bank will continue raising rates if growth and inflation evolve in line with its medium-term outlook but it is still in the process of normalizing its monetary policy stance from years of keeping short-term rates near zero percent.

–In its quarterly Outlook Report, the board left its growth forecasts little changed for fiscal years 2025, 2026 and 2027 (ending in March 2028) while revising up its inflation outlook sharply for the current fiscal year and seeing tame price rises in fiscal 2025 and 2026 as projected in the April report.

–The BOJ also noted that risks to its GDP outlook is skewed to the downside, as predicted in April, but said risks to its CPI projection is “generally balanced,” compared to the April statement that it was skewed to the downside.

–The BOJ continues to expect Japan’s economy will settle around 2% inflation. “In the second half of the projection period (fiscal 2025 through fiscal 2027), underlying CPI inflation is likely to be at a level that is generally consistent with the price stability target, it said, repeating its previous report issued on May 1.

The median projections by the board from its quarterly Outlook Report:

FY25 core CPI (ex-fresh food) +2.7% vs. +2.2% in May

FY26 core CPI (ex-fresh food) +1.8% vs. +1.7% in May

FY27 core CPI (ex-fresh food) +2.0% vs. +1.9% in May

FY25 GDP +0.6% vs. +0.5% in May

FY26 GDP +0.7% vs. +0.7% in May

FY27 GDP +1.0% vs. +1.0% in May

–The board repeated that “Japan’s economic growth is likely to moderate” as trade and other policies lead to a slowdown in overseas economies and to a decline in domestic corporate profits despite support from accommodative financial conditions. “Thereafter, Japan’s economic growth rate is likely to rise, with overseas economies returning to a moderate growth path,” it said.

–Board members warned that there are various risks to their outlook. “In particular, it remains highly uncertain how trade and other policies in each jurisdiction will evolve and how overseas economic activity and prices will react to them,” the BOJ said. “It is therefore necessary to pay due attention to the impact of these developments on financial and foreign exchange markets and on Japan’s economic activity and prices.”

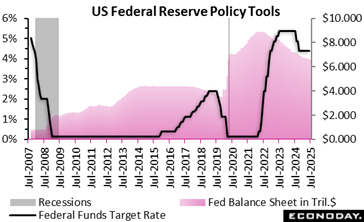

The FOMC left the fed funds target rate range unchanged at 4.25 to 4.50 percent, as expected. There are only minor tweaks to the statement compared to that issued at the prior meeting. The statement noted the continuing impact that the unusual movements in international trade have had on the GDP data and offered a slightly less upbeat assessment of economic activity. There was no change in the language regarding the labor market and inflation. The statement said, “Although swings in net exports continue to affect the data, recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.”

The statement also said, “Uncertainty about the economic outlook remains elevated.” The language about diminished uncertainty in the prior statement was removed.

The vote at the end of the meeting included two dissents from Governors Michelle Bowmand and Christopher Waller who both preferred a 25 basis point cut in the fed funds rate. It is unusual for a governor to dissent, and two governors have not dissented in a meeting vote since the 1990’s. The vote was 9-2 with Governor Adriana Kugler absent and not voting.

Employment

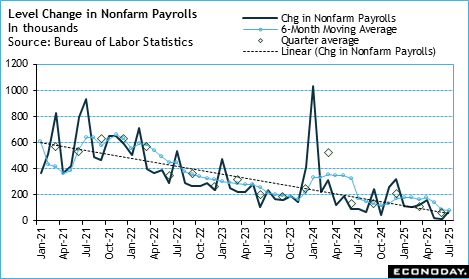

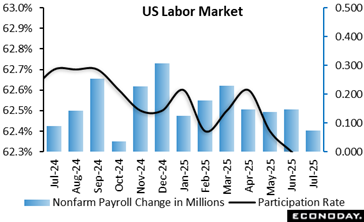

The monthly US employment report has significant revisions that paint conditions in the labor market as much weaker than previously thought and reshapes the outlook for monetary policy. The rapid cooling in hiring and small rise in the unemployment rate make a rate cut at the September 16-17 FOMC meeting much more likely unless the next round of inflation reports are particularly alarming.

Nonfarm payrolls are up 73,000 in July after increases of 14,000 in June and 19,000 in May. July nonfarm payrolls are below the consensus of up 110,000 in the Econoday survey of forecasters. The July increase is not materially different from the second quarter monthly average of up 64,000, or the six-month moving average of up 81,000. However, the last three months of hiring represents an abrupt slowdown from the fourth quarter 2024 average of up 209,000 and first quarter 2025 average of up 111,000.

The BLS noted, "Revisions for May and June were larger than normal. The change in total nonfarm payroll employment for May was revised down by 125,000, from +144,000 to +19,000, and the change for June was revised down by 133,000, from +147,000 to +14,000. With these revisions, employment in May and June combined is 258,000 lower than previously reported."

Private payrolls are up 83,000 in July. Goods-producers’ payrolls are down 13,000 with manufacturing down 11,000 and mining down 4,000, while construction added 2,000 jobs. Service-providers added 96,000 jobs in July, the majority of which are from hiring 73,300 in health care and social assistance.

Government jobs are down 10,000 in July due to declines of 12,000 at the federal level and 3,000 in local government. State governing hiring is up 5,000.

Average hourly earnings are up 0.3 percent in July from June and up 3.9 percent year-over-year. Monthly increases in average hourly earnings remain modest and the year-over-year change has been essentially the same since January.

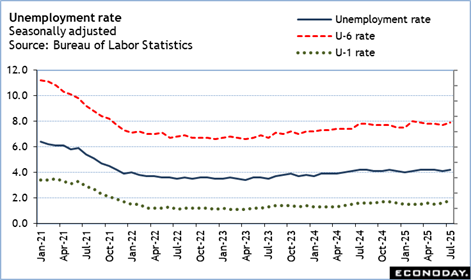

The unemployment rate is up a tenth to 4.2 percent in July due to a 260,000 decline in the number of people employed and an increase of 221,000 in the number of unemployed. The U-6 rate – the broadest measure of unemployment – is up two-tenths go 7.9 percent in July and indicates more workers are discouraged about finding jobs.

GDP

Economic growth in the euro area cooled slightly in the second quarter of 2025, with GDP edging up by just 0.1 percent compared to the previous quarter, a masked contrast to the forecasts of minus 0.1 percent. This marks a notable slowdown from the first quarter’s stronger 0.6 percent expansion, hinting at growing caution across the bloc amid persistent economic uncertainty.

Year-over-year, the economy maintained moderate momentum, with GDP rising by 1.4 percent, a slight dip from the previous quarter’s 1.5 percent. This suggests that, while the region remains on a growth path, it is navigating a more fragile recovery phase, reflecting economic policy and trade uncertainties affecting the bloc.

Within the region’s quarterly advance, France expanded 0.3 percent after 0.1 percent, while Spain grew 0.7 percent after 0.6 percent. However, Germany fell by minus 0.1 percent after 0.3 percent, while Italy also fell by minus 0.1 percent after 0.3 percent.

These updates offer an early signal that the eurozone’s recovery is still intact, though losing pace. The minimal quarterly gain highlights the need for vigilance among policymakers and investors, especially as consumer confidence and investment sentiment become more crucial in steering the region’s short-term economic direction.

U.S. economic activity rebounded in the second quarter of 2025, as the significant drop-off in goods imports, coupled with a notable increase in consumer spending, drove the increase in real GDP. Further reason for the Federal Reserve to hold off on cutting the federal funds rate at the conclusion of the FOMC meeting today.

Q2 GDP increased by 3 percent, more than offsetting the 0.5 percent decline in the first quarter and beating expectations for a 2.5 percent rise in the Econoday survey of forecasters.

Consumer spending as measured by Personal Consumption Expenditures was up 1.4 percent in Q2 following just a 0.5 percent uptick in the first quarter, while the demand for imports plunged 30.3 percent after Q1’s 37.9 percent surge.

However, exports were also down last quarter – tempering the increase in economic activity. The decline was by 1.8 percent, cancelling out 0.4 percent growth in the first quarter. Gross domestic private investment also plummeted, down 15.6 percent – more than half of Q1’s 23.8 percent jump.

US Review

Weak Jobs Report Puts Rate Cuts Back on Table for September

By Theresa Sheehan, Econoday Economist

The July Employment Situation presents a large downside surprise. Not only was the 73,000 increase in nonfarm payrolls below the Econoday consensus forecast of up 110,000, but there was a huge net revision lower of 258,000 for the prior two months. The mediocre increase in July payrolls on top of the reset to job gains in the past two months changes the outlook for monetary policy.

The FOMC will have to reassess the risks to maximum employment, especially if the preliminary benchmark revision scheduled for release on September 9 also affirms that job gains are lower than previously thought. Had the July employment data been available on July 30, a rate cut would have been almost assured. As it is, the Fed policymakers may find the risks to inflation from tariffs are less compelling when they next meet on September 17-18. Of course, this will be dependent on the data reports set for release in the intermeeting period.

In any case, hiring has cooled abruptly and significantly, and to the point where it suggests that businesses are not only not hiring but that they will soon be cutting current staffing.

The one-tenth uptick to 4.2 percent in the July unemployment rate is well within normal month-to-month variation. However, it should not be dismissed out of hand. In the context of the two-tenths rise in the U-6 unemployment rate to 7.9 percent, it feels like the beginning of an upward trend. The unemployment rate has pegged at 4.2 percent in four of the past five months and is at the top of the narrow range of 4.0 percent to 4.2 percent that has prevailed for the past 20 months.

It is also notable that the unemployment rate for those unemployed 15 weeks or longer is up to 1.8 percent in July after 1.6 percent in June and 1.5 percent in May. Periods of unemployment are lengthening.