Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

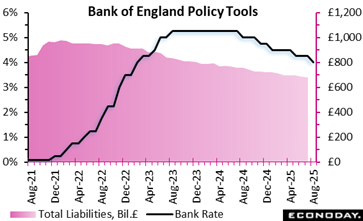

In a finely balanced 5–4 decision, the Bank of England’s Monetary Policy Committee opted to cut the Bank Rate to 4 percent, signaling cautious optimism in the disinflation journey. This move reflects a growing belief that the worst of inflation may be behind, even as short-term pressures persist. Inflation has edged up to 3.6 percent and is forecast to peak at 4 percent in September due to energy, food, and administered prices. However, beneath the surface, pay growth is easing and economic slack is emerging, with weak GDP growth and rising unemployment suggesting a softening labour market.

Divisions within the committee highlight differing priorities. Some members pushed for a larger rate cut to support faltering demand and mitigate recession risks, while others remained wary of sticky inflation expectations, especially from households reacting to high food and energy costs. The vote captures a turning point. The economy is no longer overheating, but confidence in disinflation is not yet unanimous.

Markets had largely anticipated the cut, and with no pre-set path for policy, future moves will hinge on how quickly inflationary pressures abate. This rate cut, although modest, represents a deliberate shift from tight policy towards a more growth-sensitive stance.

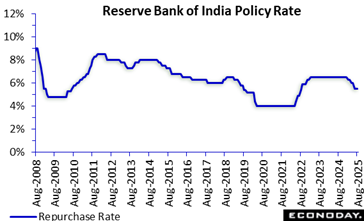

The Reserve Bank of India’s Monetary Policy Committee has left its benchmark repurchase rate on hold at 5.50 percent at its policy review held today, in line with the consensus forecast. Officials cut this rate by 100 basis points over the previous three meetings after the rate had been left on hold for two years.

Data released since the RBI’s previous meeting in June have shown headline CPI inflation moderating from 3.16 percent in April to 2.82 percent in May and 2.1 percent in June, back below the mid-point of the RBI’s target range of two percent to six percent. This decline was anticipated by officials and largely reflects the impact of food prices. PMI survey data have shown strong conditions, though industrial production growth has moderated in recent months.

In the statement accompanying today’s decision, RBI officials again highlighted the recent decline in inflation and advised that favourable weather conditions will likely further reduce food inflation pressures. With the near-term inflation outlook now “more benign than anticipated earlier officials have lowered their inflation forecasts for this fiscal year from 3.7 percent to 3.1 percent. Officials expressed concerns about “headwinds emanating from prolonged geopolitical tensions” the impact of a “challenging global environment” but expressed confidence that domestic demand will be supported by supportive monetary and fiscal policy and “congenial financial conditions.” They forecast GDP growth of 6.5 percent this fiscal year.

Reflecting this assessment, officials concluded that policy settings should be kept on hold today as they “wait for further transmission of the front-loaded rate cuts to the credit markets and the broader economy.” They also announced that they retain the policy stance as “neutral” as they consider incoming data.

Demand

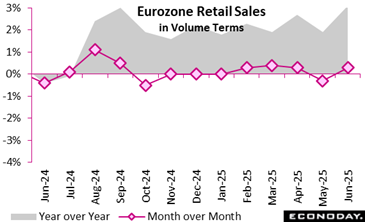

Retail activity in the euro area showed modest but encouraging growth in June 2025, signaling a slight rebound in consumer confidence. Retail trade volume rose by 0.3 percent month-over-month, reversing the 0.3 percent decline recorded in May. On an annual basis, the retail index climbed by a notable 3.1 percent, reflecting healthier consumer demand compared to June 2024.

Across categories, all segments contributed positively to this growth. Non-food products (excluding automotive fuel) led the way with a 0.6 percent monthly increase, suggesting stronger discretionary spending. Automotive fuel sales rose by 0.4 percent, and food, drinks, and tobacco edged up by 0.2 percent, pointing to steady essentials-based consumption.

The year-over-year data further confirms this positive momentum as non-food products surged by 4.3 percent, while automotive fuel and food-related sales increased by 4.0 percent and 1.7 percent respectively. This broad-based growth hints at easing inflationary pressures and a cautiously improving consumer outlook.

Overall, June’s data paints a picture of a retail sector regaining stability, fueled by a blend of necessity-driven and lifestyle purchases, offering a welcome signal of resilience amid wider economic uncertainty.

Production

New orders in German manufacturing declined by 1.0 percent compared to May, driven largely by a steep drop in large-scale transport equipment orders (minus 23.1 percent) and setbacks in the automotive (minus 7.6 percent) and metal product industries (minus 12.9 percent). However, when excluding these large-scale orders, the picture improves slightly, with a modest 0.5 percent rise month-over-month.

Year-over-year data reveals a stark contrast. While June saw only a 0.6 percent increase from June 2024, May had reported a robust 6.3 percent growth over the previous year, partly due to a late-reported major order that revised earlier figures.

On a more positive note, intermediate goods rose by 6.1 percent, consumer goods by 0.5 percent, and electrical equipment soared (23.5 percent), helping to cushion the decline. Domestic demand also showed resilience, climbing 2.2 percent, although foreign orders dropped 3.0 percent, weighed down by a 7.8 percent fall from outside the euro area.

Despite weaker orders, real turnover in manufacturing grew by 0.9 percent in June, suggesting production processes remained active. Overall, the data reflect underlying volatility and dependence on high-value transport orders, with moderate domestic strength balancing global demand weaknesses.

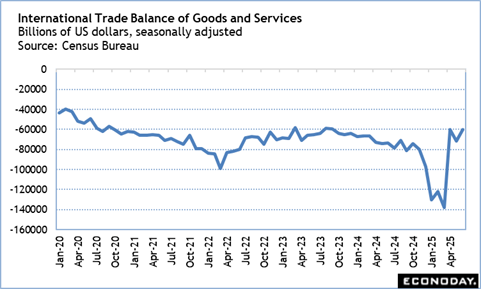

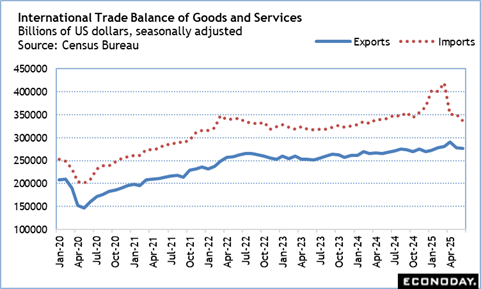

International trade

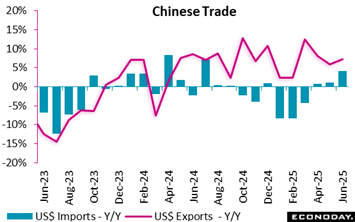

China’s merchandise trade surplus in US dollar terms was $98.24 billion in July, narrowing from $114.77 billion in June but well above the level of $84.65 billion recorded in July 2024. Exports rose 7.2 percent on the year in July after increasing 5.8 percent in June, while imports rose 4.1 percent, picking up from a previous increase of 1.1 percent.

Although the data showed further weakness in Chinese exports to the United States, down 22 percent on the year, this was outweighed by stronger shipments to other major trading partners. This may, in part, reflect the re-routing of exports ultimately destined for the United States as part of efforts to avoid the impact of higher tariffs imposed on China by the Trump Administration. Stronger exports to south-east Asia and Latin America, in particular, may be partly driven by this practice.

Business Surveys

U.S. services sector activity decelerated in July, with growing concern about employment and growing inflationary pressures.

The ISM Services purchasing managers index dipped to 50.1 in July from 50.8 recorded in June and below the 51.5 expected in the Econoday survey of forecasters.

“July’s PMI level continues to reflect slow growth, and survey respondents indicated that seasonal and weather factors had negative impacts on business,” the report said. “The Employment Index’s continued contraction and faster expansion of the Prices Index are worrisome developments.”

The Business Activity Index showed expansion for July, but at a slower pace compared to June. New orders also expanded at a slower rate, while employment shrank for the fourth time in the last five months.

Prices jumped compared to June and remain elevated (the July price reading is the highest since October 2022).

US Review

Trade Balance Swings Back in 2Q after Bump in Q1; Trump Gets Opening at Fed Board

By Theresa Sheehan, Econoday Economist

The international trade balance for June in addition to the trade balances in April and May points to a narrowing in the trade deficit in the second quarter 2025 after a massive widening in the first quarter. The first quarter saw businesses stocking up on hard goods in advance of expected big hikes in tariffs that would make imports more costly – in some instances much more so. That has more or less ended, although still unsettled tariff policy may see bursts of activity to take advantage of periods when the imposition of tariffs are delayed.

It is a little hard to parse out where changes the dollar value of imports and exports are due to higher or lower prices, or changes in exchange rates, or to the volume of goods and services.

What can be said is that the upward trend for exports appears to be moderating while the bump in demand for imports does not appear to have significantly weakened the underlying trend. However, trade agreements and tariff policy remain unstable and leave businesses and consumer in a fog of uncertainty.

With the departure of Federal Reserve Governor Adriana Kugler, there is an opening on the Fed board for the currently unexpired term ending January 31, 2026. Whoever is appointed to replace Kugler will fill out the last months of that term. It would be a normal practice to approve the nominee for the subsequent 14-year term ending January 31, 2040. However, that must be explicit in the formal nomination sent to the Senate. President Trump has said he will nominate the current chair of the Council of Economic Advisors Stephen Miran to fill the remaining six months.

There is little reason to think that the vote in the full Senate will not approve this nomination once the confirmation process is complete. The addition of a Trump partisan to the board of governors is a development that will add to questions about the Fed’s independence. This is especially the case after Governor Christopher Waller – touted as a possible successor to Chair Jerome Powell – and Vice Chair for Supervision Michelle Bowman dissented in the vote of the July 29-30 FOMC meeting. Waller and Bowman are both Trump appointees. Both agree that the price increases from tariffs will be short-lived and feed inflation over the longer term. Miran would share their views.