Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

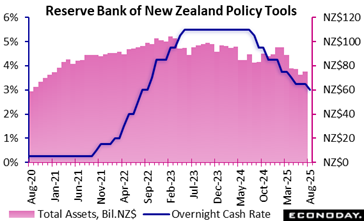

The Reserve Bank of New Zealand’s Monetary Policy Committee has reduced the official cash rate by 25 basis points to 3.00 percent, in line with the consensus forecast. Officials have lowered policy rates by a cumulative 250 basis points over their previous eight meetings after an extended period of restrictive policy settings.

In the statement accompanying the decision, officials noted that price pressures are moderating and expressed confidence that inflation is likely to return to around the middle of their target range of 1 percent to 3 percent by mid-2026. Although they expect domestic growth will be supported by previous policy easing, they cautioned that global uncertainty and weaker house prices may slow the pace of economic recovery.

Reflecting this assessment, officials decided that that it was appropriate to cut policy rates again today. They also advised that if medium-term inflation pressures ease as they anticipate, they will likely cut the cash rate further in coming meetings.

Inflation

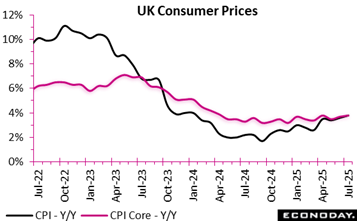

The July 2025 UK inflation report shows a modest but notable upward movement in consumer prices. CPI rose to 3.8 percent annually, compared with 3.6 percent in June and 0.1 percent above the consensus forecast, driven mainly by transport costs, especially air fares, which added upward pressure. However, this was partly offset by housing and household services, particularly owner occupiers’ housing costs, which kept CPIH increases relatively contained.

On a monthly basis, CPI inched up by 0.1 percent, contrasting with a fall recorded a year earlier, signalling firmer price momentum.

Core inflation remained sticky, with CPI at 3.8 percent and CPIH at 4.2 percent on an annual basis, reflecting persistent demand-side pressures beyond volatile energy and food. Goods inflation picked up slightly, while services inflation remained stronger, with CPI services rising to 5.0 percent and CPIH services holding steady at 5.2 percent.

These figures indicate that while inflationary pressures are not accelerating sharply, underlying price stickiness in services may complicate the path toward stabilisation. Indeed, July’s data suggest that the balance between transport-driven price increases and housing-related relief remains fragile, pointing to the need for continued vigilance in monetary and fiscal policy responses.

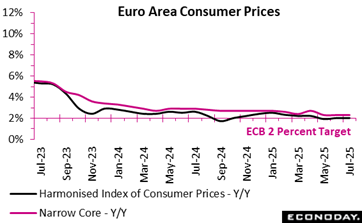

Euro area inflation held steady at 2.0 percent in July 2025, unchanged from June but notably lower than the 2.6 percent recorded a year earlier, reflecting a gradual easing in price pressures. Over the month, however, there were no changes in the inflation numbers within the zone, reflecting stability.

Services remained the dominant driver, adding 1.46 percentage points to the headline rate, underlining persistent cost pressures in labour-intensive sectors. Food, alcohol and tobacco contributed a further 0.63 points, showing that households continue to face elevated grocery bills. Non-energy industrial goods added 0.18 points, indicating moderate price gains in manufactured items. By contrast, energy exerted a negative contribution (minus 0.23 points), reflecting lower fuel and utility costs that helped offset upward pressure elsewhere.

Beneath the stability, inflation dynamics varied across member states: eight countries saw declines, six held steady, while thirteen experienced an uptick, signalling uneven progress in price stability across the bloc. Across the top four economies in the area, inflation fell in Germany (1.8 percent after 2.0 percent) and Italy (1.7 percent after 1.8 percent), but rose in Spain (2.7 percent after 2.3 percent), while it remained constant in France (0.9 percent after 0.9 percent) on an annual basis.

As a result, the overall picture suggests that while headline inflation has returned to the European Central Bank’s 2 percent target, the composition points to stubborn service-sector inflation.

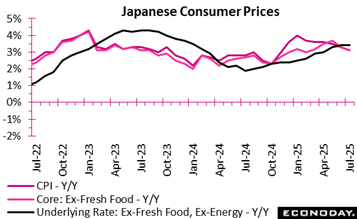

Japan CPI: All as expected, high inflation is hurting households whose main rice earners see real wages fall for the seventh straight month in June (revised labour survey just out – total monthly average cash earnings per regular employee were up 3.1% vs initial +2.5% but wages after adjusted for inflation slipped 0.8% vs. prelim -1.3%)

–Consumer inflation in Japan eased further in July to just above 3% in two key measures, thanks to retail gasoline subsidies which has offset the continued uptick in processed food costs. The yen’s rise from last year’s slump has also lowered import costs and sparked a pullback in spending by visitors from overseas who lost their currencies’ competitive edge over the yen.

–The core reading (excluding fresh food) posted a 3.1% rise on year in July after its annual rate decelerated to 3.3% in June from 3.7% in May. The year-on-year rise in the total CPI also moderated to 3.1% from 3.3% in June and 3.5% previously. The underlying inflation measured by the core-core CPI (excluding fresh food and energy) stood at 3.4% after rising to a 17-month high of 3.4% from 3.3%.

–The impact of slowing overall energy price gains (gasoline has been down) was mitigated by elevated processed food prices despite gradually easing domestic rice supply shortages. Regular rice prices rose as high as 90% y/y but that is slightly lower than over 100% (double) earlier this year. The prices of chocolate remain high, up 51%, while those of coffee beans climbed 44%.

Takeaway:

The current high inflation rate is not fully backed by domestic demand (wage-heavy services price hikes lag behind goods price gains) but largely pushed up by higher import costs. This means that inflation in Japan is not accompanied by sustained and substantial wage growth and that underlying inflation, estimated by the Bank of Japan to be around 1.5%, just below the bank’s 2% price stability target. The bank is in the process of normalizing its policy stance after a decade-long large-scale easing period through 2022 and is set to continue gradually raising the overnight interest rate from the current level of 0.5%. Officials argue that real borrowing costs remain "significantly negative" because the BOJ has been cautious about raising rates even when inflation expectations are rising moderately.

GDP

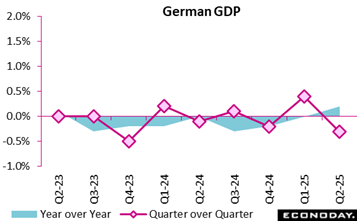

Germany’s economy slipped back into contraction in the second quarter of 2025, with GDP falling by 0.3 percent from the previous quarter and 0.2 percent lower than the same period a year earlier (price and seasonally adjusted). Revised figures show that weaker-than-expected industrial output, coupled with a sharp downturn in construction (minus 3.7 percent), dragged growth into negative territory.

Household consumption offered little relief, edging up by just 0.1 percent, while government spending (0.8 percent) was the only notable domestic support. Capital formation suffered a significant setback, particularly in machinery (minus 1.9 percent) and construction investment (minus 2.1 percent). External trade compounded the weakness, as exports declined (minus 0.1 percent) and imports surged (1.6 percent).

On a yearly basis, household and government consumption provided modest growth (1.2 percent and 2.1 percent), yet this was outweighed by steep declines in investment and goods exports minus 3.6 percent). Employment remained stable at 46 million, but productivity gains were uneven, reflecting reduced hours worked. The savings ratio dropped to 9.7 percent as consumption grew faster than incomes.

Compared internationally, Germany’s performance lagged behind Spain (0.7 percent), France (0.3 percent) and the US (0.7 percent), underlining its fragile recovery. Overall, the latest update demonstrate an economy weighed down by weak industry, lowering investment, and global trade headwinds, with consumption alone preventing a deeper downturn.

International trade

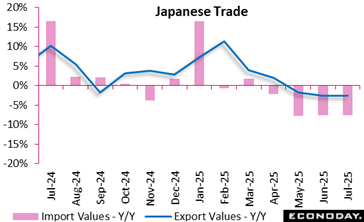

Japan trade data:

–Japanese export values -2.6%, the third straight y/y drop in July -0.5% in June and -1.7% (the first decline in eight months) in May. Japanese carmakers are reducing the prices for U.S. customers to cover high Trump import tariff costs, exerting downward pressures on overall export prices, but the volumes of Japan’s exports to the world remain on an uptrend. The decline in July export values was led by autos, iron/steel and auto parts.

–Import values -7.5% after marking an unexpected rise in June (+0.3%) and slumping 7.6% in May. The decrease was driven by lower prices for crude oil, coal and liquefied natural gas.

–The trade balance: a deficit of ¥117.55 billion vs. a downwardly revised ¥152.12 billion surplus in June (the first black ink in three months) and a ¥628.34 billion deficit recorded in July 2024.

–Exports to the United States -10.1% y/y, the 4th straight drop (-11.4% the previous month), hit by autos, auto parts and semiconductor-producing equipment; Exports to the European Union -3.4%, the first drop in three months (+3,6%), pushed down by iron/steel, organic compounds and auto parts; Exports to China -3.5% y/y, the 5th straight drop (-4.7%) on slower demand for autos, non-ferrous metals and auto parts.

US Review

Fed’s Powell Sets Stage for Rate Cut

By Theresa Sheehan, Econoday Economist

Fed Chair Jerome Powell’s keynote address at the Kansas City Fed’s annual Jackson Hole Forum eclipsed the economic data for the week.

Powell set the stage for a rate cut at the September 16-17 FOMC meeting while warning – yet again – that monetary policy is not on a preset path, and that its decisions are made at the meeting, not before. He said, “FOMC members will make these decisions, based solely on their assessment of the data and its implications for the economic outlook and the balance of risks. We will never deviate from that approach.” Powell may be making an oblique reference to the dissent in the July 28-29 meeting vote by Governor Christopher Waller and Vice Chair for Supervision Michelle Bowman – both Trump appointees to the Board of Governors. Powell is asserting the independence of Fed policymakers and their distance from politics.

The “tension” between the mandates for maximum employment and price stability has shifted, and the weakening in the labor market may make a rate cut appropriate. Powell provided a nuanced examination of when the unemployment rate remains in the low 4-percent range, mainly due to labor supply falling at the same time labor demand is decreasing.

Powell also spoke in-depth about the risks to price stability from higher tariffs. “The effects of tariffs on consumer prices are now clearly visible,” Powell said. He highlighted that these the effect could be “relatively short lived” but also that these will not show up all at once. Powell called this a “reasonable base case” for inflation, but “It will continue to take time for tariff increases to work their way through supply chains and distribution networks. Moreover, tariff rates continue to evolve, potentially prolonging the adjustment process.”