Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

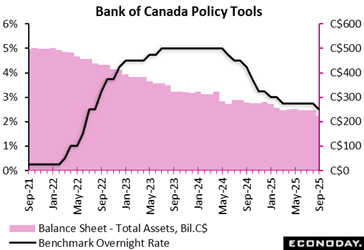

As expected, the Bank of Canada cut its key policy rate by 25 basis points to 2.50 percent Wednesday, citing a “weaker economy and less upside risk to inflation.”

In his statement, Governor Tiff Macklem cited three developments that have shifted the balance of risks since the July 30 status quo: softening labor market conditions, easing inflationary pressures despite mixed signals, and the removal of most retaliatory tariffs by Canada that lower inflationary risk.

Macklem left the door open for more rate cuts should economic conditions warrant it, noting that the BoC will continue to "look over a shorter horizon than usual, and be ready to respond to new information."

Going forward, the central bank still expects trade tensions to continue to add costs despite the drag on economic activity.

The policy rate had been at 2.75 percent since March, when it was lowered from 3.0 percent.

At 2.50 percent, the policy rate remains slightly above the nominal neutral range of 2.25 to 3.25 percent.

As the BoC proceeds “carefully”, its focus is on risks and uncertainties facing the Canadian economy as it supports growth while ensuring inflation remains under control. The central bank also noted signs of a slowing global economy.

On the inflation front, the BoC pointed out that the upward momentum in monthly core inflation has dissipated even as the Bank’s own measures remain close to 3 percent. The most recent inflation data indeed showed that while headline inflation rose to 1.9 percent in August from 1.7 percent in July, two of the BoC’s own measures of core inflation slowed down to 2.5 percent and 3.0 percent, respectively, with the third remaining stable at 3.1 percent. The average is currently at 2.9 percent. The central bank estimates that, based on broader measures, the underlying inflation rate is around 2.5 percent.

The BoC continues to closely watch the impact of trade on both inflation, actual and expected, and business and household activity.

The Canadian economy contracted at an annualized rate of 1.6 percent in the second quarter as exports collapsed. This was close to the Bank’s projection of a 1.5 percent GDP contraction. The job market has also been rapidly deteriorating, with 65,500 jobs lost in August and 40,800 in July. The unemployment rate now stands at 7.1 percent, the highest since May 2016, excluding the 2020 and 2021 pandemic years. The BoC statement highlighted that job losses have been mainly concentrated in trade-sensitive sectors.

Looking at household spending, the central bank expects slow population growth and the weakness in the labor market to be a drag in months ahead.

A key piece of information missing is the 2025 federal budget, which won’t be tabled until November 4. It remains to be seen how this will impact the central bank’s assessment.

In its July 30 Monetary Policy Report, the central bank provided three scenarios: In the current scenario, Canada and China retaliatory tariffs are assumed to be permanent, while other countries are assumed to not retaliate, fostering high uncertainty into next year. After a decline in the second quarter of 2025, Canada’s GDP grows by about 1 percent in the second half of this year, with exports stabilizing and household spending recovering. GDP growth accelerates to 1.8 percent in 2027. Inflation remains close to 2 percent over the forecasting horizon.

Under its “de-escalation scenario”, the BoC expects Canada and other countries to remove their retaliatory tariffs, and uncertainty decreases. GDP growth rebounds faster and inflation is expected to remain below the 2% target until late 2026. Inflation would average around 2 percent in 2027.

Canada’s federal government recently decided to remove most retaliatory tariffs on imported goods from the U.S., which the BoC expects to lessen upward pressure on goods prices.

By contrast, under the escalation scenario, Canada and China double the value of U.S. goods subject to retaliatory tariffs, with other countries also increasing their tariffs on the U.S. Under this scenario, growth contracts through the end of 2025. CPI inflation is projected to peak at just above 2.5% in the third quarter of 2026, before receding to around 2 percent in 2027.

Inflation

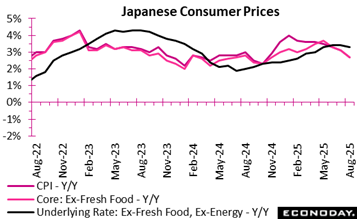

Japan’s core inflation, excluding fresh food, was up 2.7 percent on year in August, matching expectations. That reflected slower gains in prices for processed foods, which have been elevated by rice supply shortages. It also reflected deepening declines in energy prices due to fuel price subsidies.

JAPAN AUG TOTAL CPI +2.7% Y/Y, 48TH STRAIGHT RISE (JULY +3.1%); MEDIAN FORECAST +2.8%

JAPAN AUG CORE-CORE CPI (EX-FRESH FOOD, ENERGY) +3.3% Y/Y, 41ST STRAIGHT RISE (JULY +3.4); MEDIAN FORECAST +3.3%; ABOVE 3% FOR 4 MTHS IN A ROW

JAPAN AUG CPI: PROCESSED FOOD +8.0% (+1.90 POINT) VS. +8.3% (+1.98 PT) IN JULY

JAPAN AUG CPI: ENERGY PRICES -3.3% Y/Y (-0.27 POINT VS. -0.3% (-0.03 PT) IN JULY

JAPAN AUG CPI SERVICES (EX-OWNERS’ EQUIVALENT RENT) +2.1% VS. +2.1% IN JULY; GOODS (EX-FRESH FOOD) +3.8% VS. +4.6%

JAPAN AUG CPI: WAGE GROWTH STILL LAGS BEHIND HIGH COSTS FOR PROCESSED FOOD, UTILITIES, LIKELY KEEPING PRIVATE CONSUMPTION SLUGGISH IN Q3 GDP.

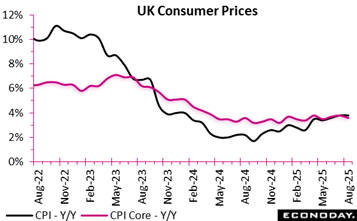

UK inflation held steady in August 2025, with the headline CPI rising 3.8 percent year-over-year, unchanged from July. On a monthly basis, CPI increased by 0.3 percent, mirroring last year’s pace. The broader CPIH measure, which includes owner occupiers’ housing costs, eased slightly to 4.1 percent from 4.2 percent, also recording a modest 0.3 percent monthly rise, lower than the 0.4 percent seen in August 2024.

Air fares provided the biggest drag on inflation, softening the overall figures, while restaurants, hotels, and motor fuels exerted upward pressure, partly offsetting the decline. Core inflation showed signs of cooling. Core CPI slowed to 3.6 percent from 3.8 percent, while Core CPIH slipped to 4.0 percent from 4.2 percent. This suggests underlying price pressures are easing, especially in services, with CPI services inflation falling from 5.0 percent to 4.7 percent and CPIH services from 5.2 percent to 4.9 percent.

Goods inflation, however, inched up slightly from 2.7 percent to 2.8 percent, reflecting persistent cost pressures in certain sectors. Overall, the data signals a stabilisation of inflation, with services cooling but goods showing resilience, an environment that could ease pressure on households while still posing challenges for policymakers seeking a decisive return to target.

Demand

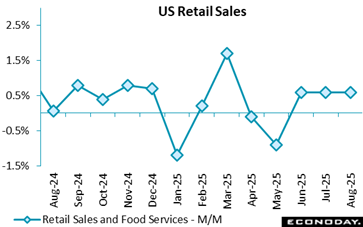

U.S. retail sales came in as stronger than expected in August while July’s reading was revised higher. The underlying data is a mixed bag but paints the picture of decent consumer spending combined with higher prices due to tariffs boosting sales revenues. Still, enough consumer resilience for Federal Reserve officials to cut – although not aggressively – at this week’s FOMC meeting.

U.S. August retail sales jumped 0.6 percent, maintaining the revised 0.6 percent monthly surge reported for July (previously +0.5 percent), and vs. the +0.3 percent consensus in the Econoday survey of forecasters.

Core retail sales, removing autos and gasoline sales, increased 0.7 percent last month following a revised 0.3 percent reading in July (previously reported as +0.2 percent). Core retail sales are up 5.4 percent on an annual basis in August compared to a 4.6 percent y/y jump in July.

Auto sales rose 0.5 percent in August, following July’s 1.7 percent increase, and are up 5.6 percent vs. last year. Activity continues its recovery as consumer demand for affordable car options as prices for new and used cars remain elevated.

Sales were up 1 percent for clothing stores, +0.8 percent for sporting goods, and a 0.3 percent rise in both electronics and grocery sales – all sectors where higher tariffs have filtered through to prices. Even furniture stores and miscellaneous store retailers, despite a monthly dip in sales, saw a 5.2 percent and 10.7 percent spike, respectively, compared to the same month a year ago.

E-commerce sales accelerated by 2 percent increase in August from +0.6 percent in July, and they are 10.1 percent higher than a year ago. This is another tariffs-impacted sector, where increased prices following the elimination of the de minimis exemption for imported goods below $800 has likely inflated sales figures.

Compared to a year ago, August retail sales are up 5 percent, compared to July’s 4.1 percent jump.

Excluding gasoline, retail sales increased 0.6 percent, after July’s 0.6 percent increase, and jumped 5.5 percent from August 2024 vs. +4.6 percent on an annual basis in July.

Stripping out purchases of motor vehicles and parts, sales rose 0.7 percent compared to a 0.4 percent increase (previously +0.3 percent) in July. On an annual basis, retail sales ex-autos are up 4.9 percent, speeding up from July’s 3.9 percent pace.

Production

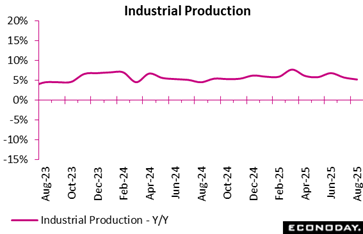

Chinese industrial production rose 5.2 percent on the year in August, slowing from growth of 5.7 percent in July and below the consensus forecast of 5.6 percent. In month-over-month terms, industrial production rose 0.37 percent in July, little changed from an increase of 0.38 percent in July.

Within the industrial sector, manufacturing output rose 5.7 percent on the year in August, also moderating from an increase of 6.2 percent in July. Utilities output and mining output rose 2.4 percent and 5.1 percent on the year respectively, after previous increases of 3.3 percent and 5.0 percent respectively.

In their statement accompanying monthly data published today, officials characterised the data as showing the economy "maintained a generally stable momentum with steady progress" despite "unstable and uncertain factors in external environment”. Officials reiterated their commitment to implement existing macroeconomic policies but provided no specific guidance about whether additional changes to policy settings will be considered in the near-term. Data published today were weaker than consensus forecasts.

US Review

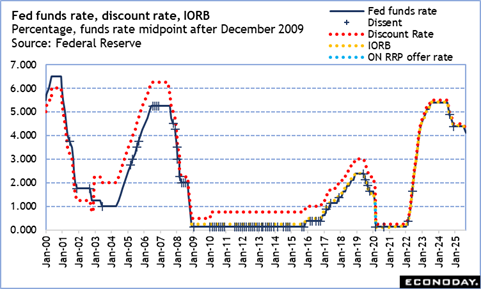

FOMC Delivers As-Expected 25 BP Rate Cut, 11-1

By Theresa Sheehan, Econoday Economist

Going into the September meeting, there were questions about who would be voting. Governor Lisa Cook won her legal challenge and was there and voting. The empty seat on the Board of Governors was filled in short order with the confirmation of Stephen Miran on September 15 and his swearing in before the meeting began on the 16th. Thus, the vote included a full complement of 12 voters.

The FOMC meeting of September 16-17 resulted in a 25-basis point rate cut as expected. The meeting statement tried to balance the increased risks to maximum employment against the halt in progress in bringing inflation down. Conditions have tipped toward the employment side of the dual mandate needing more support with removal of some monetary policy restriction. However, that does not mean that the inflation data is not receiving attention.

Only Miran dissented in the vote, preferring a 50-basis point cut. The dissenters at the previous meeting – Governor Christopher Waller and Vice Chair for Supervision Michelle Bowman – voted with the majority this time, probably because the consensus was that it was time to pick up the pace over the next two meetings.

In his post-meeting press briefing, Fed Chair Jerome Powell noted that at present there is not path for monetary policy that does not involve risk. The FOMC sees the base-case for inflation as one in which current upward price pressures on goods from the imposition of higher tariffs as of short duration. Powel said that so far the pass-through of higher costs to the consumer level has been smaller and is taking longer than previously thought. But he also said that the price increases will reach consumers sooner or later.

Nonetheless, the US economy has so far avoided recession with solid consumer spending. The labor market is adjusting to both diminished labor supply — largely from immigration policy — and a pullback in hiring as businesses navigate uncertain conditions.

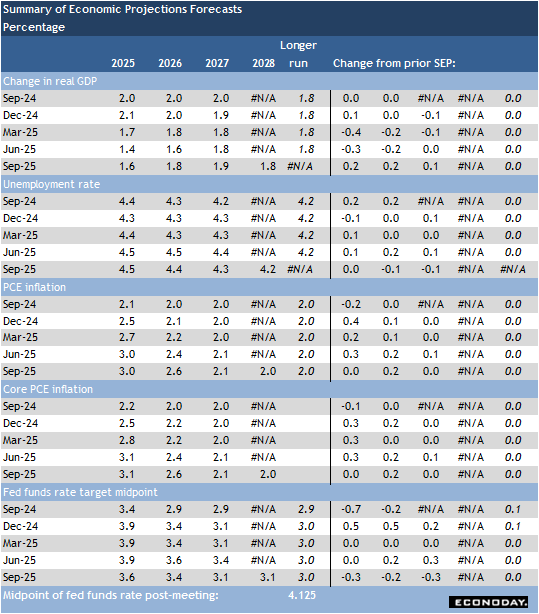

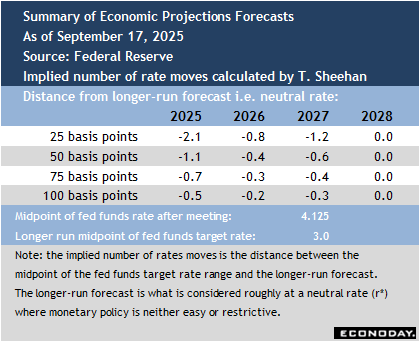

What was somewhat unexpected is that the summary of economic projections did not see much in the way of revisions from the June edition and revisions were small. That the forecast for 2025 GDP was revised up two-tenths to up 1.6 percent was a surprise, along with small upgrades to growth forecasts for the next two years. The was no revision for the forecast of the unemployment rate to end 2025 at 4.5 percent, and forecasts for the next two years were revised higher by only one-tenth. There was no revision to the PCE deflator forecasts of up 3.0 percent and up 3.1 at the core. Inflation forecasts for 2026 were up a bit, but still reflecting a downward trend for inflation.

The most positive news for financial markets was that the mid-point for the fed funds target range is revised down to 3.6 percent from 3.9 percent in the June forecast. This sets up two 25-basis point rates cuts for the October 28-29 and December 9-10 FOMC meetings.