Last Week: Key Global Events

Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

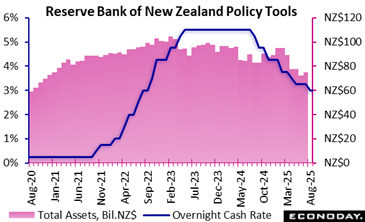

The Reserve Bank of New Zealand’s Monetary Policy Committee has reduced the official cash rate by 50 basis points to 2.50 percent, a bigger cut than the consensus forecast for a reduction of 25 basis points. Officials have lowered policy rates by a cumulative 300 basis points over their previous nine meetings after an extended period of restrictive policy settings.

In the statement accompanying the decision, officials noted that inflation is currently around the top of their target range of 1 percent to 3 percent but expressed confidence it will return to around the mid-point of that range early next year. Recent activity data, however, have shown conditions to be weaker than they had anticipated and indicate that "there remains significant capacity in the New Zealand economy".

Reflecting this assessment, officials decided that that it was appropriate to cut policy rates again today. Although they also considered a 25 basis point reduction, they concluded a bigger reduction would mitigate downside risks to the growth outlook. They also advised that if medium-term inflation pressures ease as they anticipate, they remain ‘open" to cut the cash rate further in coming meetings.

Employment

Demand

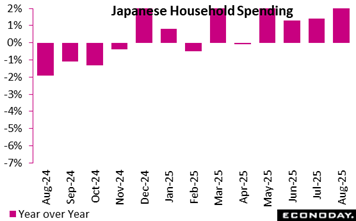

Japan’s real household spending rose 2.3 percent in August from a year ago, well above the expected 1.0 percent increase, and topping the highest forecast of up 1.7 percent. This is the fourth consecutive annual increase. Real household spending was up 1.4 percent in July.

Other key points in the report:

JAPAN AUG REAL HOUSEHOLD SPENDING S/A +0.6% M/M (JULY +1.7%), 2ND STRAIGHT RISE; MEDIAN FORECAST -0.3% (RANGE: -1.4% TO +0.5%)

JAPAN AUG REAL CORE HOUSEHOLD SPENDING (EX-HOUSING, VEHICLES, GIFT MONEY) +3.0% Y/Y VS. +0.2% IN JULY WHEN OVERALL SPENDING ROSE 1.4%

JAPAN AUG HOUSEHOLD SPENDING Y/Y RISE LED BY AUTO PURCHASES, OVERSEAS/DOMESTIC PACKAGE TOURS, DONATION; DROP IN GIFT MONEY, RICE, OTHER REMITTANCES WEIGH

Production

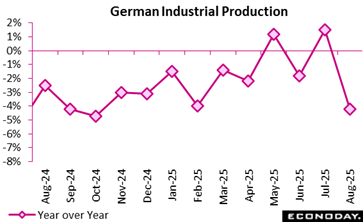

Germany’s industrial output experienced a notable downturn in August 2025, signalling a slowdown after earlier gains in July. Production fell by 4.3 percent from the previous month and 3.9 percent year-over-year after seasonal and calendar adjustments. This reversal contrasts with July’s modest growth of 1.3 percent, reflecting sectoral disruptions rather than a systemic decline.

The automotive industry, Germany’s largest manufacturing sector, was the key driver of the downturn, posting an 18.5 percent monthly drop attributed to factory holidays and production realignments. The mechanical engineering sector also fell by 6.2 percent, while the pharmaceutical and electronics industries recorded respective contractions of 10.3 percent and 6.1 percent. Collectively, these declines contributed to a 5.6 percent overall fall in industrial production excluding energy and construction.

While capital and consumer goods output declined sharply (minus 9.6 percent and minus 4.7 percent, respectively), energy-intensive industries showed slight resilience, rising 0.2 percent compared with July. However, in the broader three-month view, output in these energy-intensive sectors remained 2.7 percent lower than in the preceding period.

In summary, the August updates highlight a manufacturing sector undergoing adjustment pressures amid seasonal shutdowns and structural changes, rather than sustained weakness in industrial fundamentals.