Last Week: Key Global Events

Edited by Simisola Fagbola, Econoday Economist

The Economy

GDP

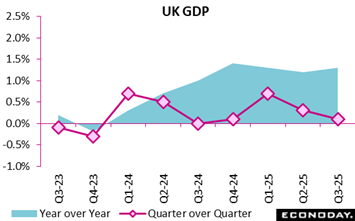

The UK economy continued to expand in the third quarter of 2025, but the pace of growth slowed. Real GDP rose by 0.1 percent, a modest increase compared with the 0.3 percent recorded in the second quarter. However, the annual picture appears more positive, with GDP 1.3 percent higher than the same quarter in 2024, suggesting a gradual recovery over the longer term.

Sectoral performance shows an uneven pattern. Services grew by 0.2 percent and construction by 0.1 percent, providing the main support for quarterly growth. In contrast, the production sector contracted by 0.5 percent, signalling persistent challenges in manufacturing and energy-related activities. Despite overall economic expansion, real GDP per head did not grow, which implies that the benefits of economic improvement are not being felt evenly across the population.

Recent revisions to earlier data, including updates linked to UK trade and the improved measurement of precious metals, did not alter the headline GDP figures. However, small adjustments to the GDP deflator and current price estimates indicate refinement rather than structural change.

Overall, the third quarter reflects a cautiously improving economy, but one marked by uneven sectoral performance and limited gains in living standards.

The euro area economy showed modest but continued improvement in the third quarter of 2025. Quarter-on-quarter GDP growth rose to 0.2 percent, up from 0.1 percent in the previous quarter. This steady pace suggests that the region is gradually strengthening despite ongoing uncertainties in global markets.

Looking at annual performance, GDP expanded by 1.4 percent compared with the same quarter in 2024. Although this is slightly below the 1.5 percent recorded in the second quarter, it still reflects a stable recovery pattern. The slight moderation hints at softer domestic demand, yet the overall picture remains broadly positive.

Within the region’s quarterly growth, France recorded a stronger rebound, rising by 0.5 percent after a contraction of 0.3 percent. Spain also increased by 0.6 percent, though this was slightly below its previous growth of 0.8 percent. Germany showed no growth, holding at 0.0 percent after a decline of 0.2 percent, and Italy similarly posted 0.0 percent following a small fall of 0.1 percent.

Together, the quarterly and annual trends suggest an economy moving forward at a cautious but consistent pace. The incremental rise in growth signals resilience across the euro area, supported by improving external conditions and moderate internal activity. While the momentum is not rapid, it reflects a balanced recovery rather than a volatile one.

Employment

The UK labour market showed signs of softening in late 2025, with employment levels slipping and wage growth moderating. Estimates indicated that the number of payrolled employees declined by 117,000 (0.4 percent) over the year to September 2025 and by 32,000 (0.1 percent) between August and September, signalling a cooling demand for labour. The early figure for October 2025 pointed to a sharper annual drop of 180,000 (0.6 percent).

The employment rate fell slightly to 75.0 percent in July-September 2025, while unemployment edged up to 5.0 percent, reflecting mild slackening in the job market. Economic inactivity stood at 21.0 percent, unchanged, while the claimant count increased on the month to 1.696 million people. Vacancies remained broadly stable at 723,000, suggesting employers are cautious but not retrenching sharply.

Wage growth persisted, with total pay up 4.8 percent and regular pay 4.6 percent, translating to modest real pay increases of 0.5-1.0 percent after inflation adjustment. Public sector pay growth outpaced the private sector due to earlier settlements.

Overall, the data portray a labour market that is cooling yet resilient as employment is easing. Still, earnings are holding up, offering a mixed outlook for household incomes and inflationary pressures as we head into 2026.

Production

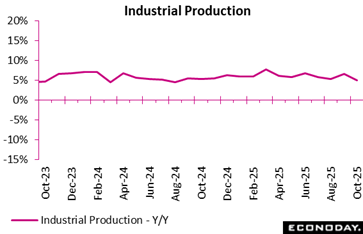

Chinese industrial production rose 4.9 percent on the year in October slowing from growth of 6.5 percent in September and falling short of the consensus forecast of 5.5 percent. In month-over-month terms, industrial production rose 0.17 percent in October after an increase of 0.64 percent in September.

Within the industrial sector, manufacturing output rose 4.9 percent on the year in October, also slowing from an increase of 6.8 percent in September. Utilities output and mining output rose 5.4 percent and 4.5 percent on the year respectively, after previous increases of 2.0 percent and 5.8 percent respectively.

In their statement accompanying today’s data, officials characterised the data as showing the economy "maintained a generally stable momentum of progress". Although officials again refrained from explicitly referring to trade tensions with the United States, they noted that "there are many unstable and uncertain factors in external environment". Officals provided no specific guidance about whether changes to policy settings will be considered in the near-term.

Business Surveys

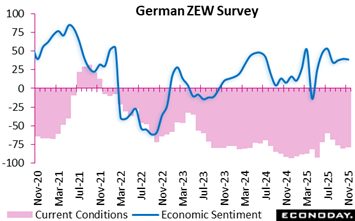

The German economic sentiment indicator slipped marginally to 38.5 points, showing that optimism persists but has plateaued. Meanwhile, the current situation score of minus 78.7 points reveals that the economy remains deeply strained despite a slight uptick. Confidence in the government’s ability to address persistent structural challenges is waning, even as new investment programmes aim to boost growth.

Sectoral trends highlight a mixed recovery, as the chemical and metal industries face worsening prospects, while banking and insurance continue to show further decline. Encouragingly, private consumption surged by 13.3 points, signalling a revival in domestic demand supported by stronger performance in IT, telecommunications, and services.

The eurozone follows a similar pattern of cautious optimism, with expectations rising to 25.0 points and current conditions improving modestly to minus 27.3 points. In summary, the latest updates suggest that while consumer activity is injecting short-term momentum, Germany’s industrial weaknesses and policy uncertainty continue to weigh on sustained recovery.

US Review

Small Business Sentiment Stable but Uncertainty Rises

By Theresa Sheehan, Econoday Economist

The past week was largely devoid of significant economic data for the US as the government shutdown dragged to its official end on Wednesday when President Trump signed the funding bill.

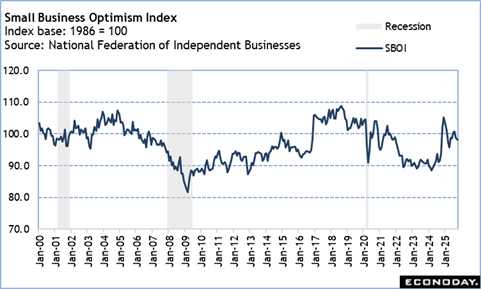

The lack of data in the week throws the spotlight on the October NFIB small business optimism index. The index was little changed at 98.2 compared to 98.8 in September. It hovered above the 52-year average of 98 for a second month in a row. The index reflects only slightly positive conditions as small businesses navigate the evolving economic environment with more changes to trade and tariff policies, a government shutdown, and a labor market in which they are disadvantaged.

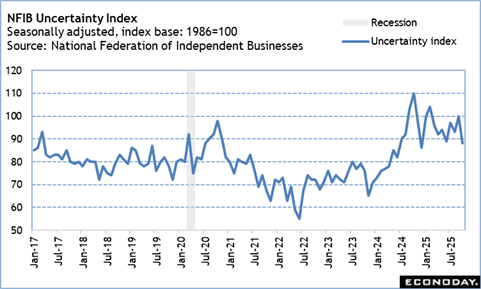

However, the NFIB uncertainty index fell 12 points to 88 in October from September. Uncertainty remains elevated but closer to levels in more normal economic conditions.