Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

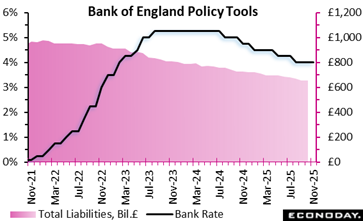

The Bank of England’s Monetary Policy Committee held Bank Rate at 4 percent in November 2025, reflecting a finely balanced policy environment. The narrow 5-4 vote highlights growing divisions over how quickly to unwind monetary tightening. While CPI inflation is judged to have peaked and underlying pressures are easing, supported by slower wage growth, cooling services prices and a softening labour market, significant uncertainty persists. One camp remains wary of entrenched inflation expectations and structural shifts in wage-setting that could slow progress. The opposing view emphasises weak household demand, rising slack and the risk of overshooting below the 2 percent target if policy remains too restrictive.

Past rate increases are now weighing noticeably on activity, with sluggish consumption and employment signaling emerging spare capacity. Although disinflation is progressing, the MPC emphasised the need for further evidence before considering another rate cut. As the Bank Rate approaches its neutral level, judging monetary restrictiveness becomes increasingly tricky.

Looking ahead, interest rates are expected to fall gradually if inflation continues to ease. However, the path remains data dependent. The November decision captures a central theme of 2025 monetary strategy by balancing the threat of persistent inflation against the growing risk of demand-driven weakness.

Demand

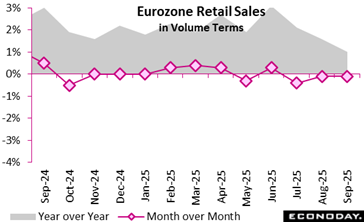

Retail activity in the euro area showed signs of stagnation in September 2025, with retail trade volume edging down by 0.1 percent month-over-month for a second consecutive month. The decline reflects weak short-term consumer momentum, driven primarily by reduced spending on non-food items and a sharper fall in demand for automotive fuel, which dropped by 1.0 percent. Meanwhile, spending on food, drinks and tobacco remained stable, suggesting that households are prioritising essential goods amid ongoing economic uncertainty.

On an annual basis, however, retail performance appears more resilient. Compared with September 2024, overall sales rose by 1.0 percent, supported by stronger demand for non-food products, which increased by 1.4 percent. This indicates consumers are cautiously returning to discretionary spending categories over the longer horizon. By contrast, fuel sales across specialised outlets continued to decline year-over-year, reflecting potential behavioural shifts, higher fuel prices or increased transport efficiency.

In essence, the latest updates highlight a mixed retail landscape, characterised by a slight downward monthly momentum and modest annual growth. While essential categories underpin stability, persistent weakness in fuel-related spending and pressure on non-food segments point to ongoing consumer sensitivity to economic conditions.

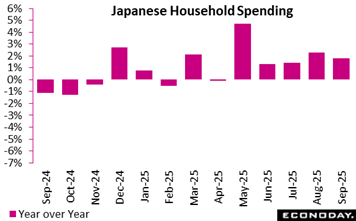

Japanese real household spending rose by 1.8 percent in September from a year ago, missing expectations that centered on a 2.6 percent increase. The September increase was the fifth straight month of year-on-year gains and followed a 2.3 percent rise on year in August.

Real household spending slipped by 0.7 percent on the month in September from August, seasonally adjusted, after rising 0.6 percent on the month in August. The September monthly decline was the first in three months, and the decrease exceeded the 0.5 percent decline anticipated in the survey of forecasts.

Production

German manufacturing activity in September 2025 presents a mixed picture, with short-term improvement offset by ongoing structural weaknesses. New orders rose by 1.1 percent compared with August, helped mainly by strong demand in the automotive sector (3.2 percent), electrical equipment (9.5 percent), and other transport equipment (7.5 percent). This signals continued appetite for technologically intensive and export-oriented goods. However, the fall in fabricated metal products (minus 19.0 percent) and basic metals (minus 5.6 percent) highlights persistent fragility in upstream industrial supply chains and volatility linked to large one-off orders.

Consumer goods orders performed strongly (6.2 percent), potentially reflecting easing inflation and recovering household confidence, while capital goods stagnated, hinting at cautious investment sentiment. Foreign demand offered necessary support, rising 3.5 percent, especially from outside the euro area. Domestic orders, however, contracted by 2.5 percent, revealing weaker internal economic momentum.

Despite rising orders, manufacturing turnover fell by 2.1 percent on the month, indicating delays between ordering and revenue realisation, and possibly pricing pressures. In essence, manufacturing shows selective resilience, but underlying demand remains uneven and sensitive to sector-specific fluctuations.

Business Surveys

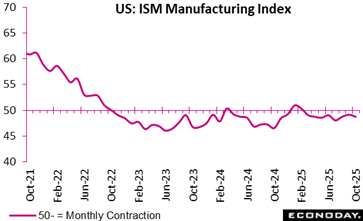

US ISM manufacturing index misses expectations at 48.7 in October versus the 49.5 figure expected and 49.1 in September. Tariff uncertainty continues to weigh on the sector and hiring and capex remain effectively frozen as manufacturing decision-makers hope for clarity, ISM says.

The dip in the manufacturing index in the latest month reflect declines in production and inventories.

All four demand indicators (New Orders, New Export Orders, Backlog of Orders, and Customers’ Inventories indexes) improve although they remain in contraction. The Customers’ Inventories Index contracts at a slower rate.

On the output side, production deteriorated and employment contracted at a slower pace as 67 percent of panelists say managing head count remains in effect at their companies, as opposed to hiring.

Inputs (defined as supplier deliveries, inventories, prices and imports), are mixed, with the Supplier Deliveries Index indicating slower deliveries, the Inventories Index contracting at a faster rate, and the Prices Index continuing to indicate pricing increases, but at a slower rate. The Imports Index contracts again but at a slower pace.

An ISM official tells reporters the US-China deal looks like a good start toward reducing the uncertainty level facing manufacturing but firms worry it will be reversed and need to see it implemented. They also need to see things settle down generally on the trade front before hiring can recover, and certainly before any of the hoped-for reshoring of manufacturing can occur.

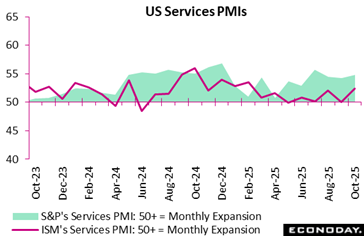

The ISM services index topped expectations at 52.4 in October, up from 50.0 in September, and well above the 51.0 figure anticipated in the Econoday consensus.

New orders notably lifted to 56.2 in October from 50.4, and business activity/production rose to 54.3 from 49.9. Employment remained in contraction at 48.2 from 47.2, and order backlog dropped to 40.8 from 47.3. Prices paid worsened to 70.0 from 69.4 as tariffs continued to boost input prices.

ISM described the latest report as a continuation of a downward trend of more than 10 percentage points in the 12-month average since February 2022, when it was 62.6. Despite the uptick for the main ISM index in the latest month, the 12-month average is the lowest since 51.7 in August 2024 and the second lowest since 51.4 in June 2010.

The S&P Global US Composite Purchasing Managers’ Index final reading came in at 54.6 in October compared to 53.9 in September, and 54.6 in August, signaling a pick up in business activity growth at the second fastest pace so far in 2025 – although employment saw only a “modest” uptick and sentiment regarding future conditions fell to a six-month low.

The US Services PMI Business Activity Index recorded 54.8 in October, up from 54.2 in September, but below expectations of 55.2 in the Econoday survey of forecasters.

“Prices data showed the slowest increases in costs and selling prices since April,” the report said.

“[I]nput costs rose to the slowest degree in six months, which helped to explain a similar slowdown in the rate of selling price inflation (also the weakest since April),” it added. “Panelists reported that competitive pressures had limited the degree to which higher costs could be passed onto clients.”

Tariffs also continue to fuel higher input costs compared to September.

On the employment front, job growth was modest as employers chose not to replace job leavers. “This partly stemmed from cost considerations, with service providers noting that labor related expenses had been a source of increased overall operating expenses during October,” S&P said.

US Review

Markets Make Do with Private Employment Data

By Theresa Sheehan, Econoday Economist

The monthly employment data is now missing for September and October as the government shutdown continues. How much longer the shutdown will drag on is anyone’s guess. It now passes the record 35 days of the prior shutdown of December 22, 2018-January 25, 2019 which occurred in the last Trump administration.

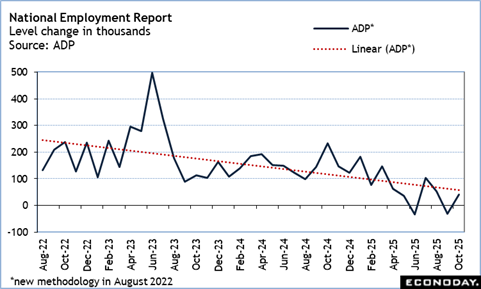

Markets and policymakers are having to make do with what private sources can say about conditions in the labor market. The ADP national employment report for October presented a picture of uneven hiring while the Challenger report on announced job cut intentions suggested broad-based plans to eliminate jobs – out of caution or hard necessity.

The ADP increase in private payrolls was 42,000 in October. On the surface the number looks decent. However, hiring was mainly in a few narrow sectors and looks to be one-offs. The rise of 25,000 in education and health services is probably mostly in healthcare workers where the loss of immigrant labor has been substantial. The 47,000 increase in trade, transportation, and utilities is probably related to hiring of seasonal workers for the winter holidays. Many of these jobs are temporary and many are on the lower end of pay scales.

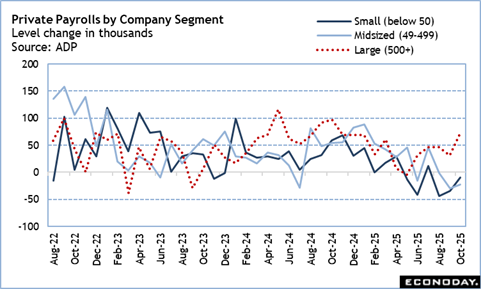

What is also important to note is that hiring is skewed to larger firms that have more resources to attract and retain workers with the right skills and experience. Larger establishments (500+ employees) added 74,000 workers to payrolls while small company payrolls (1-49 employees) saw a reduction of 10,000 and mid-sized firms (50-499) had 22,000 fewer workers on payroll.

The outlook for the labor market is less positive at the start of the fourth quarter. If hiring continues, albeit unevenly and modestly, the prospect of job losses is more elevated.

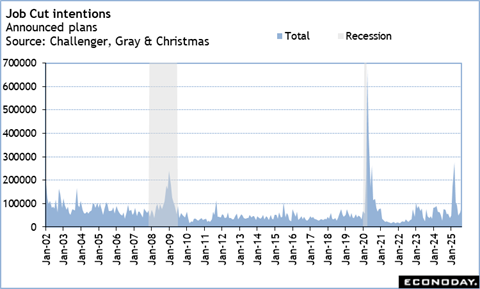

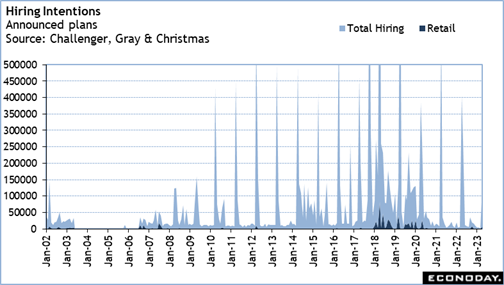

The Challenger report on announced job cut intentions showed an increase of 183.1 percent in October to 153,074 after 54,064 in in September and a rise of 175.3 percent compared to 55,507 in October 2034. For 2025 to-date, there are 1,099,500 job cuts announced compared to 664,839 in the same period of 2024. October year-to-date is the highest since 2,162,904 in the first 10 months of 2020 and 1,032,033 in the comparable period of 2009. This is consistent with an economy facing recession or responding to an economic crisis. The story for the past two years is restructuring in the technology sector, first pulling back on some of the COVID pandemic hires and second from adoption of artificial intelligence (AI) business tools. The DOGE cuts earlier in 2025 which totaled 307,638 so far, but this is essentially done. Ongoing is the changing landscape in the tech sector which has the second largest total job cut announcements for the first 10 months of 2025 at 141,159.

Job cut announcements were broad-based in October with only one industry (legal) not reporting planned cuts. If the two largest of warehousing (47,878, or 31.3 percent of the total) and technology (33,281, or 21.7 percent) accounted for over half of all announcements, that still leave a substantial 71,915 announcements.

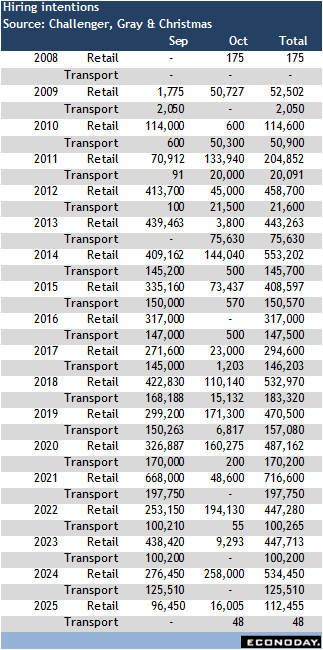

The 283,138 hiring plans in the Challenger report can be dismissed. The increase is mostly due to a single sector where technology announced 250,466 plans. Of the remaining 32,672, 16,005 are in retail and likely the tail end of seasonal hiring plans.

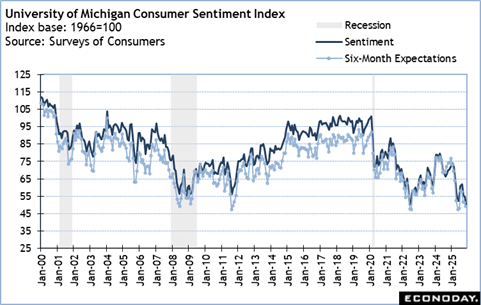

The University of Michigan consumer sentiment index was down to 50.3 in preliminary November reading. This is the lowest since 50.0 in June 2022. The government shutdown and its consequences are weighing heavily on consumers. The outlook for consumer spending over the holiday period is going to be cautious, at best. The six-month index is in recession territory at 49.0 in October.