UK Labour Report Shows Employer Caution; US Beige Book Depicts Slowing Economy

Edited by Simisola Fagbola, Econoday Economist

The Economy

Employment

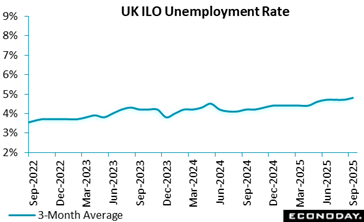

The latest UK labour market report shows that payrolled employees fell by 93,000 over the year to August 2025, with only a modest monthly rise of 10,000, reflecting subdued hiring momentum. The early estimate for September 2025 showed a further 100,000 fall in employment, suggesting ongoing labour market softening. Employment between June and August stood at 75.1 percent, slightly down from the figure recorded between March and May, while unemployment rose to 4.8 percent, indicating that some job losses have yet to be absorbed. Economic inactivity remained steady at 21.0 percent, suggesting limited re-engagement of those outside the workforce.

Vacancies declined for the 39th consecutive period, signalling persistent employer caution across industries. Despite weakening job creation, wage growth remained relatively strong at 4.7 percent for regular pay and 5.0 percent including bonuses, with higher increases in the public sector. Adjusted for inflation, real wage growth was modest at 0.6 percent (including owner occupiers’ housing costs) and 0.9 percent (excluding owner occupiers’ housing costs) for regular pay, reflecting limited purchasing power improvement.

The Claimant Count rose slightly to 1.692 million, and 15,000 working days were lost to industrial disputes, highlighting ongoing worker unrest. In essence, these updates suggest a cooling labour market with cautious optimism supported by moderate pay growth but continued structural fragility.

Production

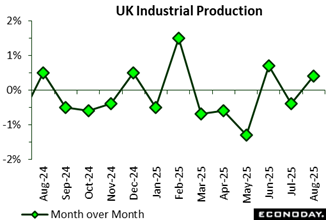

The UK’s industrial production data for August 2025 reflects a modest rebound in output, offering a brief respite from July’s contraction. Overall production rose by 0.4 percent, reversing the previous month’s decline and signalling some resilience within the industrial sector. The recovery was primarily driven by gains in manufacturing (0.7 percent), supported by upticks in electricity and gas (0.4 percent) and water supply and sewerage (0.3 percent), while a 2.3 percent fall in mining and quarrying offset part of the progress.

Encouragingly, eight of the thirteen manufacturing subsectors recorded growth, with basic pharmaceutical products (3.0 percent) making the most significant contribution, a reflection of continued global demand for healthcare-related goods. However, on a yearly basis, industrial production still declined 0.7 percent, with manufacturing output down 0.8 percent, highlighting persistent challenges in sustaining momentum.

The latest updates suggest that while short-term output is stabilising, structural issues, particularly in energy-intensive and extractive industries, continue to weigh on industrial performance. Hence, although August’s figures provide a glimmer of optimism, the broader trajectory indicates that UK industry remains vulnerable to both domestic cost pressures and external market uncertainties.

Industrial production on a monthly basis, fell by 1.2 percent after a modest 0.5 percent increase in July, reflecting a temporary loss of momentum in the manufacturing sector. The decline was largely driven by weaker activity in capital goods (minus 2.2 percent) and durable consumer goods (minus 1.6 percent), suggesting reduced investment demand and cautious consumer spending. Energy production also dipped (minus 0.6 percent), reflecting continued pressure on the energy market, while non-durable consumer goods posted a slight rise (0.1 percent), possibly supported by household essentials.

However, compared with August 2024, industrial production rose by 1.1 percent, signalling a degree of recovery over the year. This improvement was mainly sustained by strong growth in non-durable consumer goods (8.2 percent), which helped offset declines in all other categories, including durable consumer goods (minus 2.6 percent) and intermediate goods (minus 1.7 percent).

The annual data suggest that while consumer-oriented industries remain resilient, investment-related sectors are still struggling to regain consistent growth. In summary, the figures point to uneven industrial recovery across the euro area, shaped by fluctuating demand, energy adjustments, and broader economic uncertainties affecting production dynamics.

Labour market conditions in Australia were mixed in September, with full-time employment rebounding after a previous decline but the unemployment rate increasing. Reserve Bank of Australia officials noted that labour market conditions "was still a little tight" at their most recent meeting, but the increase in the unemployment rate reported today may strengthen the case for another rate cut at their next meeting in November.

The number of people employed in Australia rose by 14,9000 persons in September after falling by 5,400 persons in August, well below the consensus forecast for an increase of 20,000. Full-time employment rose by 8,700 persons after falling by 40,900 persons previously, continuing the oscillation between increase and decreases in recent months. Part-time employment, increased by 6,300 persons after a previous increase of 35,500 persons. Hours worked rose 0.5 percent on the month after advancing 0.1 percent previously.

Today’s data also show the unemployment rate rose from 4.3 percent in August to 4.5 percent in September, its highest level since late 2021. The participation rate rose slightly from 66.9 percent to 67.0 percent.

International trade

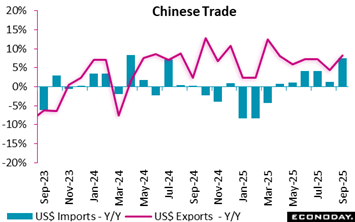

China’s merchandise trade surplus in US dollar terms was $90.45 billion in September, narrowing from $102.33 billion in August but well above the level of $81.7 billion recorded in September 2024. Exports rose 8.3 percent on the year in September after increasing 4.4 percent in August, while imports rose 7.4 percent, picking up from a previous increase of 1.3 percent.

Today’s data showed further weakness in Chinese exports to the United States, down 27 percent on the year, but this was again outweighed by stronger shipments to other trading partners. Strong growth in exports to other markets likely reflects re-routing of trade flows in an attempt to circumvent the impact of US tariffs on China.

Business Surveys

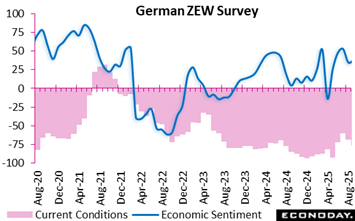

Germany’s economic outlook showed modest improvement in October 2025, with expectations rising 2.0 points to 39.3, suggesting cautious optimism among financial experts. However, this optimism contrasts sharply with the deeply negative assessment of current conditions, which fell further to minus 80.0 points, reflecting the ongoing strain from weak domestic demand and global economic uncertainty.

The latest update signal hopes for a medium-term recovery, even as confidence remains tempered by concerns over the government’s investment programme and volatile global markets. Encouragingly, export-oriented industries, notably metal production, pharmaceuticals, mechanical engineering, and electrical equipment manufacturing, show signs of renewed momentum following a recent slump in exports to China. The automotive sector, however, continues to struggle, reflecting broader structural challenges and softening global demand.

Across the eurozone, sentiment dipped modestly, with expectations falling 3.4 points to 22.7 amid fiscal uncertainty in France, and the current situation index weakening to minus 31.8. Overall, the report depicts improving expectations driven by export resilience and innovation, yet weighed down by persistent structural weaknesses and fragile consumer confidence.

US Review

Beige Book Shows Economy Softens

By Theresa Sheehan, Econoday Economist

The shutdown of the US federal government drags on. The delays in releasing economic data are accumulating and ripple effects are spreading. Some reports from outside the statistical agencies are beginning to be affected. For example, the Federal Reserve had to postpone the release of the September industrial production report (originally scheduled for October 17) and the Chicago Fed has put on hold releasing the national activity index numbers (originally scheduled for October 23). Some private data reports will be using proxies for the government numbers, but that will result in less reliable data and eventual revisions.

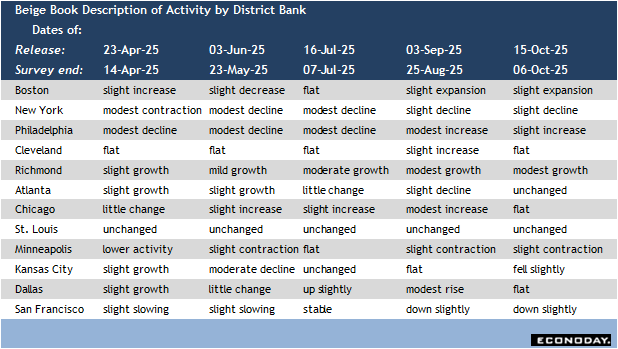

This week the most important release was the Fed’s Beige Book compiled in advance of the October 28-29 FOMC meeting. The anecdotal evidence about economic conditions across the 12 districts will be more important than usual since the FOMC will have fewer hard numbers to guide setting monetary policy. In a speech on Tuesday, Fed Chair Jerome Powell warned against placing too much reliance on the quarterly summary of economic projections released in September. With the shutdown lengthening and new tariffs announcements out of the White House, economic uncertainty has grown. Powell stressed that monetary policy is not on a “predetermined path” and that the FOMC will have no “risk-free” choices between gauging the health of the labor market and the duration and size of the recent inflation pressures.

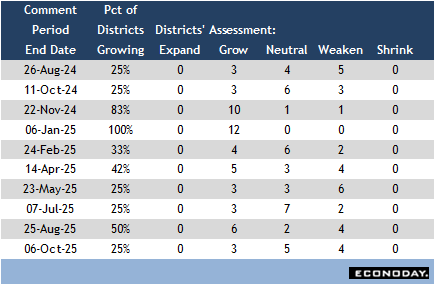

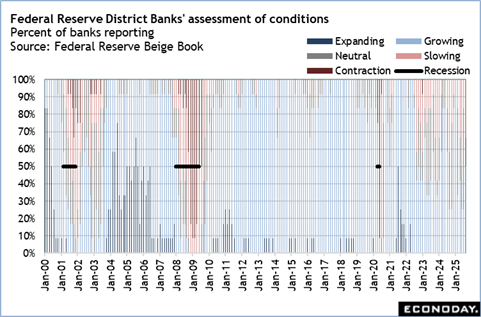

The Beige Book covered roughly the period between late August and early October. Overall, the report reflected softer activity since the prior report with only 3 districts reporting growth, 5 neither growing or contracting, and four slightly weaker. At this point it would not take much to tip the US economy into recession despite the resilience demonstrated by the rebound to 3.8 percent GDP growth in the second quarter. The GDP Nowcasts from three district banks are mixed, with two out of the three showing lower growth in the third quarter and one – the Atlanta Fed which has the best correlation with the advance estimate – growth continuing at 3.8 percent. However, the real challenge will be the fourth quarter and if consumers spending pulls back during the holiday season and businesses turn more cautious in uncertain times.