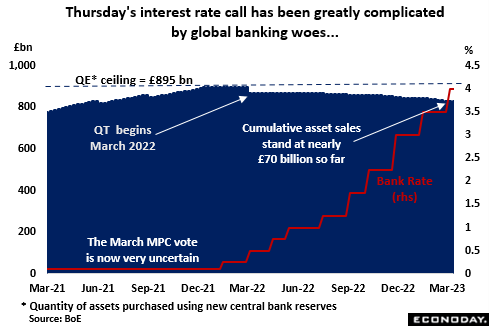

The March BoE MPC meeting had been widely expected to deliver an eleventh successive increase in Bank Rate with the majority of forecasters looking for a 25 basis point hike in the benchmark rate to 4.25 percent. This would have boosted the cumulative tightening in the current cycle to some 415 basis points. However, the ongoing turmoil in the global banking sector has made Thursday’s call much more uncertain. The MPC’s two main doves (Swati Dhingra and Silvana Tenreyro) were already essentially guaranteed to repeat their February call for no change and might now even favour a rate cut while some other members, who would previously have wanted the 25 basis point move, could switch their vote in preference of stability. On balance, an increase in Bank Rate to 4.25 percent would still just about seem to be the market consensus call but, in the current environment, this is a moving target and Thursday is a long way away.

By contrast, QT has continued to run quite smoothly in the background and would seem to be on course to achieve its goal of reducing the bank’s gilt holdings in its Asset Purchase Facility (APF) by £80 billion to £758 billion by November. As of the start of this month, bond holdings stood at £821.2 billion. With outright sales having begun on 28 September, the stock of corporate bonds has also been reduced from just over £20 billion to £8.92 billion. These disposals will continue with a view to winding up the programme by around the end of the year.

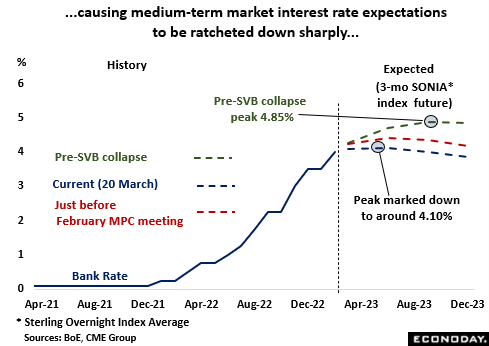

Shortly before the collapse of Silicon Valley Bank (SVB) and subsequent run on Credit Suisse, financial markets saw 3-month money rates topping out this year around 4.85 percent in September. This was up sharply from the 4.4 percent peak priced in for June just before the February MPC meeting when Bank Rate stood at 3.5 percent. By year-end, borrowing costs were expected to be almost 70 basis points above what was previously thought likely. However, the mayhem in the banking sector has prompted a major reassessment and rates are now seen peaking at just 4.15 percent by the middle of 2023. Moreover, policy is expected to be eased over the latter half of the year leaving rates at just 3.85 percent in December.

In fact, worries about the banking fallout have had a significant impact on the entire yield curve. Compared with just before the troubles began, 5-year yields are down about 50 basis points, 10-year yields 45 basis points and 20-year yields 35 basis points. On paper, contagion risks were thought likely to be relatively limited as domestic banks’ holding of gilts have not been subject to the sort of aggressive monetary tightening from the BoE that U.S. Treasuries have faced from the Federal Reserve. In addition, the bank moved quickly to facilitate a private sale of the UK arm of SVB to HSBC, a move which protects deposits without requiring the support of the taxpayer. Even so, with UK banking stocks having slid around 15 percent since the start of the crisis and, at the time of writing, still falling, the current flight to safety may take some stopping and the MPC will not want to add fuel to the fire.

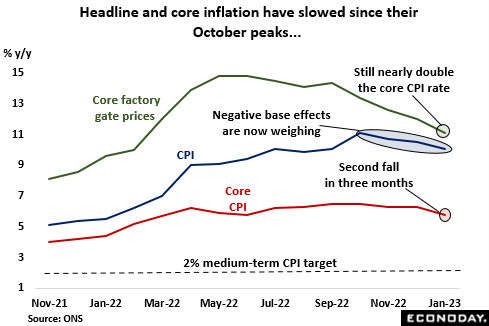

Meantime, headline inflation has fallen further since the last MPC meeting, sliding to 10.1 percent in January and matching a 5-month low. The February data, due for release just a day ahead of this week’s policy announcement, are also expected to extend the downtrend. Negative base effects stemming from last year’s surge in energy prices have helped but importantly too, there has been some better news on underlying prices. At 5.8 percent in January, the core rate was down 0.7 percentage points from last October’s peak and equalled a 10-month trough. In addition, the BoE’s latest quarterly survey of household inflation expectations found the 1-year ahead view cut from 4.8 percent in November to 3.9 percent and the 5-year ahead call reduced from 3.3 percent to 3.0 percent. Even so, while moving in the right direction, both actual and expected measures remain well above the 2 percent CPI target which does nothing to bolster policy credibility.

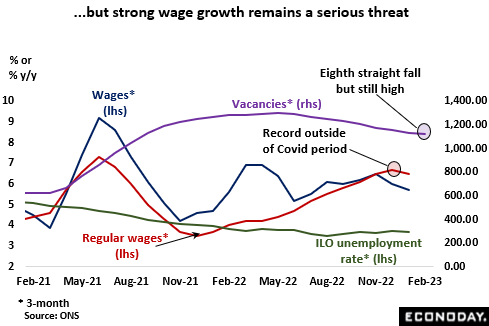

Moreover, wages remain a serious threat to any sustainable reduction in inflation. Average earnings growth has eased in recent months but, with an annual increase of 5.7 percent in the three months to January, it was still too high to be consistent with meeting the inflation target. Making matters worse, regular earnings remain notably stronger and at 6.5 percent over the same period, were only a couple of ticks below their fourth quarter mark, itself a record outside of the distorted pandemic period. Indeed, the BoE’s Chief Economist has acknowledged that wages have proved stickier than the bank expected in its February Monetary Policy Report (MPR) forecasts. Pay rates continue to be supported by a labour market that, despite loosening somewhat, remains historically very tight. With skills shortages still a major issue, even businesses anticipating slower sales are reluctant to shed staff. Vacancies have fallen quite significantly since the middle of last year but from all-time highs and are still well above normal levels.

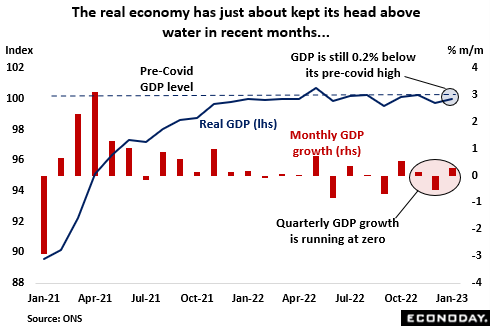

As it is, the economy has recently proved surprisingly resilient. Fourth quarter GDP did not contract as widely forecast and total output rose a respectable 0.3 percent in January. Retail sales volumes expanded in the same month for only the second time since August 2021 and, albeit from a very weak January level, consumer confidence in February posted its largest gain in nearly two years. February’s PMI composite output index (53.1) was also above 50 for the first time in seven months and on some measures, even the housing market has shown some tentative signs of a pick-up. That said, the squeeze on real earnings (down a yearly 3.2 percent in January) continues and with quarterly economic growth only running at zero, the economy at the start of the year was still 0.2 percent smaller than it was just before the arrival of the pandemic. The big picture remains soft and although last week’s Budget was, if anything, a little looser than anticipated, it still implies sizeable net tax rises if the government is to get the grip it seeks on public sector finances.

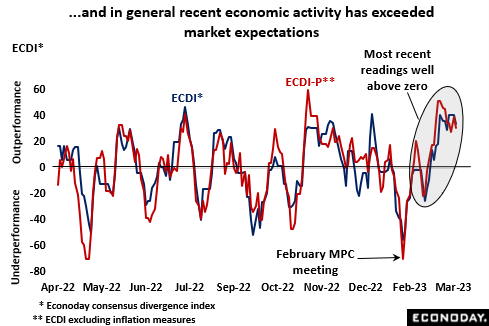

In fact, having undershot market expectations by a sizeable amount in the run-up to the February MPC meeting, in general the more recent data have proved surprisingly strong. Both the UK’s ECDI and ECDI-P have been consistently above zero since late last month and may mean that first quarter growth will carry a positive handle. In any event, the latest readings suggest that the risk of excessive monetary tightening is not as high as the doves might make out.

Against this backdrop, the MPC will have to weigh extremely carefully a number of conflicting factors for policy. Another split vote looks very probable and it could be a good deal closer than the 7-2 seen in February. To be sure, unless the banking sector begins to behave itself, another hike at this time could easily prove to be a tightening too far.