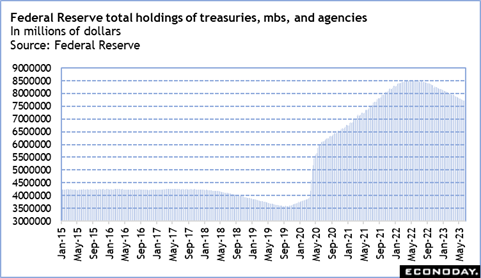

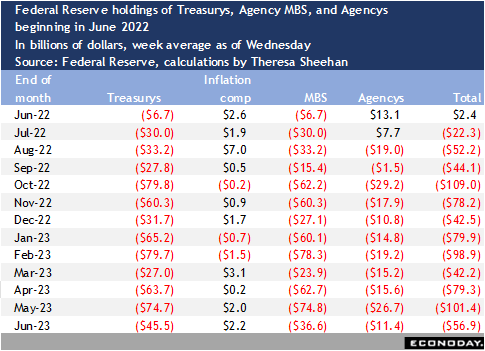

How much progress has been made in quantitative tightening since the Fed started, in June last year, to reduce its reserve holdings of US treasuries and agency mortgage-backed securities?

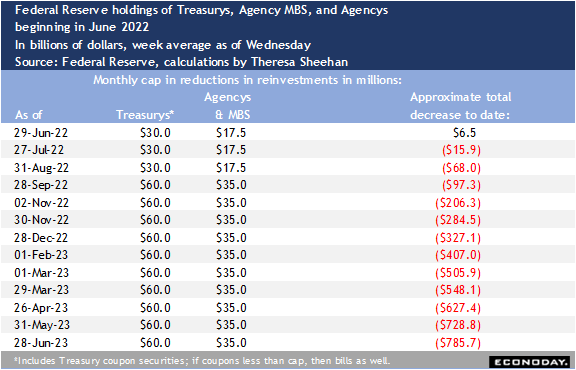

It was on May 4, 2022 that the FOMC announced its plan to reduce the size of the balance sheet. For the June-August 2022 period the program would begin with monthly caps of $30.0 billion in US treasuries and $17.5 billion in agency mortgage-backed securities, then in September rise to $60.0 billion and $35.0 billion, respectively. The FOMC has stuck to this plan since its announcement. Fed Chair Jerome Powell has repeatedly signaled that for the time being the FOMC has no intention of changing this steady, predictable path of reductions.

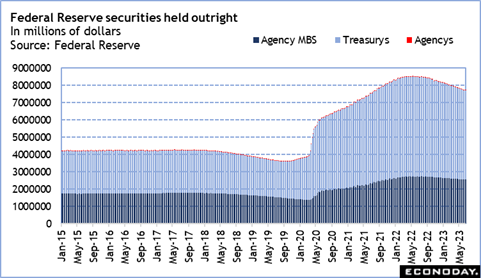

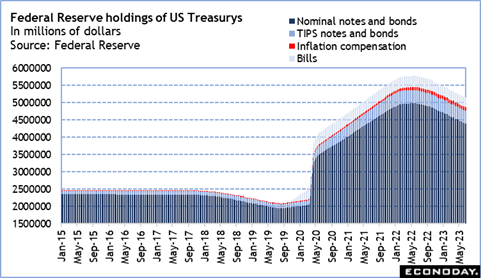

The Fed H.4.1 report on the factors affecting reserve balances is weekly and therefore doesn’t necessarily align neatly with the start and end of the month. However, it broadly paints a picture of the path of progress over time. It should be noted that the monthly caps need to be read in terms of maturing securities. While US treasuries have a fixed maturity schedule and principle payments are predictable, those for mortgage-backed securities are less predictable due to the potential for mortgages to be paid in full or refinanced to a new note.

At the start of June 2022, the Fed’s holdings of US treasuries, mortgage-backed securities, and agencies was $8.480 trillion. Routine reductions have brought the reserves down by more than $785 billion to $7.694 trillion. Compared to a year ago, this is visible progress. However, there is a long way to go before the level looks anything like the “ample reserve balance” that the FOMC settled on just prior to the pandemic. It is a not unreasonable concern that the next shock to the economy that triggers a need for rate cuts could be bad enough to take interest rates back to the effective lower bound (ELB) and bring another round of large-scale asset purchases back into play before the balance sheet has normalized.