Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

The US Consumer Price Index in April rebounded by 0.2 percent, following a 0.1 percent decline in March, and a 0.2 percent jump in February. This compares to expectations for a 0.3 percent rise in the Econoday survey of forecasters. The slowdown in the pace of consumer price continues after a steep rise in the CPI between November 2024 and January 2025.

Over the last 12 months, consumer prices are up 2.3 percent, compared to a 2.4 percent year-over-year rise in March. Expectations were for a 2.4 percent increase.

Core CPI, excluding food and energy prices, are up by 0.2 percent, after rising by just 0.1 percent in March, and +0.2 percent in February. Consumer prices less food and energy rose 2.8 percent from April 2024, the same rate of increase on an annual basis in March.

The data is likely the calm before tariff-driven storm – with expectations that the inflationary impact on consumer prices will hit from mid-2025 onwards. The Federal Reserve will be encouraged by this data, but it is unlikely to influence the central bank’s decision to remain in wait-and-see mode for the foreseeable future.

After rising by 0.2 percent in March, shelter costs rose by 0.3 percent in April (and are up 4 percent year-over-year). Food prices dipped 0.1 percent, slowing down after a 0.4 percent rise in March, as grocery prices declined by 0.4 percent last month, and restaurant prices rose by 0.4 percent.

Energy costs rose by 0.7 percent over the month, as increases in the cost of natural gas (+3.7 percent) and electricity (+0.8 percent) offset a 0.1 percent decline in gasoline prices. Energy prices saw a 2.4 percent decline in March.

Energy prices are down 3.7 percent year-over-year, following a 3.3 percent slide for the 12 months ending March. Food prices increased 2.8 percent compared to April 2024, compared to a 3 percent rise in March.

GDP

The UK economy picked up pace in the first quarter of 2025, with GDP expanding by 0.7 percent, a notable acceleration from the modest 0.1 percent growth in the previous quarter. Over the year, the UK GDP grew by 1.3 percent, a slight drop from the year-over-year growth of 1.5 percent in the fourth quarter of 2024. The latest GDP growth was driven by broad-based sectoral improvements, led by the services sector, which grew by 0.7 percent, and a robust 1.1 percent rise in production output. In contrast, the construction sector remained flat, reflecting stagnation in building activity despite broader economic gains.

From an expenditure perspective, the economy was fueled by increased household spending, higher gross fixed capital formation, and stronger net trade performance—pointing to renewed confidence among consumers and investors. Encouragingly, nominal GDP rose by 1.6 percent, buoyed by a rise in employee compensation, signaling a rebound in earnings and potential improvements in living standards.

Importantly, real GDP per head grew by 0.5 percent, marking a turnaround after two consecutive quarters of decline and suggesting that economic growth is beginning to translate into individual gains. In essence, the first quarter of 2025 offers a positive outlook, with solid foundations laid for a more sustained and inclusive recovery.

Employment

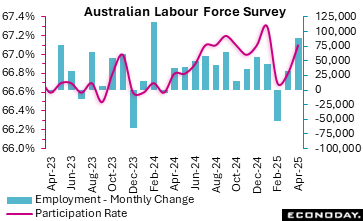

Labour market conditions in Australia remained strong in April, with employment recording a sharp increase and the unemployment and participation rates continuing to indicate very tight conditions. This will likely keep the focus of the Reserve Bank of Australia on risks to the inflation outlook ahead of its policy meeting next week and may reinforce concerns among officials about whether an immediate rate cut is warranted.

The number of people employed in Australia rose by 89,000 in April, up from an increase 32,200 in March and well above the consensus forecast for an increase of 24,000. Full-time employment rose by 59,500 persons after a previous increase 15,000 persons, while part-time employment rose by 29,500 persons after a previous increase of of 17,200 persons.

Today’s data also show the unemployment rate was steady at 4.1 percent in April. The unemployment rate has been little changed from this level for a year. The participation rate rose from 66.8 percent to 67.1 percent, close to its recent high.

Demand

The dollar value of US retail and food services sales is up 0.1 percent in April after an upward revision to up 1.7 percent in March. The April month-over-month increase matches the consensus in the Econoday survey of forecasters. Sales excluding motor vehicles are also up 0.1 percent in April after an upward revision to up 0.8 percent in March. This is below the consensus of up 0.3 percent in the Econoday survey. Sales excluding motor vehicles and gasoline are up 0.2 percent in April after rising 1.1 percent in March.

Sales of motor vehicles are down 0.1 percent in April compared to the 5.5 percent increase in March. The burst of purchases of new motor vehicles and part that was related to anticipation of higher tariffs is fading. Motor vehicles and parts account for 19.6 percent of total sales. Gasoline sales are down 0.5 percent in April after down 2.5 percent in March. Gasoline prices are falling contrary to the usual seasonal trend of higher prices in April when refineries are switching production to summer fuel formulations. Gasoline sales account for 7.0 percent of all retail sales.

The second largest share of retail sales is at nonstore retailers with 17.1 percent of the total. Sales at nonstore retailers are up 0.2 percent in April after rising 0.1 percent in March. Nonstore retailers include online shopping.

The presence of spring holidays in April did support some spending in April, mostly likely from travel. Sales at eating and drinking places is up 1.2 percent in April, although slower than the 3.0 percent increase in the prior month. Sales of building materials and garden supplies is up 0.8 percent in April after rising 2.9 percent in the prior month. This is probably from the tail end of tax refunds arriving during the milder weather when consumers are out repairing winter damage to homes and working in gardens.

The personal consumption expenditures are off to a slow start for the second quarter 2025, while the revisions could add a little to spending for the first quarter when the second estimate is released at 8:30 ET on Thursday, May 29. The data reflect annual revisions released by the Census Bureau on April 25.

Production

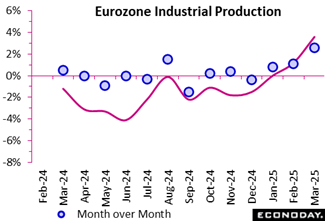

Industrial production in the euro area showed a strong rebound in March 2025, rising by 2.6 percent compared to February. This monthly momentum builds on February’s modest 1.1 percent growth, suggesting a firming recovery in the region’s industrial sector. The surge was led by capital goods (up 3.2 percent) and durable consumer goods (up 3.1 percent), pointing to increased investment and consumer confidence. Non-durable goods also saw a healthy rise of 2.3 percent, although energy production dipped slightly by 0.5 percent.

On an annual basis, euro area industrial output climbed 3.6 percent compared to March 2024, with standout performance in non-durable consumer goods, which soared by 15.7 percent, reflecting strong demand for everyday essentials. Energy production also grew by 2.2 percent, potentially driven by seasonal factors or stabilised energy markets. However, intermediate goods declined slightly by 0.2 percent, hinting at ongoing challenges in supply chains or slower upstream demand.

Regionally, industrial production rose across three of the top four-euro economies, with the largest rise experienced in Spain (1.3 percent after minus 1.8 percent), Germany (0.3 percent after minus 3.5 percent), and France (0.3 percent after minus 0.1 percent). However, Italy (minus 1.8 percent after minus 2.6 percent) continued to witness a negative industrial production growth.

Overall, the data signals growing industrial resilience across the eurozone, underpinned by rising demand and investment. Despite energy fluctuations and mild contraction in intermediate goods, March 2025 marks a turning point towards broader industrial recovery across member states.

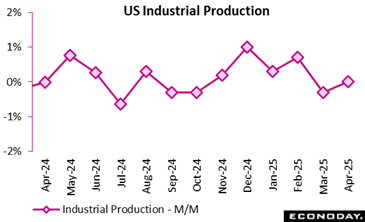

Output comes in flat for April from March, just below the expected 0.2 percent rise, as a big 3.3 percent rise in utilities offsets declines in manufacturing and mining. Manufacturing output is depressed by lower output of motor vehicles and parts, down 1.9 percent on the month.

Manufacturing is down 0.4 in April after rising by 0.4 percent in March (revised from up 0.3 percent previously). Mining is down 0.3 percent on the month.

Capacity utilization is effectively flat at 77.7 percent versus an unrevised 77.8 percent in March. This is 1.9 percentage points below the long-term average and unchanged from 77.7 percent a year ago.

Within manufacturing, output excluding motor vehicles and parts decreases 0.3 percent. Durable goods output is down 0.2 percent with motor vehicles and parts down 1.9 percent. Nondurable goods is down 0.6 percent in April, with declines in most major categories.

Sentiment

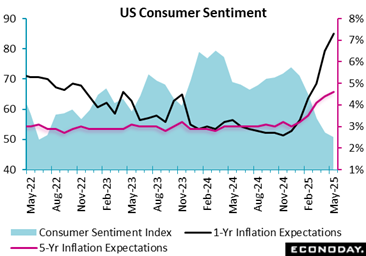

U.S. consumer sentiment continues its downward spiral – declining each month so far in 2025 – with April’s preliminary estimate coming in at 50.8 vs. April’s final reading of 52.2 and 57.0 in March, below expectations for 53.0 in the Econoday survey of forecasters.

Sentiment is now down by almost 30 percent since the start of the year. “[C]urrent assessments of personal finances sank nearly 10% on the basis of weakening incomes,” the report says. “Tariffs were spontaneously mentioned by nearly three-quarters of consumers, up from almost 60% in April; uncertainty over trade policy continues to dominate consumers’ thinking about the economy.”

The report notes that the survey collected responses before the announcement of the 90-day pause in higher reciprocal tariffs on goods from China.

Nevertheless, “[m]any survey measures showed some signs of improvement following the temporary reduction of China tariffs, but these initial upticks were too small to alter the overall picture – consumers continue to express somber views about the economy.”

The preliminary year-ahead inflation expectations surged again to 7.3 percent in May, jumping from 6.5 percent in April.

Long-run inflation expectations in May went up to 4.6 percent from 4.4 percent last month.

US Review

Tariff Effects Limited So Far

By Theresa Sheehan, Econoday Economist

Data reports for April for the consumer price index and retail sales both suggest that the impact of tariffs has been muted so far. In part, that seems to be because there was a lot of stocking up before price hikes were expected to kick in. As a result, consumer purchases are mostly of goods before tariffs pushed prices higher. Broadly speaking, prices on the shelves are not noticeably changed and the dollar value of sales isn’t larger.

The April consumer price index (CPI) for April is up 2.3 percent year-over-year and falling for the third month in a row to its slowest rise since up 1.7 percent in February 2021. On the face of it this would point to disinflation progressing toward and within reach of the Fed’s 2 percent inflation objective. However, the core CPI – excluding food and energy – shows an annual increase of 2.8 percent in April, the same as in March. Although these readings are the slowest gains since up 1.6 percent in March 2021, these also are consistent with what the FOMC calls “somewhat elevated” inflation. As such, the implication for monetary policy is no change in the fed funds target rate range of 4.25-4.50 percent at the June 17-18 meeting.

April retail sales edged up a scant 0.1 percent overall, up 0.1 percent excluding motor vehicles, and up 0.2 percent excluding motor vehicles and gasoline. The few categories that showed some gains were nearly offset by weakness elsewhere. Retail and food services in March ended on a solid increase of 1.7 percent for total sales, with respectable increases of 0.8 percent for sales excluding motor vehicles, and up 1.1 percent for sales excluding motor vehicles and gasoline. Personal consumption expenditures should see a little upward revision in the second estimate of first quarter GDP when those numbers are released at 8:30 ET on Thursday, May 29. On the other hand, early estimates for growth in the second quarter will be restrained by soft consumer spending.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.