The complexion of the September 16-17 FOMC meeting changes with two developments.

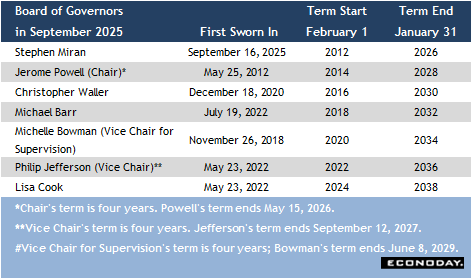

First is the unusually swift confirmation of Stephen Miran as a Fed governor and his swearing in that took place before the meeting began on Tuesday. Miran is appointed to complete the term ending January 31, 2026 that was vacated early by Adriana Kugler. It can be inferred that his time on the board will intentionally be short since his confirmation did not include a reappointment to the new term when the current one expires. This leaves President Trump with the option nominating someone else to the term beginning February 1, 2026 and running through January 31, 2040. Miran joins two other Trump appointees on the Board – Governor Christopher Waller and Vice Chair for Supervision Michelle Bowman.

Governor Lisa Cook has won her appeal to remain on the board unless and until the efforts of the Trump administration to unseat her are effective. So far legal grounds for her removal are thin and unlikely to prevail.

Fed Chair Jerome Powell faces even greater challenges to his leadership in maintaining the professionalism and independence of the central bank. Despite the statements in his confirmation hearing about the importance of an independent Fed, Miran is keeping his ties with the Trump administration. This does not presage the disinterred stance of a monetary policymaker sworn to try to achieve the dual mandate of price stability and maximum employment. However, this is conjecture and his actions will determine his legacy at the Fed.

In any case, the FOMC will have a full complement of 12 voters to set monetary policy at the end of the two days of deliberations.

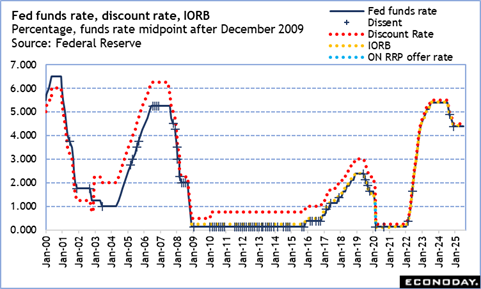

Should the majority of the FOMC voters favor a 25-basis point rate cut at this meeting as is widely expected, this raises a distinct possibility of another dissent in the vote. At the prior meeting Waller and Bowman dissented in favor of a 25-basis point cut against the majority for no change in the fed funds target rate range of 4.25-4.50 percent. It would be no surprise if Waller, Bowman, and/or Miran prefer a 50-basis point cut at this meeting. It is not out of the realm of possibility that one, two, or all three would prefer a 75-basis point cut.

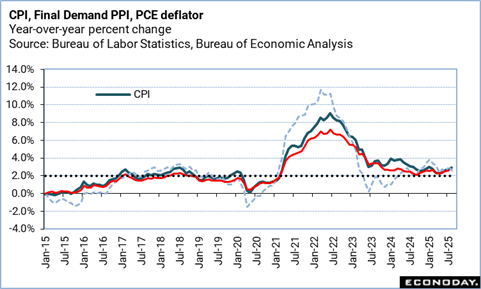

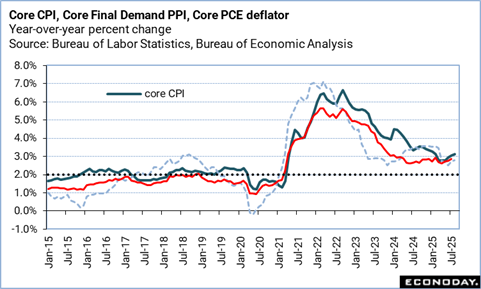

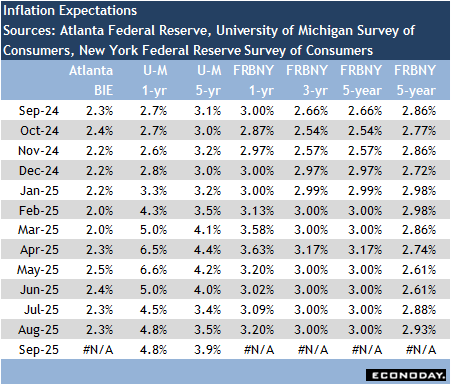

Should the FOMC majority determine a 50-basis point rate cut is appropriate, the probability of dissenting votes is much less, especially if the quarterly update to the summary of economic projections (SEP) signals an acceleration in the timeline for rate cuts. The SEP forecasts for the US economy are likely to show a downgrade in growth, higher unemployment, and less progress in disinflation toward the Fed’s 2 percent inflation target. The SEP could well reflect anticipation of cuts at the October 28-29 and December 9-10 meetings, and more into 2026.

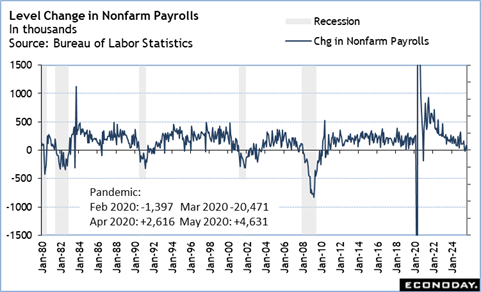

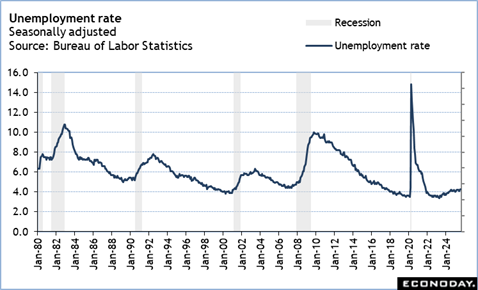

The updated SEP will be released at 14:00 ET on Wednesday along with the FOMC statement and implementation note. The statement will be a cautious one as the currently delicate balance between achieving maximum employment and price stability is starting to tip the focus more toward the weakening labor market even as inflation remains elevated and inflation expectations are reluctant to come down. Critical to the FOMC decision is how much emphasis will be placed on the drop in hiring even as unemployment has barely risen versus the recent uptick in inflation – mostly related to tariffs and possibly of short duration – and persistently higher inflation expectations for the longer term.

In his press briefing at 14:30 ET on Wednesday, Powell will likely receive many questions that he cannot or will not answer regarding the impact of political interference at the central bank and the relationships between his colleagues on the FOMC. He will, as ever, insist that the FOMC makes its decisions solely on the basis of the available information, that no decision is made before the meeting, and that monetary policy is not on a preset course. Nonetheless, he will be pressed on the FOMC consensus about the decision and what it means for the future path of interest rates.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.