Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

The Swiss National Bank decided not to push rates into negative territory following its September meeting, leaving the rate on sight deposits which banks keep at the SNB at 0.0 up to a determined threshold. The discount rate for sight deposits above the limit was held at 0.25 percent.

Switzerland’s central bank also specifically mentioned US tariffs, noting the global economy is being hobbled by the levies. A high degree of uncertainty remains and that barriers could in fact be raised further. Still, the SNB said the global economy could provide more resiliency than anticipated.

For the Swiss economy in particular, tariffs are the main risk, likely further dampening exports and investment, with watchmakers and manufacturers of machinery particularly hard hit. The services industry has been mostly spared, which should help the economy to remain stable amid some moderate growth. The SNB is forecasting growth between 1.0 to 1.5 percent this year and slowing to 1.0 percent next year.

The Swiss franc remains strong, with the SNB reiterating it’s willing to remain active in the foreign exchange markets. One option available to help ease the tariff impacts are devaluing the Swiss franc, although that would make imports more expensive. However, with inflation presently under control, it’s certainly an option for the SNB. This year, inflation is expected to be 0.2 percent, rising to 0.5 percent in 2026, and increasing again in 2027 to 0.7 percent.

Today’s decision shows a cautious SNB weighing its options and seeing how conditions develop around tariffs. In the United States, an appeals court upheld the decision of a trade court declaring most of the tariff’s illegal. That is expected to reach the US Supreme Court in October or November which is before the governing board meets again in December to decide on rates.

Inflation

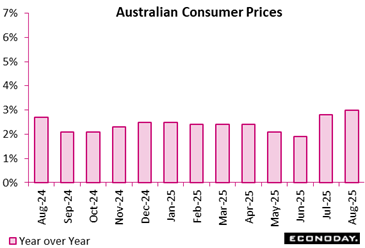

Monthly Australia CPI data show headline inflation rose from 2.8 percent in July to 3.0 percent in August, just above the consensus forecast of 2.9 percent, with annual electricity price increases the main factor pushing up headline inflation. Headline inflation has now been within the Reserve Bank of Australia’s target range of two percent to three percent for thirteen consecutive months but is now at its highest level for this period. This monthly indicator measures the year-over-year change in the CPI index compared with the same month twelve months earlier.

The increase in headline inflation in July was largely driven by electricity prices, up 24.6 percent on the year after a previous increase of 13.6 percent. This increase reflects the impact of rebates paid last year. Excluding this impact, electricity prices rose 5.9 percent on the year. Automotive fuel prices fell 1.7 percent on the year after a previous decline of 5.5 percent while food prices rose 3.0 percent on the year, as they did previously. Underlying measures of inflation showed mixed results, with the trimmed mean measure easing from 2.7 percent to 2.6 percent, and the measure excluding volatile items and holiday travel picking up from 3.2 percent to 3.4 percent.

At their most recent policy meeting last month, the RBA lowered policy rates by 25 basis points, with officials advising that they expect headline inflation to pick up slightly later this year but then fall back to around the mid-point of their target range of two to three percent. The minutes of the meeting published earlier this week also showed that officials expect to lower rates further but are not sure about the likely pace of policy easing. With the increase in headline inflation reported today largely driven by the impact of rebates, this may be discounted when officials assess whether another rate cut is warranted at their meeting next week.

Employment

The pace of US annual core PCE price inflation has been stuck at just under 3 percent since May – stubbornly refusing to make any further progress towards the Federal Reserve’s 2 percent inflation objective. That, along with the solid rate of consumer spending, underscores the increased uncertainty around the outlook for monetary policy, and why Fed Chair Jerome Powell’s warned this week about the upside near-term risks to inflation.

U.S. personal income rose 0.4 percent in August, matching the rate of increase in July and above expectations for a 0.3 percent rise in the Econoday survey of forecasters. Consumer spending, as measured by the Personal Consumption Expenditures (PCE) index, jumped 0.6 percent last month, following an unrevised 0.5 percent rise in July. Increased spending on goods (+0.8 percent) was boosted by the August 11 extension of the Trump administration’s pause on punitive tariffs on Chinese imports.

As for the Federal Reserve’s preferred inflation gauge, the PCE price index was up by 0.3 percent on a monthly basis in August, picking up the pace from the 0.2 percent uptick in July and following a 0.3 percent rise in June.

Prices for goods saw a 0.1 percent rise and prices for services increased 0.3 percent. Food prices jumped 0.5 percent and energy prices surged 0.8 percent. Excluding food and energy, the PCE price index was up 0.2 percent, following a 0.2 percent increase in July.

Compared to a year ago, the August PCE price index rose 2.7 percent, speeding up from a 2.6 percent year-over-year rise in July. Prices for goods are up 0.9 percent, and the cost of services jumped 3.6 percent. The core PCE price index is up 2.9 percent from August 2024, matching the pace set in July.

Expectations in the Econoday survey were for a 0.3 percent monthly increase and a 2.7 percent rise on an annual basis.

Business Surveys

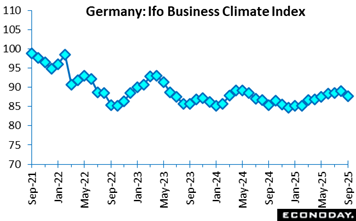

Germany’s September 2025 overall Ifo business climate index dropped to 87.7, well below both the consensus (89.1) and the previous month’s 89.0. This sharp fall signals that optimism is slipping faster than anticipated, with firms sensing headwinds rather than recovery.

The decline stems from weakness in both current activity and future outlook. Current conditions eased to 85.7 against expectations of stability at 86.4, suggesting that firms are already grappling with fragile demand and persistent cost pressures. More striking is the deterioration in business expectations, which fell to 89.7 from 91.6, missing forecasts of 91.7. This gap reflects growing unease about Germany’s near-term prospects amid sluggish global trade, energy uncertainty, and ongoing geopolitical tensions.

Taken together, the latest update implies that confidence is weakening across the corporate landscape. German firms are not only feeling the heat but also bracing for more challenging times ahead. Unless external conditions improve or domestic policy support strengthens, momentum in Europe’s industrial powerhouse risks slipping further into contraction territory.

Germany’s composite PMI rose to 52.4, its highest in 16 months and 2.3 points above the consensus, signalling growth momentum. This was primarily driven by the services sector, which bounced back strongly to 52.5 after slipping in August. Manufacturing, however, slipped further into contraction at 48.5, pointing to fragility in industrial activity. While output rose, new orders fell across both sectors, with manufacturers reporting their sharpest decline in demand since January and a second month of falling export sales. Businesses continued to rely on backlogs, which have been steadily depleting for more than a year.

Labour market conditions deteriorated further, with employment shrinking for a sixteenth consecutive month, especially in manufacturing. Rising cost pressures complicated the picture, as input and output inflation both accelerated to multi-month highs, led by services. Although business expectations remained in positive territory, confidence slipped below the long-run average, reflecting concerns about sluggish growth, persistent uncertainty and elevated costs.

Indeed, the data suggests that while Germany has regained some growth momentum, it remains underpinned by weak demand, declining employment and fragile confidence, leaving its recovery vulnerable to renewed headwinds.

US Review

Lower Mortgage Rates Lift Housing Sector

By Theresa Sheehan, Econoday Economist

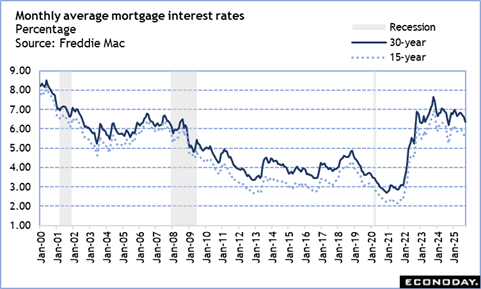

It appears that the recent declines in mortgage rates will provide a boost to the housing market in the near term. However, the burst of activity could quickly sap what little pent-up demand there is. Many potential homebuyers are concerned about the direction of the US economy, rising prices on essential items in household budgets, and broader job security. The sales pace may steady, although it is likely to remain soft.

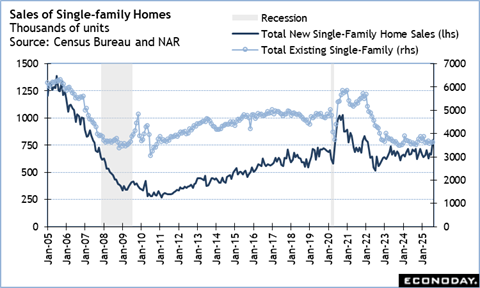

August sales of existing single-family homes – to look at the numbers outside the volatile multi-unit sector – are down a slight 0.3 percent to 3.63 million units at a seasonally adjusted annual rate compared to 3.64 million units in July. However, sales of existing homes are for contracts closed and largely reflect mortgages taken out in the prior month.

The Freddie Mac average rate for a 30-year fixed rate mortgage fell from 6.82 percent in June to 6.72 percent in July. This is a modest improvement but still near enough to the 7-percent mark that buyers often opted for adjustable-rate mortgages. July coincides with the start of the annual trend for the median price for an existing home to fall after peaking in June, and lower prices can tempt some buyers. The closing price of an existing single-family home declines 1.0 percent in August to $427,800from $432,000 in July. The price is up 4.5 percent compared to a year earlier. Home prices continue to appreciate on an annual basis although the pace has eased.

Sales of new single-family homes jump 20.5 percent to 800,000 in August after 664,000 in July and are up 15.4 percent compared to a year ago. Buyers moved quickly to sign contracts for new construction while the September Freddie Mac average rate for a 30-y6ear fixed rate mortgage dropped to 6.35 percent. The rate is one that improves the affordability of a home purchase and can lead buyers to opt for a larger unit than previously planned. New construction is typically more costly than existing units. The 4.7 percent increase in the median price for a new home at $413,500 in September from $395,100 in July is probably more from buying of pricier units than a widespread gain in prices. The year-over-year increase is 1.9 percent as supplies of new homes remain relatively abundant and facing competition from increased supplies of existing units.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.