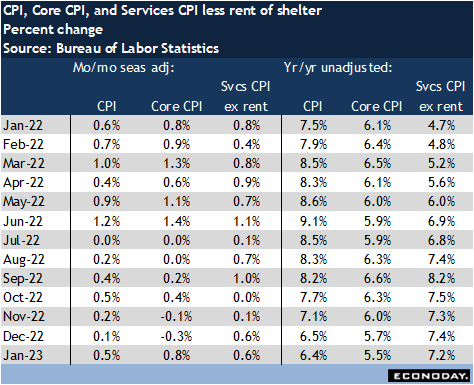

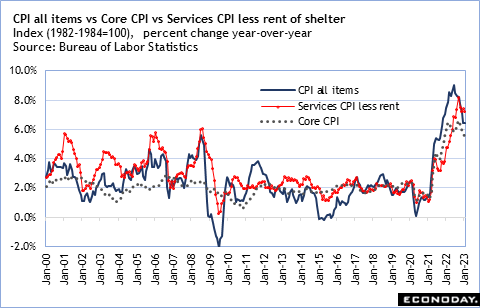

It is sometimes hard to parse out what Fed policymakers mean when they talk about non-housing services inflation. The CPI report has a special aggregate of the CPI for services less rent of shelter. It probably isn’t a perfect match with the Fed’s rhetoric, but it serves as a proxy.

A look at the data over the past year shows that the all items CPI peaked at a year-over-year up 9.1 percent in June 2022, core CPI at up 6.6 percent in August 2022, and services less rent for shelter continued to climb until it peaked at up 8.2 percent in September 2022. Since then, the all items CPI year-over-year change is at up 6.4 percent in January, down 270 points from its June 2022 peak. The core CPI – excluding food and energy – is down 110 points to 5.5 percent in January from its September peak. The CPI for services less rent for shelter has fallen only 100 points from its September 2022 peak.

This illustrates the problem facing the FOMC in taming inflation. While the headline numbers for the CPI look promising for inflation’s rapid improvement, and the core never rose as much as the all items and has since eased, there is a sort of core within the core that is less sensitive to the effect of higher interest rates. This is what worries Fed policymakers about inflation getting entrenched and what they are working to reduce. The CPI for services less rent for shelter will bear watching to gauge the timing of future rate hikes, and/or when the FOMC will pause in making monetary policy more restrictive to bring inflation down.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.