The ECB’s key interest rates have been raised a cumulative 200 basis points since the start of the current tightening cycle back in July. That in itself might be seen as reason for expecting this week’s central bank meeting to take its foot off the brake just to give time for the policy actions taken so far to have their effect. However, with annual inflation last month still some 8.0 percentage points above target, borrowing costs will assuredly be hiked again and the only question facing financial markets is the size of the increase. Following 75 basis point increases in both September and October, the consensus call is 50 basis points which would put the deposit rate at 2.0 percent, the refi rate at 2.5 percent and the rate on the marginal lending facility at 2.75 percent. However, a third successive 75 basis point cannot be ruled out, particularly in the wake of President Lagarde’s claim a couple of weeks ago that “rate hikes still have a long way to go”.

This week’s gathering is also expected to provide at least a general outline on how the balance sheet will be shrunk (QT) next year. The hawks have been pressing for QT for a while now and some, notably Bundesbank President Joachim Nagel, want to start next quarter. Currently, the bank is still committed to fully reinvesting maturing QE assets acquired under the asset purchase programme (APP) “for an extended period of time” after interest rates began to rise. For the PEPP, which was terminated in March, full reinvestment is scheduled to remain intact until at least the end of 2024. Outright asset sales (active QT) are unlikely to get past the doves, many of whom wanted only a 50 basis point hike in interest rates in October. However, a measured and predictable approach to reducing the reinvestment share of maturing assets (passive QT) should not find too much disagreement and, while certainly not a substitute in the eyes of the ECB, it might also ease some pressure for additional increases in rates. Indeed, some form of QT may well be needed to placate the hawks if rates do only rise 50 basis points.

Still, market expectations for ECB tightening next year are little changed from just before the October meeting. From currently around 2.0 percent, futures are pricing 3-month money rates at around 2.4 percent in January before peaking at about 3.0 percent in June. Subsequent expected ECB easing then sees rates drifting back down to just below 2.5 percent by the end of 2024.

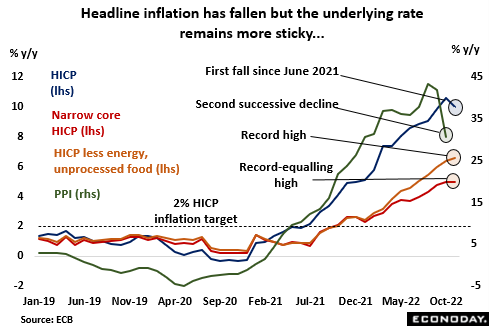

There was some good news for the ECB in the flash HICP inflation data for November. The headline annual rate finally decelerated (for the first time since the middle of last year) and by an unusually large 0.6 percentage points. However, at 10.0 percent, it was still a huge 8 percentage points above target and, more importantly, the drop was not mirrored in the underlying measures. Hence, the narrowest gauge held firm at October’s 5.0 percent record high while an alternative core that excludes just energy and unprocessed food accelerated from 6.4 percent to 6.6 percent, a new all-time peak. For some Governing Council (GC) members, this will be interpreted as an indication that inflation is becoming more entrenched, and so requires another substantial hike in interest rates to bring it back under control. The ECB has already said that it now places more weight on the core measures and these will become particularly important in 2023 when energy-related base effects are likely to subtract several percentage points off the overall rate. Producer price inflation has also slowed but even an 11 percentage point drop in October left the overall annual rate at some 30.8 percent and the monthly core rate saw a 3-month high.

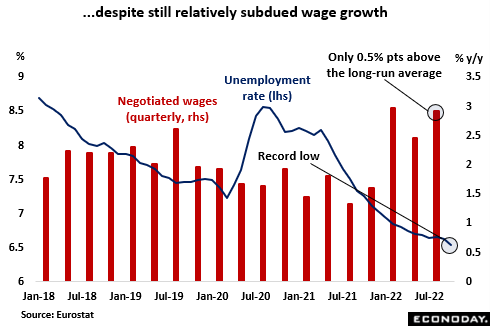

Meantime, the labour market, a key input into ECB policy decisions, remains as tight as ever. Apart from this August, joblessness has fallen every month since April 2021 and at 6.5 percent in October, the unemployment rate was the lowest on record. Demand has clearly slowed but vacancies are at unprecedented levels and business surveys show firms across much of the region are still struggling to find staff. However, to date, the impact on wages appears to have been quite mild. Negotiated wage data for the region are only available on a quarterly basis but for the three months to September annual growth was running at a relatively subdued 2.9 percent, only 0.5 percentage points above its long-run average. That said, recently there have been signs of sizeable one-off payments by firms trying to retain staff; not helping matters is a marked deterioration in the efficiency of the existing workforce.

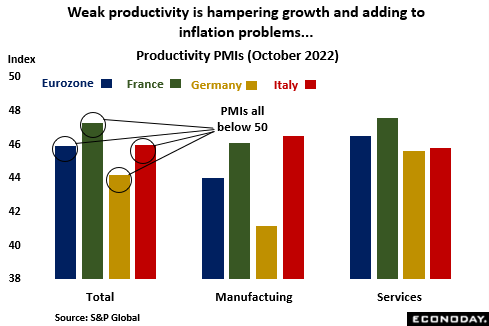

Productivity has slumped across the region as output growth has slowed and headcount continued to rise. According to S&P Global’s PMI survey, October saw both a sixth successive monthly deterioration and the fastest decline since mid-2020. All of the larger three member states have witnessed a significant worsening in performance, particularly in manufacturing where Germany has suffered disproportionately. Declining productivity is hampering output and adding to upside pressure on inflation as firms are forced to raise prices to protect profits already squeezed by declining demand. Retailers are struggling badly as rising prices and near-record low consumer confidence undermine sales which, in October, fell to their lowest level since April 2021. Private sector orders have been falling steadily since July with losses in both the domestic and overseas markets, and business sentiment in November was only just above September’s 28-month low. However, at this stage the downturn in economic activity is unlikely to significantly impact policy as most GC members seem to accept that a mild recession would not of itself be capable of returning inflation back to target.

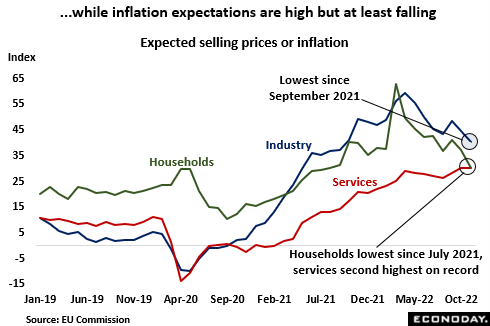

Crucial to the ECB policymakers are inflationary expectations and here developments have been mixed. According to the ECB’s own survey, median household year-ahead inflation expectations in October rose from September’s 5.1 percent to 5.4 percent while the 3-year ahead outlook was stable at 3.0 percent. However, the EU Commission found expected selling prices in industry declining in November to their lowest mark in more than a year while households’ inflation outlook was the weakest since July 2021. Even so, the falls have been from the all-time peaks registered earlier in the year and current levels remain historically very high. Indeed, in services a minor dip in expected prices charged last month still left the second highest reading on record. Accordingly, while recent results have broadly been moving in the right direction, all the measures have a long way to go to reach normal levels.

More generally, the Eurozone economy has held up a little better than expected since the October ECB meeting. Econoday’s consensus divergence index (ECDI) which measures how overall economic activity has recently performed versus market expectations, has been mainly, although certainly not exclusively, in positive surprise territory. In other words, in the main the forecasters have been a little too pessimistic. This may increase the chances that the widely anticipated downswing will at least be no worse than currently anticipated.

In line with so many other central banks, the ECB remains firmly in tightening node. However, with key rates approaching neutral levels and disagreement over where the terminal rate lies, it is probably reasonable to assume 75 basis point hikes are coming to an end, particularly if QT is launched next quarter. That said, with the central bank’s credibility riding on getting inflation back down it is unlikely that the interest rate rises will be ended prematurely which probably leaves economic risks firmly tilted to the downside.