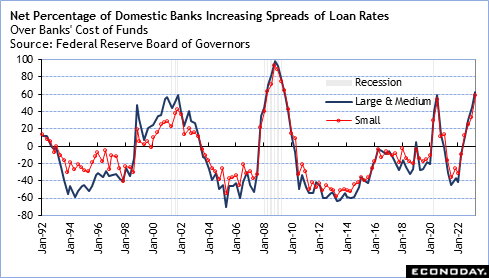

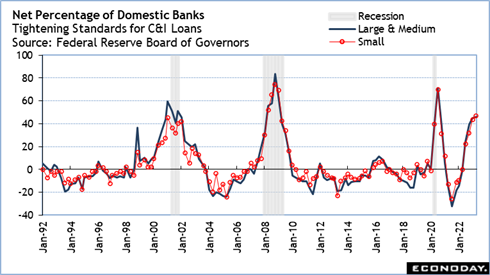

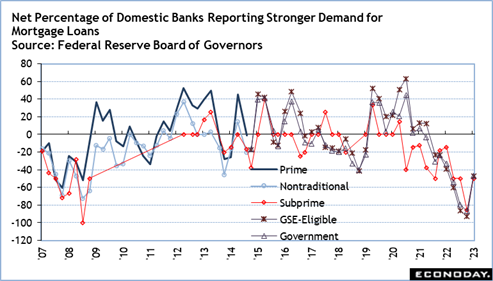

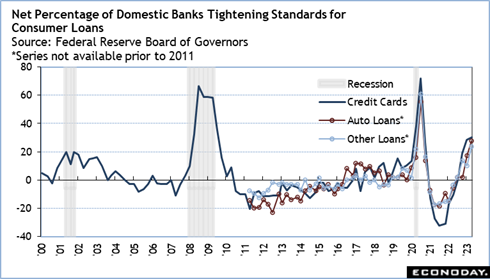

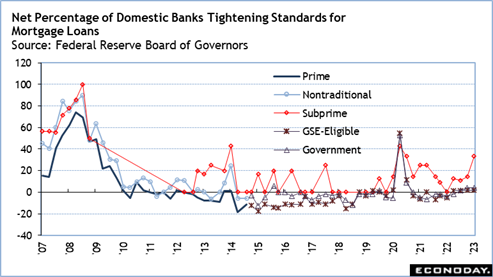

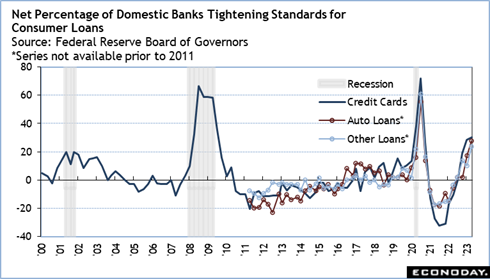

The April senior loan officer opinion survey on bank lending practices was presented to Fed policymakers at the May 2-3 FOMC meeting. It shows tighter standards and weaker demand for commercial and industrial loans (C&I) and for commercial real estate (CRE) lending. For residential real estate loans, almost all categories of lending have tightened standards other than GSE-eligible and government residential mortgages which were about unchanged. Demand for mortgages was weaker in all categories of residential real estate lending. Standards are tighter for home equity lines of credit and for all other types of consumer lending except credit cards which are not much changed.

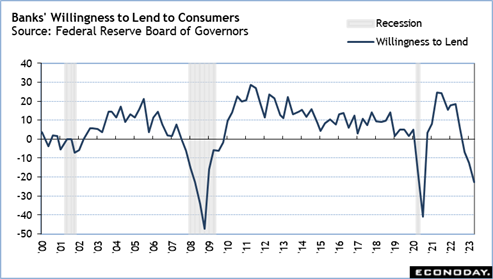

The current reports of tightening of bank lending standards – both commercial and consumer – and unwillingness to lend to consumers are consistent with periods of recession. Whether the US is technically in a recession or not, restrictive financial market conditions will, as Fed policymakers say, weigh on growth and reduce demand. This is a positive development in the fight against entrenched inflation, but worrisome for those fearing a deterioration in the labor market.

The report said, “The April SLOOS included three sets of special questions, which inquired about banks’ changes in lending policies for CRE loans over the past year; about the reasons why banks changed standards for all loan categories over the first quarter; and about banks’ expectations for changes in lending standards over the remainder of 2023 and reasons for these changes.”

The report does not directly reference recent developments in the banking industry and if the failure to manage interest rate risk is on the mind of loan officers. However, it is clearly hovering in the background, especially for the community and regional bank.

The report said, “In comparison to the largest banks, mid-sized and other banks more frequently cited concerns regarding their liquidity positions, deposit outflows, and funding costs as reasons for tightening. Major shares of mid-sized banks cited the economic outlook, reduced tolerance for risk, concerns about the bank’s liquidity position, deterioration in collateral values, deterioration in credit quality of loan portfolio, bank funding costs, and deposit outflows as reasons for tightening. Major shares of other banks cited the economic outlook, bank funding costs, reduced tolerance of risk, collateral values, concerns about their liquidity position, and deposit outflows as reasons for tightening.”

The responses indicated that banks have broadly tightened “lending policies for all categories of CRE loans over the past year, with the most frequently reported changes pertaining to wider spreads of loan rates over banks’ cost of funds and lower loan-to-value ratios.” As to why, “banks cited a less favorable or more uncertain economic outlook, reduced tolerance for risk, deterioration in collateral values, and concerns about banks’ funding costs and liquidity positions.” Banks also expect to continue to tighten lending standards “over the remainder of 2023”. The report notes, “Banks most frequently cited an expected deterioration in the credit quality of their loan portfolios and in customers’ collateral values, a reduction in risk tolerance, and concerns about bank funding costs, bank liquidity position, and deposit outflows as reasons for expecting to tighten lending standards over the rest of 2023.”