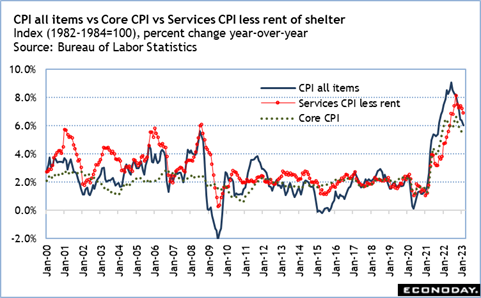

The April 10 week is a fairly busy one for economic data. The standouts will be the March CPI data on Wednesday at 8:30 ET and retail and food services sales at 8:30 ET on Friday. The CPI will be critical to the inflation outlook for Fed policymakers. The data will be scrutinized to see if any of the long and variable lags in changes in rates will be more visible for consumer prices. The all-items CPI was 6.0 percent year-over-year in February, down 4 tenths from the prior month. The annual pace of core CPI slipped only a tenth to 5.5 percent. However, the CPI for services excluding rent was down 3 tenths to 6.9 percent in February, its lowest since 6.8 percent in July 2022. If Fed policymakers see improvement in non-housing services inflation, it should cement expectations for the FOMC to soon pause in the current cycle of rate hikes.

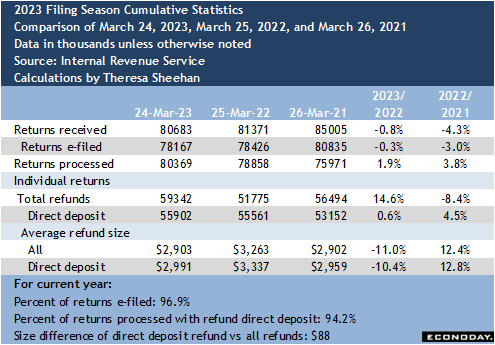

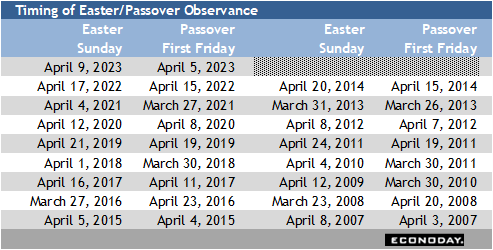

The March retail sales numbers face a number of special factors. Unit sales of motor vehicles were slightly weaker at 14.8 million (seasonally adjusted annualized rate) after 15.0 million units in February. However, if prices were not heavily discounted, the dollar value may not have changed much month-over-month. Gasoline prices were up in March from February, so the dollar value of sales at service stations should also be up, especially with travel for spring break. Some of the change may depend on consumers who received a tax refund and whether they decided to spend, save, or pay down debt. As of IRS statistics on March 24, the average size of a refund is 11.0 percent smaller than last year and is running just below $3,000. Finally, the timing of the Passover and Easter observances could affect sales. Passover began April 5 and Easter is April 9. The relatively early timing could bring some sales forward into March.

The minutes of the March 21-22 FOMC meeting will be released at 14:00 ET on Wednesday. These won’t be devoid of interest, but the timing means these won’t encompass later developments. The fallout from the disruptions in the banking sector that began with the failure of Silicon Valley Bank on March 10 can’t be fully accounted for. Improvements in inflation were tentative in late March and added to the uncertainty in the outlook for monetary policy. The March employment report gives the FOMC some leeway for another rate hike at the May 2-3 meeting to ensure that monetary policy is doing its job.