The April 24 week will see an absence of Fed speakers during the communications blackout period around the May 2-3 FOMC meeting. The period begins at midnight on Saturday, April 23 and runs through midnight on Thursday, May 4. There are no data reports on the calendar prior to the meeting that are likely to change expectations for the outcome. Most Fedwatchers think there will be another 25 basis point rate hike in the fed funds target range and then a pause while FOMC participants allow previous rate hikes to do their work.

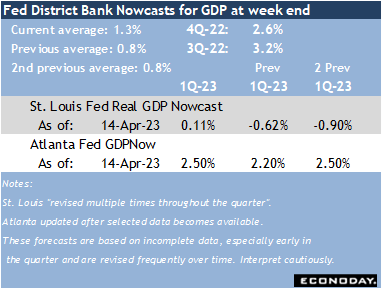

As of Friday, April 14, the GDP Nowcasts from the St. Louis and Atlanta Feds point to at least some growth when the advance estimate of first quarter GDP is released at 8:30 ET on Thursday. The St. Louis Real GDP Nowcast looks for an increase of just 0.11 percent while Atlanta’s GDPNow sees a more robust 2.5 percent rise. Forecasters’ early estimates are centering near the Atlanta measure. Even if there is a downside surprise, it is unlikely to alter the FOMC decision as policymakers are prepared for “subpar” growth and continue to emphasize the inflation fight.

Forecasts may get some last-minute updates when the Commerce Department releases annual revisions for retail sales on Monday at 10:00 ET. Consumer spending was soft in February and March (down 0.2 percent and down 1.0 percent) after an outsized increase in January (up 3.1 percent). The revisions could add or subtract from those performances.

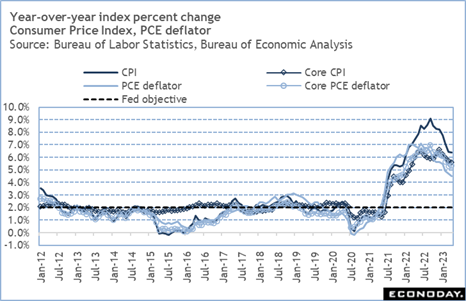

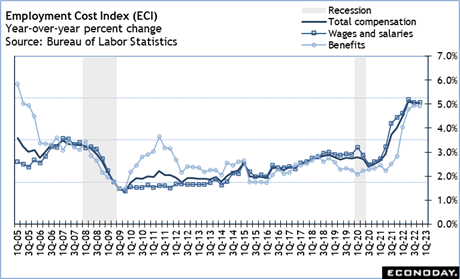

There are two important readings for inflation in the week. The March PCE deflator will be reported with the numbers on personal income and spending at 8:30 ET on Friday. Also at that time will be the employment cost index (ECI) for the first quarter. Fed policymakers will be looking for signs of moderation in consumer prices – especially in non-housing services – and whether upward pressures on employee compensation are easing. Again, even a downside surprise in either report shouldn’t change the outlook for a 25 basis point hike at the May 2-3 FOMC meeting. While inflation measures may be moving in the right direction, there is still a distance to go before the Fed will say that inflation is consistently moving closer to the 2 percent objective.