The focus in the April 3 week will be on labor market data, just how tight employment remained at the end of the first quarter 2023 and what that means for the economic outlook and monetary policy.

Note that April 7 – Good Friday – is not a federal holiday in the US. However, there is an early close at 2:00 ET that day for the capital markets; the stock market will have a full close.

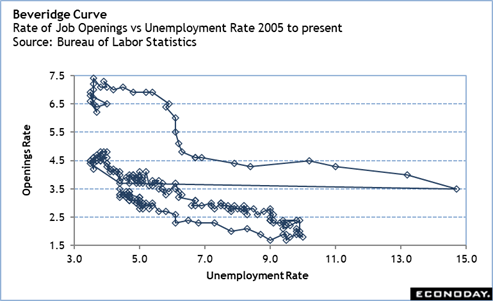

The February JOLTS report at 10:00 ET on Tuesday should reflect the shrinking – but still plentiful – number of job openings. It should also show if the pace of hiring is moderating and if layoff activity is rising. It will almost certainly show the number of people voluntarily quitting a job is declining as the imbalances in the labor market improve.

The ADP national employment report for March at 8:15 ET on Wednesday should indicate where private payrolls are growing. Recent months have shown that leisure and hospitality – which has long been seeking workers – continues to improve. However, tech companies and some financial services may be weaker. Also important to note will be if wage growth is easing up.

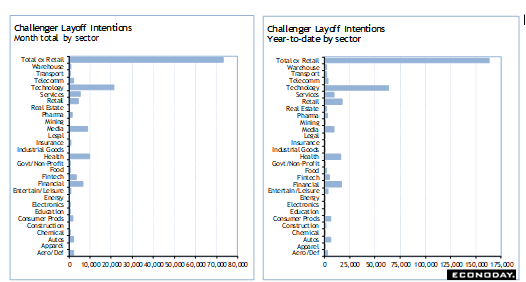

The Challenger report for March at 7:30 ET on Thursday will highlight the sectors where layoffs announcements are taking place. In recent months it has been the tech sector that has dominated the story, but the February report hinted that layoffs are becoming more broad-based due to deteriorating business conditions.

The initial jobless claims report for the week ended April 1 at 8:30 ET on Thursday will include annual revisions. They probably won’t do much to change the tone of the recent data, but the revisions may be enough to require a little extra time to explore and understand the underlying trend.

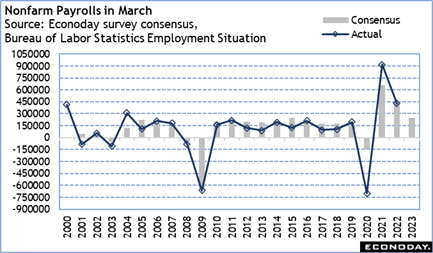

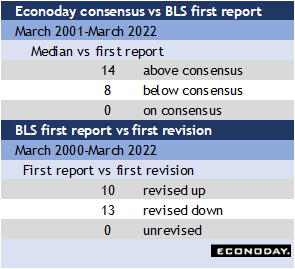

The employment situation for March at 8:30 ET on Friday is expected to show that payrolls continued to rise at a healthy pace, although not as quickly as in January and February. March payrolls can be tricky to seasonally adjust due to the timing of spring breaks for various school systems and the Easter/Passover observances. However, March often comes in above the market consensus. The early consensus for March nonfarm payrolls is roughly 250,000 at this writing.